|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

Australasian Biotechnology, Vol. 10 No. 3, 2000, pp. 33-43 Biotechnology and bioscience industry review: Australian Biotechnology and Bioscience Based Industry David Fayle, BioAccent Pty Ltd [www.bioaccent.com.au], Canberra, ACT; Kelvin Hopper and Joan Dawes, Aoris Nova Pty Limited [www.aoris.com.au], Sydney, NSW Code Number: au00035 SUMMARYA detailed new analysis of the biotechnology industry in Australia covers 151 dedicated biotechnology enterprises (“Group 1”), plus more than 150 other companies which have significant biotechnology involvement as part of their spectrum of activity, and/or are operating in closely related areas of bioscience (“Group 2”). For Group 1, major areas of biotechnology activity are analysed. About 43% of these companies have their main focus on health, with significant numbers also in agribiotech/food, biologicals, genetic testing, veterinary, or several different major areas. Of the health sector, 63% mainly concentrate on pharmaceuticals, 15% on diagnostics, and 12% on both. Group 1 companies listed on stock exchanges are identified, and additional Tables list examples of companies focusing on selected industry sectors. New South Wales and Victoria each account for around 30% of the Group 1 companies, with the other mainland States hosting 9%-12% each. Results from previous studies are summarised on key indicators of industry growth such as revenue, exports, strategic alliance activity, and intellectual property transaction activity. International comparison reveals that Australia rates relatively well in terms of number of dedicated biotechnology companies. Many of these are small, young start-up ventures, and the industry has expanded markedly recently. The 21/2-year period to mid-2000 has seen 39 enterprises commence their biotechnology activity - 26% of the currently active companies. We conclude that to build the Australian biotechnology industry as a key player in the 21st century economy, the emphasis should be on developing stronger, more viable companies, with better access into global markets. For Group 2 companies, which operate over a wide spectrum of biotechnology and bioscience sectors, Tables show examples of companies in prominent areas of activity, and companies listed on the Australian Stock Exchange. The article concludes by identifying selected areas of strength in the Australian biotechnology and bioscience based industry, with numerous examples of companies to illustrate the wide variety of products and activities. ANALYSIS OF AUSTRALIAN BIOTECHNOLOGY-RELATED INDUSTRY Overview Taking a broad definition of biotechnology related industries, Australia’s small but dynamic sector has entered a phase of strong growth, especially over the last four years. A large number of promising start-up companies have come onto the scene during this period, and a number of companies have successfully listed on the Australian Stock Exchange (ASX) and other world stock exchanges. These trends look set to continue, although the recent downturn in investment in many technology companies, including some in biotechnology, raises short-term uncertainties for generating capital. Blockbuster products initiated from fundamental Australian research are now among the world’s biggest selling biopharmaceuticals. The colony-stimulating factors G-CSF and GM-CSF, discovered by Professor Donald Metcalf and colleagues at the Walter and Eliza Hall Institute of Medical Research in Melbourne, were commercialised by multinational biopharmaceutical companies. In 1998, worldwide sales of G-CSF and GM-CSF totalled around US$1.35 billion and US$80 million, respectively. A second potential blockbuster, the flu drug Relenza™, developed by Biota with Glaxo-Wellcome, is also making an impact on the world market. Many biopharmaceuticals are in the drug development pipeline - a few examples are Progen’s PI-88; AMRAD’s AM424, AM365, AM133 and others; Novogen’s NV-06, NV-07, NV-08 and NV-04; Pi2/Biotech Australia’s PAI-2; and the Howard Florey Institute’s relaxin, licensed to US company Connetics. A number of home-grown biotechnology companies, across a broad range of technologies and applications, are now established in the market, growing and consistently profitable, and on current trends, the industry as a whole is starting to deliver on the high expectations of the 1980s. Biotechnology: the application of science and engineering in the direct or indirect use of living organisms or parts of organisms in their natural or modified forms, in an innovative manner, in the production of goods and services or to improve existing processes.2 Table 1. Stock-exchange-listed biotechnology companies

Number of biotechnology companiesUsing this definition of biotechnology, we can identify 151 dedicated biotechnology enterprises in Australia (“Group 1”), with a further 16 operational subsidiary companies. This total includes a small number of biotechnology-specific funding vehicles. Other definitions give counts of 120-170 companies1. In common with other similar countries with active R&D programs, a number of companies originating over the previous 15-20 years have consolidated their positions and others have ceased operations. More than 150 additional companies have significant biotechnology involvement as part of their spectrum of activity, and/or are operating in closely related areas of bioscience (“Group 2”). This snapshot of the Australian biotechnology industry will cover these groups in turn. Group 1 - dedicated biotechnology companiesFig 1Stock-exchange-listed biotechnology companies Almost 17% of Australia’s dedicated biotechnology companies (25) are listed on stock exchanges, primarily the Australian Stock Exchange (ASX). The number of listings continues to grow, with Prana Biotechnology Ltd being the most recently listed company at the time of writing. Among companies publicly known to be planning ASX listing during 2000 are:

