|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

Australasian Biotechnology, Vol. 11 No. 5, 2001, pp. 25-30 BIOTECH TAXATION REVIEW “Growing Australian Biotechnology Through Improved Access to People and Capital”: Recommendations for Changes to Taxation Code Number: au01064 AusBiotech consulted over 100 of its industry members and biotechnology stakeholders over the past several months with the specific intention of determining taxation issues that are impeding the growth of the biotechnology sector in Australia. The purpose of the paper below is to highlight areas where Australian Taxation issues are inconsistent with supporting the growth of the Australian Biotechnology industry through the existence of a non-competitive financial environment compared to leading biotechnology countries. The resultant paper below outlines achievable and responsible solutions to enhance the Australian biotechnology industry’s ability to compete, grow, and mature into a sustainable and competitive industry. 1. Introduction The purpose of this Paper is to highlight areas where Australian Taxation issues are inconsistent with supporting the growth of the Australian biotechnology industry (The Industry) through the existence of a noncompetitive financial environment compared to leading biotechnology countries. Furthermore, this paper outlines achievable and responsible solutions to enhance The Industry’s ability to compete, grow and develop into a sustainable and world competitive, biotechnology industry. The Industry has the potential of providing very significant benefits to Australians through addressing major issues including:

AusBiotech consulted over 100 of its industry members over the last 3 months with the specific intention of determining the taxation issues that are impeding the growth of the sector in Australia. A theme, which was consistently emphasised during this consultative process, was the urgent need to foster and stimulate The Industry. This concept has achieved support through the Federal Government’s “Backing Australia’s Ability” National Biotechnology Strategy, the Federal Opposition’s “Knowledge Nation” Paper, and the release of several State and Territory Government (ie. Queensland, Victoria, South Australia, ACT, and New South Wales) Biotechnology Strategies. Australia has a good record, and is recognised internationally, for the quality of its biotechnology research, especially in medical and agricultural fields. This excellence in research has not been paralleled by achievements in commercialisation and exploitation. However, recently there has been a marked improvement in commercialisation in terms of the emergence of start-up companies due to increasing support from the Federal Government and several State Governments and an improving policy framework from the Federal Government. There is a greater understanding and awareness of the challenges facing emerging industries by researchers, industry and governments. The Industry applauds the introduction of the Pre-Seed Fund, the Biotechnology Innovation Fund, the Innovation Investment Funds and the continuation of the R&D Start Program. AusBiotech is building on these initiatives and is encouraging the Federal Government to examine and address several taxation issues specifically relating to the growth of the biotechnology industry in Australia. There remain a number of barriers impeding the development and growth of Australian biotechnology companies, with some of these applicable to other industry sectors. Two of the barriers identified during AusBiotech’s consultative process that would be relatively inexpensive to implement but would have a substantial impact on the Australian biotechnology industry are: i) Barriers impacting people (ie the ability to attract and retain skilled human resources to drive the growth of the industry); and ii) Barriers restricting access to capital. These two issues were identified as critical in AusBiotech’s Business Plan, entitled “Growing Australian Biotechnology”. They were further highlighted during AusBiotech’s consultative process that involved over 100 key biotechnology stakeholders throughout Australia. The issues were also identified by BIOCOG and in the Australian Biotechnology Report 2001 by Ernst & Young/Freehills. When addressing the challenge of dealing with the barriers to attracting skilled human resources and access to capital, it is essential to consider the inherent nature of The Industry that involves high elements of risk, long lead times to market, and the need to operate within complex regulatory regimes. For Australia to be part of the emerging world economy, in which biotechnology is playing an increasingly dominant role, we must, at the very least, adopt initiatives and incentives that bring Australia into line with other leading world economies, including taxation standards. Therefore, while many issues were raised during AusBiotech’s consultative process, this Discussion Paper focuses on 7 recommendations that, if addressed, will make a substantial difference to The Industry. 2. Background 2.1 The Australian Biotechnology Industry The Australian biotechnology industry is growing from a fertile base of high quality and innovative research, and in a diverse range of sectors. According to the Australian Biotechnology Report 2001, 47% of companies focus on human health (pharmaceutical, medical devices and diagnostics), with significant additional investments in genomics/ proteomics/bioinformatics (13%), agriculture (14%) and equipment/ services (14%). Recent reports have highlighted the growth and diversity of The Industry, identifying nearly 200 “core” biotechnology companies at the end of 2000, with projections of 224 companies by mid 2001 and 250 companies towards the end of 2001. Programs by Federal and State Governments, and an increasing recognition of the value of intellectual property from research providers, are the basis for the emergence and expansion of these companies. All governments are becoming more considered in their investment strategies and are recognising the potential of the biotechnology industry and the rewards that are possible from “innovation rather than imitation”. 