|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

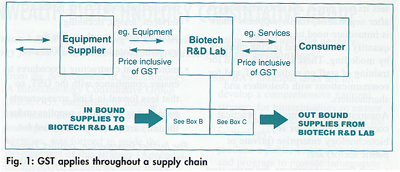

Australasian Biotechnology, Vol. 10 No. 1, 2000, pp. 31-32 THE IMPACT OF THE GST IN THE BIOTECHNOLOGY SECTOR Trevor Chambers and Dr Craig Fowler, Ernst & Young Code Number: au00013 The introduction of the Goods and Services Tax (GST) on 1 July 2000 is the next major business issue for Australian enterprises to grapple with and implement. This article is intended to provide brief explanation of the basics of the GST and gives some insight into its many complexities. Further articles in subsequent issues will explore those complexities in greater detail. GST is a 10 per cent tax on both goods and services and rests at its core on the concepts of (and legal definition of): supplies that are made for consideration; in the furtherance of an enterprise; with these supplies being connected with Australia; and made by an enterprise which is registered or required to be registered. It applies equally to the public and private sectors and under circumstances where supply has the widest possible definition in relation to goods and services and where consideration is not necessarily limited to money. The mechanics of the tax are such that GST is collected at every point of production and/or service delivery, ie. at each transaction in a supply chain (Fig. 1). It is the final consumer who ultimately bears the tax. Registered enterprises in the supply chain must account for GST to the Australian Tax Office (ATO) the net of the GST they paid on their inbound supplies (ie. business input costs) and that GST they are liable for on their outbound supplies (ie. on revenue earned by providing goods and services). The enterprise will therefore on a periodic basis (monthly or quarterly) remit payments to, or seek credits from, the ATO in accord with their net GST outcome.

There are three different categories of supply in the GST legislation; these being Taxable; GST-free and input-taxed supplies (see Box A). A limited number of events may be outside the scope of GST, eg. salaries paid to employees, and some appropriations involving inter-Government transactions. Most supplies are taxable. Some supplies, for the public good or other reasons are GST-free, eg. education, health, childcare; and some food, as well as exports, whilst other supplies are input-taxed, eg. many financial supplies. The consequences of these categories are explained in Box A. Typical goods and services supplied to (inputs) or provided by (outputs) a biotechnology enterprise are shown in Boxes B and C. The GST is not simply a tax issue. It has widespread impact across the operations of any enterprise including its accounting and information management systems, its commercial activities (eg. cash flow, contracting, capital expenditure, pricing etc.) and its communications with stake-holders. From a practical perspective, all supplies within the scope of the GST must be identified and accounted for, ie. each transaction must have its correct GST supply status applied consistent with the legislation. Each transaction must then be correctly captured in accounting systems. Input tax credits on enterprise-related expenses must be verified by possession of a GST compliant tax invoice, and claimed provided they are for creditable acquisitions ie. acquisitions used by the enterprise in making taxable or GST-free supplies, rather than, for example, acquisitions for personal use. All adjustments for prior periods, eg. bad debts and volume discounts, must be included where they change prior returns. All this means businesses need to be efficient in regards to GST administration so as to minimise their compliance costs. From a commercial perspective, the GST will potentially have significant impacts on cash flow and pricing strategies. There will be pricing adjustments that will ripple through the national economy over the next six months or so. Prices will not automatically increase by 10%; rather prices will only increase/decrease after all prior taxes embedded in the economy are removed, eg. wholesale sales taxes, and GST levied where applicable. Further, there is the expectation, under threat of scrutiny and penalty by the Australian Competition and Consumer Commission (ACCC) that this transition will not be accepted as an excuse for price exploitation or adjustment in margins. This means any biotechnology enterprise must be mindful as to how it sets its new prices and also what it pays, after negotiation, for its supplies. There is immediate need to assess and quantify these cost and pricing changes by modelling. There is also the need for training of staff on matters GST and for communications with customers and shareholders. Amongst the most important practical commercial issues for any biotechnology enterprise (private or public sector) are:

For further information, contact Trevor Chambers - Partner (Transaction Taxes and Tax Reform) on (03) 9288 8827, email trevor.chambers@ernstyoung.com.au or Dr Craig Fowler - Senior Manager (Transaction Taxes and Tax Reform) on (03) 9288 8947, email craig.fowler@ernstyoung.com.au

The following images related to this document are available:Photo images[au00013f1.jpg] |

| |||||||||

{kind=link}