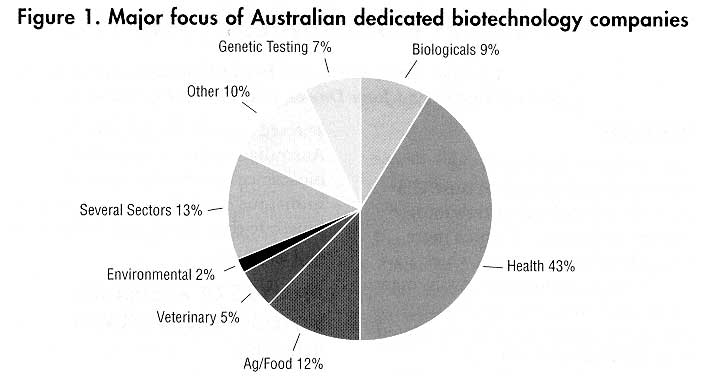

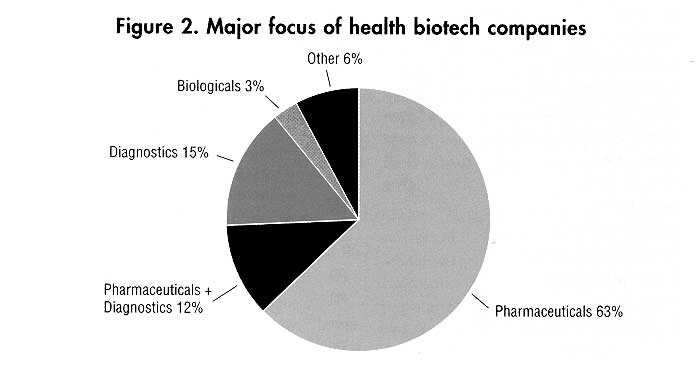

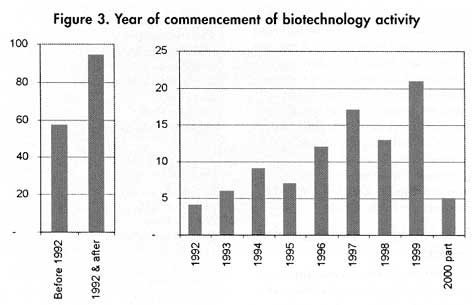

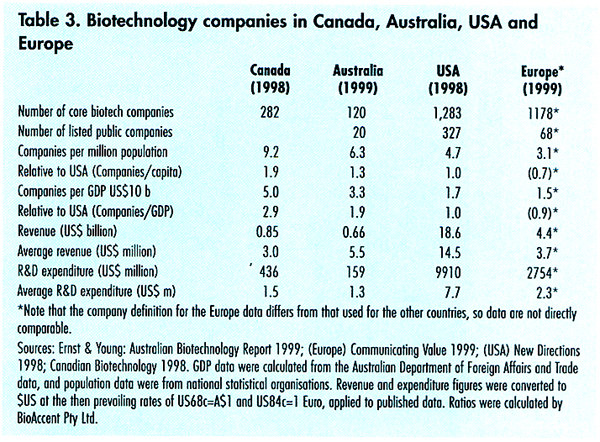

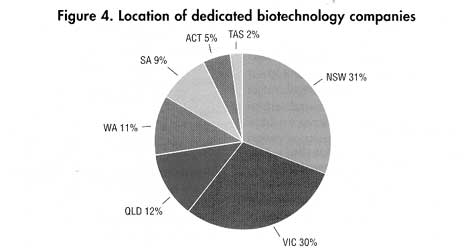

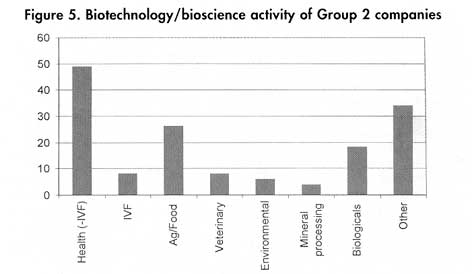

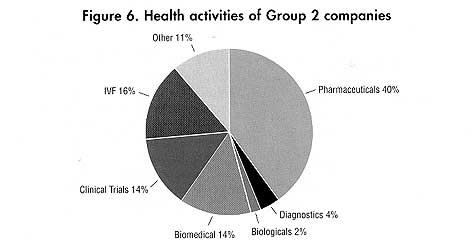

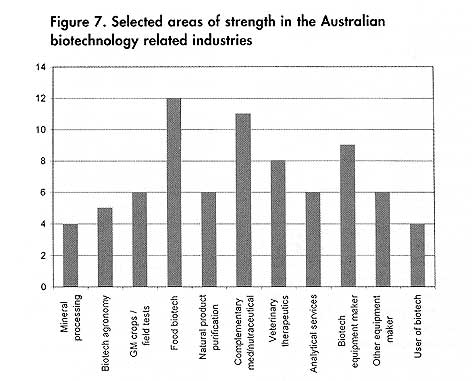

For much of the past 18 months, biotechnology companies listed on the Australian Stock Exchange (ASX) have fared, as a group, better than the major listed companies in traditional sectors. The ASX Healthcare & Biotechnology Index (10 of the larger companies) significantly outperformed the All Ordinaries Index during the whole of 1999 and the first quarter of 2000. Several more comprehensive specialist indexes have been developed, notably the Deloitte Touche Tohmatsu Biotech Index3, but the trends are similar, because the overwhelming influence on any index is that of the nine largest companies. Unlisted biotechnology companiesThe other 83% of Australia’s dedicated biotechnology enterprises represent a diverse group, operating across a wide spectrum of industry. These companies will be covered later in this report. Focus and sectors of activityBiotechnology, being a set of powerful technologies rather than an industry in the classical sense, impacts on many industry sectors. Some companies are tightly focused on a particular sector; others operate in several areas, or have platform technologies that are widely applicable. Australian dedicated biotechnology companies span a wide range of sectors. Health constitutes one of the most important (Figure 2); well over 40% of the companies focus on this sector. In addition, of the companies focusing on several sectors, more than half have projects in the health sector. Three out of every four health biotechnology companies have major activity in the pharmaceutical area, while a quarter focus on human health diagnostics; the overlap - firms with significant efforts in both diagnostics and pharmaceuticals - totals eight companies. Some examples of companies in the health sector will be covered later in the article. Biotechnology companies grouped by sectorBiotechnology related companies, grouped by broad area of activity, are shown in the Table 2. Many companies are active in two or more areas, but are listed under their major focus. This Table shows a representative selection of companies; publicly listed companies head each list (shaded in grey), followed by unlisted companies. A few companies from Group 2 are included for convenience. Dedicated biotechnology companies - Recent analysesAn important 1999 survey of the industry in Australia was carried out by Ernst & Young and the Commonwealth Department of Industry, Science and Resources (ISR)3; the biotechnology definition used in their Australian Biotechnology Report 1999 (see earlier panel) is also used here. Revenue and exportsBased on their 1998/99 survey3, for 120 Australian core biotechnology companies, the Australian Biotechnology Report 1999 estimated total revenue at A$965 million, of which $801 m (83%) was product sales and $31 m (3%) was contract research. About 76% ($737 m) of total revenue was based on biotechnology. Approximately 50% of all revenue was from exports. The bulk of total revenue (76%) was earned by the 20 surveyed companies listed on stock exchanges. Capital raisingThe companies surveyed for the Australian Biotechnology Report 1999 raised almost AU$184 million capital during 1998/99, including more than $25 m in four initial public offerings. Since the start of 1999, eight Group 1 companies have collectively raised over A$52 million listing or relisting on stock exchanges. R&D focusThese 120 companies are strongly focused on R&D, with total 1998/99 R&D spending of AU$234 million. Predictably, given Australia’s strong research effort, many companies are spin-offs from research institutions. A 1998 analysis undertaken by Dr Lyndal Thorburn of Advance Consulting & Evaluation Pty Limited covered 132 dedicated biotechnology companies1; of these, 40% were spin-offs from research institutions. Typically, the institutions license commercialisation rights to the company. Numerous spin-off enterprises have been formed since this analysis was done. Strategic alliance activityStrategic alliances and links between the Australian biotechnology industry and other organisations, both within Australia and overseas, are important. Dr Thorburn surveyed a set of 60 companies, and found one-third with collaborative R&D arrangements, one-quarter with R&D contracts, and 22% with in-licensing agreements. Joint ventures (7%) and technology exchange agreements (6%) were less common. Industry interest in the synergies and mutual benefits possible with well-crafted strategic alliances is growing rapidly. Funding pressures have accelerated a similar trend in the research sector. Intellectual property transaction activityThe Australian Biotechnology