2.2 Australian Biotechnology Companies The Australian Biotechnology Report 2001 highlights the importance of Universities, CSIRO and other publicly funded research organisations in contributing Intellectual Property (IP) to established and new Australian biotechnology companies. Nearly 50% of biotechnology start-up companies in Australia have developed technology from the founders of the company, rather than by “in-licensing”, with a further 26% being licensed from universities and CSIRO. Capital raising commences before a company is established by the founders and partners. Venture capital has been the primary source of funds at this stage with an increasing contribution from early stage private equity/angel funds. During this period, almost all biotech companies operate at a loss and usually do not break even for many years. Biotechnology companies, especially those focused on therapeutics and technology platforms, have long periods of research and development, and consequently need to form strategic partnerships during the development phase. 3. Tax Issues All specific and coordinated taxation based approaches to support and foster The Industry have relied on investment structures designed for more conventional industry growth. These traditional approaches are not always appropriate for the biotechnology industry given its high risk nature, long lead times to profitability, complex regulatory requirements, and the need for more sophisticated and complex financial structures required to encourage investment. 3.1 Recent Tax Reforms Recent tax reforms have provided welcomed and needed changes. These reforms and initiatives include: 3.1.1 R&D Tax Rebates The R&D rebate initiative, introduced to allow small loss-making companies to claim a tax offset in relation to certain expenditure incurred in relation to R&D, provides much needed cash flow to companies in the start-up phase of their business cycle. Broadening these provisions to include more biotechnology companies would assist in placing Australia at the forefront of this sector worldwide. 3.1.2 Scrip for Scrip Transactions The scrip-for-scrip rollover provisions make investment in Australian companies more attractive by allowing investors to defer the recognition of capital gains in certain prescribed circumstances. Such measures assist in attracting much needed capital investment in Australian business. Further broadening of these provisions would assist participants in the Australian biotechnology sector in attracting much needed capital. 3.1.3 Easing of Pooled Development Funds (PDF) Restrictions Measures introduced in relation to capital reductions and share buy backs have increased the attractiveness of PDFs as a vehicle for investing in the biotechnology sector. While we are already seeing the positive impact of this on Australian biotechnology companies, additional incentives will further stimulate investment. 3.1.4 CGT Initiatives The CGT initiatives introduced recently may lead to an improvement in the investment environment in Australia. While this initiative is a step in the right direction, further changes are required, at the very least, to bring Australia into line with other leading world economies in order to achieve the potential financial and social benefits that can arise from a truly vibrant biotechnology industry. Key strategies that have been successful in leading biotechnology countries, such as the USA include;

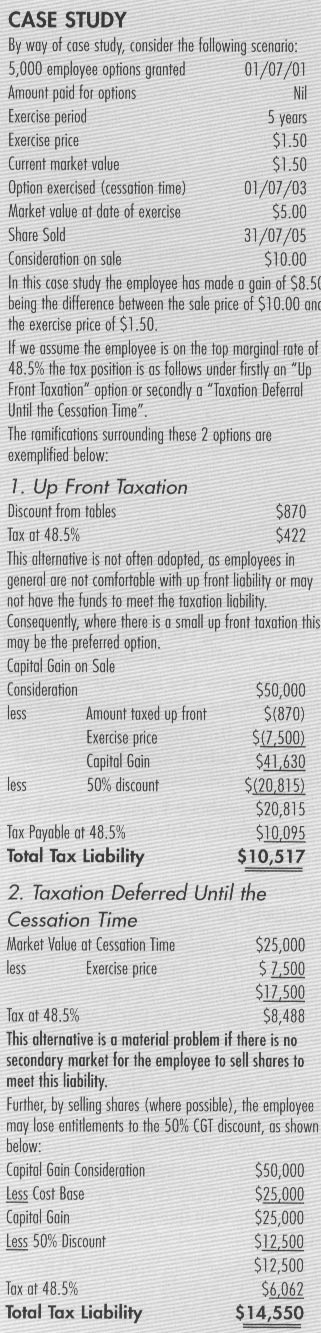

In some countries, including the UK, the rate of CGT decreases progressively the longer an investor holds shares and to a lower rate than the current Australian 50% discounted rates. Also, there is a trend worldwide for the rate to drop to an effective tax rate of 20% or lower. When this is taken into account with the long period (many years) that an earlystage investor must hold on to biotech shares before they can be traded, it becomes an important consideration to adopt changes to the Australian system which reflect the initiatives in the UK. For example, in the UK the CGT drops to an effective rate of 10% (as against the current Australian rate of as much as 24.25%) if the shares are held for 5 years or more. While not specifically designed for The Industry, some of the reforms mentioned above have resulted in a positive impact on the biotechnology sector. However, there is a significant way to go if the biotech industry is to achieve its full potential and deliver on its promise. Without further tax reform and initiatives, The Industry will not be able to be globally competitive, and therefore, development from its current embryonic state will be both slow and limited. 3.2 Proposed Changes to Taxation 3.2.1 Barriers Impacting People (ie. The ability to attract and retain skilled human resources to drive The Industry) As the Australian biotechnology industry grows, the need to recruit quality CEOs, researchers and senior business people to this sector, and to retain them, will also grow in parallel. At another level, there is a need to establish a “pool” of individuals, with the appropriate skills, to serve on Boards and Scientific Advisory Groups. Targeting qualified individuals, including Australians working and training in the USA, is one of the strategies being addressed by biotechnology companies in Australia. However, there are taxation provisions relating to pension plans, options plans, and employee share acquisition schemes that make employment within the Australia biotechnology industry less attractive to these key individuals. Pension Plans A frequent comment by US-based and Australian investors, and biotechnology professionals, is the unfair tax treatment of an individual’s pension plan should that person move to Australia. This is a major disincentive to key people, including Australian expatriates, who may be considering relocating to Australia on a permanent basis. One solution would be to introduce a tax free rollover of their pension plans into Australian superannuation funds. Options and Employment Share Acquisition Schemes The taxation problems associated with options plans and employee share acquisition schemes are now well documented and are a material concern for biotechnology companies. Under Division 13A of the Income Tax Assessment Act 1936, employees are generally given the choice between being taxed up front or at a later time referred to as the cessation time. After being taxed up front, the eventual sale of an option or share is generally dealt with under the CGT provisions. The obvious difficulty with Division 13A is that the employee under both alternatives often faces a taxation liability before a share is sold. As a result, the employee is often forced to sell shares to fund the taxation liability. However, because several years typically elapse from company establishment until a stock exchange listing or another form of liquidity is achieved, a secondary market for the share may not yet exist. Accordingly Division 13A should be amended to only have application where an underlying share or option is sold. It would also appear appropriate to ensure the 50% capital gains tax exemption is available to employees in these circumstances with the 12 month qualifying period for the 50% CGT discount running from the time the original option was granted or share acquired. Failing this core amendment there are a number of ancillary problems that could be addressed, such as:

The following case study exemplifies the tax liability of the 2 available choices, namely, being taxed up front or taxed at a later time, referred to as the cessation time. Notwithstanding the fact that up front taxation may ultimately realise a smaller taxation liability, it is unpopular with employees as they are not in a position to sell shares to fund the tax payment. Furthermore, there are often issues for employers in relation to lending money to employees to buy shares, which collectively can often make this option prohibitive. There are various permutations possible for handling share and option scenarios and therefore the case study below has been formulated to provide an overview of the 2 most common scenarios and the consequent tax liabilities which employees face. 3.2.2 Barriers that Restrict Access to Capital: Points frequently raised concerning “access to capital” during AusBiotech’s consultative process included: Direct taxation impediments of investment into the industry for emerging and mature biotechnology companies; and/or

Since the Venture Capital reforms (ie the Venture Capital Exemption - VCE - initiative) were introduced in November 1999, there has only been one major fund that has registered 21 separate VCEs and, of those registered, only one investment has been made. In relation to Taxation and related changes that are achievable, and will significantly boost The Industry, AusBiotech’s consultative process identified 3 key areas associated with access to capital that, if addressed, would greatly increase the access to capital and support the development of the Australian biotechnology industry. These three areas are: i) Broadening the Capital Gains Tax Rollover Relief Provisions; Each of the above 3 areas are addressed below together with suggested recommendations. (i) Broadening the Capital Gains Tax Roll-Over Relief Provisions The primary mechanism for investing in a company is to be issued with shares or to purchase shares. The purchase of shares is regarded as purchasing an asset for capital gains tax purposes. The amount one pays for the purchase forms the tax “cost base” of the share. Any disposal of that share will prima facie give rise to a capital gains tax liability if the sale price exceeds the cost base. Such a gain will most likely occur with a start-up company that is growing and developing valuable intellectual property. If the investor is an individual, that individual will have recourse to the 50% capital gains tax discount. If that investor is of retirement age, further capital gains tax relief may be available. An individual may also have recourse to the small business asset rollover that allows a taxpayer to defer the making of a capital gain from the disposal of shares in a company if the taxpayer acquires replacement shares within a one to two year time frame. This rollover is extremely limited, as it requires the individual to have a controlling interest in the entity of whose shares it is disposing. A capital gain is therefore crystallised only when a further disposal or other event occurs with relation to the replacement shares. The “concessions” identified above are limited in application to the circumstances of a biotechnology start up company in that they require the investor to be either of retirement age, or impose a very low maximum net assets threshold test. It should be noted that the $5 million threshold incorporates an associate-inclusive test so that the assets of the investor in addition to those of their spouse and associated companies would be included in calculating the requirement. If the investor is a small business (that is, its net asset value does not exceed $5 million), that small business will have recourse to a 50% capital gains tax concession. However, this concession is limited to small business, which traditionally does not fit the type of investors in biotechnology companies. It