Report 1999 confirmed that companies were very active in intellectual property transactions, with half the 90 surveyed firms reporting licensing activities (181 licences acquired and 219 issued). The 90 companies held a total of 1,400 patents, with 176 new applications approved, and a further 86 lodged, during the previous 12 months. FormationA high proportion of our current set of 151 extant dedicated biotechnology enterprises commenced their biotechnology activities recently - two-thirds of them during the decade 1991-2000, and 50% since the beginning of 1995. These data, however, do not include companies now defunct. It is particularly striking that in the 18 months since the start of 1999, 26 dedicated biotechnology enterprises have commenced activity - 17% of the total. Adding 1998 data brings the total to more than a quarter (39). LocationNew South Wales (48 companies) and Victoria (46) together account for more than 60% of Australia’s dedicated biotechnology companies. Victoria is notably strong in health biotechnology companies, with 24 (37% of the health-focused group - about 75% more than the rest of Australia on a population basis). NSW is relatively strong in platform technology companies and others operating across several sectors, with 45% of that category. Comparison with USA, Canada, and Europe In addition to their Australian Biotechnology Report 1999, Ernst & Young has carried out broadly comparable analyses in Canada, the USA and Europe, thus covering the vast majority of the world’s biotechnology industry. Discussing the respective biotechnology industries, they observed that “Australia is most similar in structure to the Canadian biotechnology industry, with many small and medium sized companies accounting for a large proportion of core biotechnology companies. By comparison, the USA and Europe include significantly large companies (more than 300 employees).” With over 280 firms, predominantly small companies, Canada has generated in relative terms among the most biotechnology companies, whether measured per capita or per Gross Domestic Product; similar relative company numbers are found in Sweden, Finland, Ireland and Denmark. Canada has relatively more core biotechnology companies than AustraliaComparison reveals that, whether measured against population or Gross Domestic Product, Canada has 45% -50% more core biotechnology companies than Australia. Even using our actual count of dedicated biotechnology enterprises (151) rather than the Ernst & Young/Department of Industry, Science and Resources extrapolated estimate (120), Canada’s relative count is still 16%-20% higher. Australia would appear to have a slight edge in company average revenue, though this is distorted markedly by the revenues from one large Australian company. It is nevertheless clear that both countries have a large number of small companies in this sector, and that the industry as a whole has only modest revenue. R&D expenditure per company is very similar. USA has relatively fewer companies than Australia or CanadaThe most surprising feature of these data is that the relative number of such companies in Australia is significantly larger than in the USA by 30%-90%, depending on how it is measured. On our numbers, this difference would be accentuated. Even allowing for differences in threshold or definition in data collection, this indicates that Australia matches the USA in relative company number.However, the US companies are much larger and the industry more mature Most US biotechnology companies are, however, very much larger in terms of both revenue and employee numbers than their Australian counterparts, reflecting the greater maturity of the US industry as well as some recent consolidation. The discrepancies in revenue are even greater than the data implies, for reasons already mentioned. The average US company also spends nearly six times more on R&D than its Australian equivalent, again reflecting its higher income to fund the R&D. Australian biotechnology companies, particularly the 83% not listed on the Australian Stock Exchange (ASX), are still predominantly at an early stage of growth and development. The contrast between Canada and the USA is even starker, with Canada having almost threefold more core biotechnology companies than the USA relative to GDP. Again, Canada’s companies are much smaller and less mature than those in the USA. Europe presents a complex pictureOn these figures, compared with Europe as a whole, Australia appears to have twice the relative number of core biotechnology companies. The company counts for Europe are only indicative, however, due to the use of different criteria for inclusion in the survey. It seems likely, though, that a comparable survey would provide a similar picture. The European data conceal marked differences among constituent countries, but they also reflect an historically adverse public acceptance climate in Europe. ConclusionWe conclude that, for further development of the biotechnology related industries in Australia, the main emphasis should be on fostering the growth of companies of larger effective critical mass, with global brands. Nevertheless, the current increase in small start-ups here is a healthy process, since they contribute to the growth of larger companies. We can draw important lessons from international benchmarking, but the development of the industry in Australia has unique aspects for example Canada and Australia have many similarities but there are some differences in relative access to markets (which often drives company size), and access to capital. Biotechnology deals with global problems, and Australian biotechnology needs to build stronger international linkages as quickly as possible to offer unique solutions to these problems. We predict that there will be more mergers and collaborative ventures in Australia, but also more international trade through joint ventures, mergers and company sales. Group 2 - other companies with biotechnology, or in related bioscience areasOutside of the dedicated biotechnology companies just described, there are many companies which have significant life science involvement as part of their spectrum of activity, and/or are operating in closely related areas, typically bioscience instrumentation, biomaterials, chemistry or medicine. More than 150 such companies (Group 2) form the basis for the analysis which follows. This list is not comprehensive and these companies, predictably, cover a very wide spectrum of biotechnology and bioscience activities. “IVF” in Figure 5 represents in vitro fertilisation (assisted reproduction). ASX-listed Group 2 companies active in areas of biotechnology and bioscienceDedicated biotechnology companies listed on stock exchanges were shown in an earlier Table. Group 2 listed companies are shown here. The table includes the most recent listing at the time of writing, Vita Life Sciences Limited, a diversified company producing the nuclear medicine diagnostic Technegas and associated medical equipment, as well as pharmaceuticals, complementary medicines, dietary supplements and health foods. Companies understood to be planning to float include the transdermal drug delivery developer Norwood Abbey Ltd., the medical diagnostic and monitoring equipment specialist Compumedics Sleep Pty Ltd, and a company with novel radiopharmaceutical micro-particle technology for the treatment of liver cancer, Sirtex Medical Limited. Selected companies grouped by area of biotechnology/ bioscienceSelected Group 2 companies are shown in the following Tables, classified by broad area of activity. As before, not all companies in a category are listed. Group 2 companies in health sectorThe biotechnology and bioscience activities of nearly half of these companies fall into the health area. A closer look at the health companies reveals that about 40% are in pharmaceuticals, with significant numbers also in biomedical equipment, clinical trial management, and diagnostics. Companies providing assisted reproduction services, which could arguably be classified as Group 1 biotechnology companies, were included in Group 2 for this analysis. The seven companies listed in Table 5 together account for over 60% of the in vitro fertilisation activity in Australia. Group 2 companies in other sectorsAmong the biotechnology and bioscience activities outside the health sector, particular areas of strength in Australian industry can be seen in Table 5.Sectors of biotechnology and bioscience industry strength SECTORS OF BIOTECHNOLOGY AND BIOSCIENCE INDUSTRY STRENGTHThe following section comprises examples and case studies from both Group 1 and Group 2, highlighting some of the areas in which Australian industry is particularly active. Health sector Biopharmaceuticals and therapeutics Ten examples of promising biopharmaceuticals under development were mentioned earlier. Australian companies and research organisations have a large number of other therapeutics in their development pipelines, comprehensive coverage of which is beyond the scope of this article. A few additional examples, here and later in the article, will serve to illustrate the range of targets and approaches. Praxis Pharmaceuticals, Inc. (based in Canberra) is developing novel anti-inflammatory drugs, initially for the treatment of psoriasis, eye conditions, post-surgical abdominal scarring, acne, and deep skin wrinkles. The Starpharma group’s technology, based on novel, large molecular weight, star-shaped dendrimer molecules which are capable of multiple (polyvalent) interactions with disease-related target sites, is targeting viral diseases including genital Herpes (HSV-2) and Ebola virus, and cancer metastasis (breast and colon cancer). Thrombogenix Pty Limited is developing two new classes of anti-clotting therapeutic compounds. BresaGen Limited’s treatment for breast cancer is in phase I trials. To counter HIV/AIDS, Virax Holdings Limited is applying their platform technology, Co-X-Gene™, which derives from innovative work at the CSIRO and the John Curtin School of Medical Research. A vector, an unrelated virus harmless to humans, is used to deliver two separate stimuli to the immune system - the target antigen, against which an immune response is generated, and a cytokine, to stimulate the desired population of immune-responding T-cells or B-cells. A different tack is being taken by Narhex Operations Pty. Limited, with their HIV protease inhibitor that has undergone successful Phase II clinical trials. Among other vaccines being developed are two targeting human papillomavirus infection (linked with cervical cancer and genital warts), one for treatment (Cervax Pty. Limited) and the other for prevention (CSL Limited and Merck & Co., from University of Queensland research). CSL is also developing vaccines to prevent Helicobacter pylori infection (with AstraZeneca) and glandular fever (Epstein-Barr virus infection), the latter as a core project in the Cooperative Research Centre for Vaccine Technology. This CRC’s vaccine development programs also aim to combat melanoma, malaria, and streptococcal infection, and to develop more effective vaccination technologies. Bioproperties (Australia) Pty. Ltd., together with joint venture partner Nippon Medical Research, is developing a new class of narrow-spectrum peptide antibiotic for staphylococcus and mycobacteria, currently at late preclinical stage. Human health diagnostics Health diagnostics is also an area of particular strength, as illustrated by the following examples. PanBio Pty. Ltd. has an extensive range of diagnostics for infectious disease, such as Dengue Fever, Ross River Virus, Q fever, Japanese B Encephalitis, and Epstein Barr Virus. PanBio has just achieved the remarkable feat of a place on the Business Review Weekly “Top 100 Fastest Growing Companies” list for the seventh consecutive year. Another company targeting infectious and tropical disease diagnosis is Cellabs (Cel-labs Pty. Limited.), which produces diagnostic kits for chlamydial diseases, malaria, water-borne Giardia and Cryptosporidium parasites, opportunistic diseases associated with AIDS, and other tropical and emerging diseases such as leishmaniasis and amoebic dysentery. Several Australian companies have capitalised on the groundbreaking 1983 discovery by Western Australian researchers Robin Warren and Barry Marshall that the previously unknown bacterium Helicobacter pylori is the primary predisposing factor for peptic ulcers (infection also increases the risk of stomach cancer). Through a collaboration with the University of New South Wales, Diagnostic Technology Pty Limited has developed a specific immunodiagnostic test for H. pylori. Tri-Med International Pty Ltd produces two types of H. pylori diagnostic tests, one based on enzyme analysis and the other on radiolabel detection in the breath. Medical Innovations Limited produces diagnostic tests for cancer and cardiac disease and is trialling novel drug treatments for inflammatory diseases, notably psoriasis. Cell, tissue and biomedical engineeringAustralian companies are active in a wide variety of developments which can loosely be classified as cell, tissue and biomedical engineering. Stem Cell Sciences Pty Ltd (SCS) is working with embryonic stem cells which retain the ability to form all cell types found in the body for cell-based gene and drug screening, and future application in human cell-based gene and tissue therapies. BresaGen Limited is also developing stem cell therapies, for diseases such as Parkinson’s disease and Alzheimer’s disease, where the underlying cause is the loss of cellular function. Another BresaGen interest is transplantation of organs from other species to humans (xenotransplantation). Bio Nova International Pty Ltd. produces implantable three-dimensional tissue structures for the treatment of defective tissues and organs. Bio Nova was a pioneer of engineered tissues and was the first in the world to grow spare parts in animals for surgical repairs in humans. Applications include coronary artery bypass grafts lined with endothelial cells, heart valves, stents, ligaments, hernia repair patches, nerve regeneration tubes, dural patches, bioartificial skin, wound dressings, bone grafting materials, surgical sealant plus other constructs to enable grafting of pancreatic islet cells for the treatment of diabetes. Elastomedic Pty Ltd’s innovative polymer technology is being developed into new medical devices. The novel polyurethane polymer structures incorporate high levels of silicone in four formulations ranging from quite flexible to rigid. Drug deliveryThe pharmaceutical segment includes a number of companies developing innovative drug delivery methods. Examples are Acrux Limited, Soltec Research Pty Ltd (a subsidiary of F.H. Faulding & Co. Limited), Meditech Research Limited, Vapotronics Limited, Opsoma (Australia) Pty Limited (with a New Zealand parent), Inovax Ltd, Bioactive Enhancement Technologies Aust. Pty Ltd, Provalis plc (a UK company with a base in Western Australia), and Norwood Abbey Ltd. BiomedicalA significant number of biomedical companies were included in this analysis, including some prominent sleep apnea (apnoea) companies (ResMed Limited and Compumedics Sleep Pty Ltd), as well as companies producing heart assist devices and artificial hearts (Micromedical Industries Limited); cancer diagnostic imaging equipment (Polartechnics Ltd and Optiscan Imaging Limited); and other biomedical and scientific instruments. Inclusion of all of the large number of Australian medical and scientific instrument makers would have greatly increased the size of this pie slice in the Group 2 Figure. Other equipmentAustralian equipment companies are also playing a significant role in the profoundly important fields of genomics and proteomics. The Australian-owned, ASX-listed, Silicon-valley-based company Axon Instruments, Inc., for example, produces the GenePix microarray scanner and software for genomics. Corbett Research has developed an innovative real-time DNA-amplification instrument for the detection of genetic diseases, genetically modified organisms, and pathogens in water supplies. For proteome analysis, Advanced Rapid Robotic Manufacturing (ARRM) manufactures the Bio-Rad PROTEAN 2-D spot cutter, designed by ARRM and the Australian Proteome Analysis Facility, for Bio-Rad Laboratories, Inc. (USA). Clinical trialsAustralia is a very attractive location for clinical trials of new drug candidates, in terms of cost, regulatory climate, and time-frame. Among the companies involved are Australian companies such as Symbiotic Research Pty Limited, Clinical Network Services (CNS) Pty. Ltd., and Australian subsidiaries of overseas companies, including Synermedica Pty Ltd (recently acquired by Kendle International Inc.), Quintiles Pty Limited, Covance Pty Ltd, and ICON Clinical Research Pty Limited. Some overseas based biopharmaceutical companies have also set up subsidiaries in Australia which focus on clinical trials; examples are AMGEN Australia Pty Limited and Inotek Australia Pty Ltd. In vitro fertilisationAustralia is world renowned as a leader in this field since 1971. The Monash IVF Pty Ltd team has made many significant advances in the field of assisted reproductive technology, including the first frozen embryo birth in the world, the first donor egg baby in the world, and the world’s first birth from sperm retrieval aspiration. Other sectors Biotech agronomy Bio-Care Technology Pty. Limited over a decade ago launched NOGALL™, a novel biocontrol agent for crown gall disease, caused by a soil-dwelling bacterium and markets to the agricultural and horticultural industries. This product is a pure culture of a soil bacterium called Agrobacterium radiobacter, strain K1026, and is used for the biological control of crown gall disease in stone fruit trees, nut trees, caneberries, roses and various horticultural crops. The technology was developed at the University of Adelaide by Professor Allen Kerr’s team. The active agent, K1026, is historically important because it was the world’s first release of a live, genetically-engineered microorganism to the public. Bio-Care also released the first registered mycoinsecticide in Australia, called BioGreen Granules, a biological control effective against a pasture beetle scarab. Bio-Start Australia Pty Ltd makes a range of bacteriocin products for the agricultural industry, both animal husbandry, primarily the beef, sheep and dairy industries, and horticulture. Bacteriocins are antibiotic-like bacterial products which Bio-Start produces by fermentation in liquid form. Applications include arresting and inhibiting sclerotinia diseases of beans and apples, and combating botrytis and sour rot in wine grapes. Environmental biotechnologyThere is a considerable overlap between the “biotech agronomy” companies and environmental biotechnology companies such as Enretech Australasia Pty Limited. Enretech’s sorbents are designed for bioremediation of oil-contaminated sites and other hydrocarbon spills, and contain specialised bacteria within recycled cellulose fibres to actively digest hydrocarbon pollutants. A further large group of companies fall outside the bounds of biotechnology but in closely related areas of environment industries. EcoEarth Technologies, for example, has developed a range of innovative products for the food and mass catering industry, including plant-starch-derived, fully compostable pots, cutlery, and “plastic” bags. Other products being developed include onion bags, cotton buds, and disposable nappies. Mineral processingAustralian mining companies are using and trialling both Australian-developed and imported technology for biologically assisting the processing of minerals, particularly gold and nickel. Examples in bio-oxidative processing of refractory gold ores are Pro Micro International Pty Ltd and BacTech (Australia) Pty Ltd; copper and other base metal ores, BacTech (Australia) Pty Ltd; and nickel, QNI Pty Ltd’s BioNIC™ technology. Mining companies using bioleaching include QNI, Beaconsfield Gold N.L., Perseverance Corporation Limited, and Great Central Mines Limited. Paper and pulp industryIndustrial BioSystems Pty Ltd (part of the Biotech International Ltd group) has powerful biopulping and biobleaching technology to improve the processing of paper pulp. Plant micropropagation technologyTechnico Pty. Ltd. has developed a breakthrough method of producing large numbers of seed potato tubers rapidly and efficiently. The micropropagation method utilises pathogen-tested tissue culture. A rapidly expanding company, Technico is applying its TECHNITUBER® tuber technology into USA, Mexico, China, Thailand and India, and is about to introduce the technology into Europe. Among companies micropropagating plants for export are two companies with a particular focus on the Western Australian native plant, kangaroo paw: New World Flora Pty Ltd and Burbank Biotechnology Pty Ltd; and Florigene Limited (now a part of the Nufarm Limited group). Florigene produces flowers genetically modified to give novel colours and longer cut-flower shelf-life. Burbank Biotechnology and ForBio Plants Pty Ltd were recently acquired by Arthur Yates & Co Limited, and will be called Yates Botanicals Pty Ltd from July 2000. Genetically modified cropsGenetic modification of crops is an area of considerable strength in Australia, both in research and industry. The focus is on crops such as wheat, barley, potato, canola, cotton; pastures and forages such as alfalfa and clover; numerous fruits; and selected tree species, including eucalypts. As an example, Biowest Pty. Limited and the associated Grain Biotech Australia Pty Ltd are crop breeding and genetic transformation companies based in Perth. Another subsidiary, BioTest Pty. Ltd., is engaged in biological testing. Most companies have adopted a cautious strategy for commercialisation in the current adverse climate for public acceptance. Veterinary reproductionGenetics Australia is Australia’s largest artificial breeding organisation, focusing on innovative reproductive technologies, including R&D in animal cloning and transgenic animals, and in sperm fertility. Core business includes progeny-tested semen for artificial insemination of dairy cows. Genetics Australia unveiled the first calf cloned in Australia from developed cells on 2 May 2000. Camelot BioScience has entered a more unusual area pre-sexing camels for camel racing in the Middle East, using technology developed by molecular biologists at the University of Queensland, involving genetic detection and embryo transfer systems. Food diagnosticsCheckmeat’s immunodiagnostic kits distinguish meat from 12 animals: beef, sheep, chicken, pig, horse, buffalo, kangaroo, goat, donkey, rabbit, dog, and human. TECRA Diagnostics’ immunoassay kits are used to detect pathogenic bacteria and toxins in food, environmental, cosmetics and pharmaceutical samples. Platform technology - ProteomicsProteomics is the systematic study of the protein complement, or “proteome”, of an organism. The term “proteome” was coined in Australia in 1994 by Dr Marc Wilkins; the term has now become widely used throughout the world. Australia has continued to build its position in the forefront of proteomics, which parallels the related field of genomics. Proteome Systems Limited, a technology spin-out from Macquarie University, uses proteomics for drug discovery and developing novel proteomics technology and instrumentation. Proteome Systems’ major discovery program in partnership with Dow Agrosciences (USA) is at the forefront of agricultural biotechnology. Proteome Systems is planning to establish facilities in the USA, and recently announced a major new strategic alliance with Shimadzu Corporation to build instruments that will revolutionise high throughput screening of proteins. BioinformaticsThe human genome project, with similar genomics projects in other organisms, and proteomics, are together providing an explosion in information on a scale that is difficult to comprehend. A vital key to tackling this huge mass of information to unlock the secrets within is bioinformatics. Australia’s most prominent bioinformatics company, eBioinformatics Inc., is incorporated in the USA. eBioinformatics offers leading-edge bioinformatics tools and resources via the Internet, and subscription via e-commerce, to subscribers around the world. Emphasising low cost and user-friendliness, eBioinformatics provides simplified access to the latest analysis tools and genomic and protein databases, and also professional management of scientists’ data, tutorials and specialised assistance. Platform technology - BiosensorsAMBRI Pty Limited’s ion channel switch biosensor - the world’s first purpose-built, functioning nanomachine - was developed from CSIRO and Cooperative Research Centre research. The machine detects a wide range of molecular targets and is being commercially developed for screening of new drugs, for human and veterinary diagnostics, for the detection of DNA for research purposes, and for the detection of lethal bacteria in biological weapons. Genetic testingAt least 10 companies and a large number of units in hospital and research institutes have genetic testing as their main focus (see Group 1 table). Some focus on paternity and forensic testing, and others on identification of pathogens, varieties or breeds. A fast-growing area is testing for the transgene in genetically modified foods. Blood products and processingCSL Limited has established a state-of-the-art manufacturing facility to process blood plasma. Plasma-derived products from this plant are used in treatment of bleeding disorders, for emergency trauma situations such acute blood loss, and for preventing severe infections. The facility has the unique capability to process plasma from a country, and return it as finished products to the country of origin. An increasing number of countries in the Asia/Pacific region are using this facility, and agreement was recently reached with the American Red Cross to process US plasma for the US market. Producers of high-quality products derived from animal blood include Trace Scientific Limited, Moregate Exports Pty. Ltd., Starrate Pty Ltd, Gryphen Industries Pty Ltd (ABPM Division), and CSL. Also a manufacturer of proteomics equipment, Gradipore Ltd has an innovative and powerful new blood processing platform technology, called Gradiflow, that provides improved fractionation, dialysis and concentration of blood. Gradipore is exploring further applications, including viral decontamination and removal of unwanted substances from blood. The company recently announced a collaborative research agreement with Baxter AG, the establishment of a US subsidiary, and the FDA approval of its lupus anticoagulant testing products, the GradiPlasma LA range. Colostrum and milk productsAustralia’s extensive dairy herds are the source of scarce, therapeutic-grade colostrum and milk for a number of biotech companies, for example: GroPep Proprietary Limited, which manufactures and sells growth factors, antibodies and associated reagents. A particular focus for GroPep products is digestive tract diseases. Dairy whey is the source of growth factor extracts for the prevention of gut mucositis (in Phase II clinical trials) and chronic venous ulcers (Phase I clinical trials completed successfully). GroPep’s portfolio includes recombinant insulin-like growth factors (IGF) and antibodies to IGF and related proteins. Anadis Limited, which focuses on developing colostrum-derived antibodies and peptides into biopharmaceuticals for peptic ulcers, diarrhoea, and osteoporosis, and for use in blood perfusion cartridges for treatment of septic shock, drug overdoses, and postoperative haemorrhage. NorthField Laboratories Pty Ltd., which markets Gastrogard, a colostrum-derived treatment for prevention of rotavirus diarrhoea, as well as a sports supplement. Bonlac Foods Limited has developed a novel, dairy-derived ingredient, Recaldent™, for chewing gum that promotes healthier teeth by promoting remineralisation of tooth enamel (Australasian Biotechnology 9(5): 235 (1999)). Animal/fish nutritionIn 1996, International Animal Health Products Pty Ltd launched the first registered probiotic in Australia for use in animals and birds, Protexin Multi-Strain Probiotic. They have just released a range of probiotics for aquaculture, designed to control common bacterial and viral diseases and to reduce waste build up. Natural products, complementary medicines, and nutraceuticalsThis diverse area is a major focus for industry activity in Australia. There are many Australian manufacturers of high quality oils and extracts and related products, including those from

Australia is one of the few countries so richly endowed with biodiverse biota, both terrestrial and marine, that it is described as “megadiverse”. Organisations involved in bioprospecting, primarily for new biopharmaceuticals, include ExGenix Ltd., AstraZeneca R&D Griffith University (formerly the Queensland Pharmaceutical Research Institute), the Australian Institute of Marine Science (AIMS; in collaboration with Nufarm and AMRAD), Gryphen Industries Pty Ltd, and recently renamed Bioprospect Limited (with the new Centre of Phytochemistry at Southern Cross University, in the heart of NSW’s Cellulose Valley, see Australasian Biotechnology 10(2): 32 (2000). CONCLUSIONAustralian biotechnology and bioscience related companies have expanded significantly both in number and in scope of activity over the past five years, and now represent a significant force in Australian business and the economy. Importantly, there has been a big shift toward the production of manufactured goods and the conversion of research into marketed products and services. Also vital is the continuing emergence of new companies based on innovative research coming from public institutions. With this increase in activity has come experience, and Australian managers can claim skills and war stories comparable to any. However, biotechnology related industries world-wide are experiencing similar growth and excitement, and there is growing competitive pressure to meet expectations. Nurturing the sector is vital at this critical time in its development, to ensure that it rapidly becomes a major contributor to the Australian economy. Australian governments over the past ten years can claim some credit for the increased momentum but we still lag behind other comparable countries in industry and company growth and the extent of business expenditure on R&D. Australia has long considered itself to be distanced from other countries and therefore having to rely on new ideas in order to survive. This view must now be reversed as Australian companies project their ideas and products to the international markets. Strategic linkages are becoming critical ,and access to global markets and access to capital will directly influence the fortunes of companies. ACKNOWLEDGEMENTAn earlier version of this study was partially funded by the Canadian Government through the Canadian Consulate General in Sydney. 1. Fayle D (2000) The Australian biotechnology industry: its research base and impact on medicine. In: Biomedical, Biotechnology and Pharmaceutical Innovation: Australia’s Opportunities. CL Creations and Health Media Group, Sydney, pp 28-55; Thorburn L (1999) Ten trends in Australian biotech. Australasian Biotechnology 9 (3): 151-158; Ernst & Young / Department of Industry, Science and Resources (ISR) (1999) Australian Biotechnology Report 1999. Hillyard C (1999) The biotechnology industry in Australia. Australasian Biotechnology 9 (4): 203-205. 2. Ernst & Young /Department of Industry, Science and Resources (op. cit.) 3. Deloitte Touche Tomatsu, Parramatta (www.deloitte.com.au). Note that nine of the companies on the Deloitte Biotech Index (2nd edition) are not considered by us to be Group 1 dedicated biotechnology companies (Resmed, Polartechnics, Pharmaction, Micromedical, Genesis Biomedical, Cochlear, Clover, Chemeq, and Medicine Quantale - eight of these are in our Group 2) and two more have moved into areas no longer predominantly biotechnology: Inovax (now in Group 2, though several of its subsidiaries are dedicated biotechnology companies) and the former BioDiscovery. Copyright 2000 - Australasian Biotechnology The following images related to this document are available:Photo images[au00035f2.jpg] [au00035f3.jpg] [au00035f1.jpg] [au00035t1.jpg] [au00035f4.jpg] [au00035t3.jpg] [au00035f6.jpg] [au00035t2.gif] [au00035t4.gif] [au00035f5.jpg] [au00035t5.gif] [au00035f7.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}