is highly unlikely that the profile of seed investors and venture capitalists would fit the requirements to obtain the various CGT concessions identified above. In contrast to the Australian system, the United States adopts a “prescribed industry approach” to its “Knowledge Industries” and permits a rollover of investments for CGT purposes so long as the replacement investment is also in a prescribed knowledge industry. For example, Investor A (a seed investor) invests $1 million in an IT company (“IT Co”). IT Co is included in the definition of “Knowledge Industry”. IT Co is registered with the equivalent body of the IR&D Board as a “prescribed knowledge industry”. IT Co has increased in value considerably since start up so that Investor A’s shares are now worth $5 million. Investor A sells his shares for $5 million crystallising a notional $4 million capital gain. In the US, if Investor A decides to reinvest his $5 million into another registered knowledge industry company the Tax Laws exempt Investor A from capital gains tax. He is able to reinvest the entire $5 million in another registered knowledge industry company. Investor A is only taxed when he ultimately realises his investment by electing not to rollover his investment again. In Australia, if the Seed Investor effectively controlled IT Co, and his net asset value did not exceed $5 million, then he would have received a partial exemption from his capital gains tax liability. However, as discussed above, these requirements are very unlikely to be met especially since many start-ups are funded by combinations of founders and high net wealth individuals. (ii) Ceasing to Tax Limited Partnerships as Companies A limited partnership is a partnership in which the liability of at least one partner is limited. For tax purposes in Australia, limited partnerships are effectively treated as companies. Because corporate limited partnerships are taxed as companies, there is no “flow-through”. That is, the income and capital gains of the Partnership are taxed in the hands of the entity rather than in the hands of the investors themselves. In the Background Material to the Final Report of the Innovation Summit Implementation Group titled “Innovation - Unlocking the Future” participants noted that the creation of a simple tax flow-through investment vehicle would stimulate investment in innovation by individuals and institutions. Venture capital entities are normally structured as trusts or partnerships because they are tax flow through entities. However, because partnerships have the risk of joint and several liability, they are rarely used in Australia. While limited provide no real benefit at the early stages of a company’s life. Furthermore, the ability to recoup such losses could be jeopardised in the future if there is a change in ownership of the company. For example, individuals investing in a limited partnership are unable to benefit from the CGT concession of 50% on the disposal by the partnership of any CGT assets. Furthermore, tax losses are trapped in the limited partnership and cannot be accessed and utilised by the individual partners. In the US, limited partnerships are tax flow-through vehicles and are used as the vehicle of preference for venture capital investors. Therefore, the tax laws that treat such corporate limited partnerships as companies should be reformed along the US model to enable tax flow-through. (iii) Expanding the Eligibility of the R&D Tax Rebate and the Premium R&D Concession At present, most companies undertaking eligible R&D expenditure would have recourse to the 125% R&D tax concession, which effectively offsets the company’s tax liability. For example, Company A has taxable income of $100. It has R&D expenditure of $100. Company A’s net tax position is that it has a $25 excess deduction, which then becomes a carry forward revenue tax loss. However, as most start up companies in the biotechnology sector do not become tax positive for a number of years, these carry forward tax losses provide no real benefit at the early stages of a company’s life. Furthermore, the ability to recoup such losses could be jeopardised in the future if there is a change in ownership of the company. In light of the above limitations associated with the R&D tax concession, the Government has recently passed legislation that will effectively give a cash refund for R&D expenditure rather than a tax concession. In order to be eligible, companies must have turnover (revenue) of $5 million or less per annum and an R&D spend of $1 million or less per annum. A “tax credit” (refund on R&D expenses) of 37.5c in the dollar (based on the 175% R&D Concession Rate) provides, for example, a $375,000 refund on a $1 million R&D spend. The prospective benefit for companies undertaking substantial R&D spending is very limited due to the above prescribed ceilings. According to the Australian Biotechnology Report 2001, the average R&D spend for private and unlisted core biotechnology companies for 2000-2001 is estimated to be $3.3 million and projected to increase to $4.4 million in 2001/2002. This average spend far exceeds the $1 million ceiling set under the provisions recently enacted, and thus is unlikely to benefit the bulk of biotechnology start-ups that were intended to benefit from the cash rebate. As part of Backing Australia’s Ability, the Federal Government introduced a 175% R&D Tax concession “premium” for additional R&D that was allowable under certain conditions above a threeyear R&D base. This premium only relates to labour-related components of R&D. R&D expenditure on plant depreciation or leasing as well as that required for the access of core technology is excluded. Consultations during the preparation of this Tax Paper identified the tax disadvantages of companies that were not yet profitable but had R&D expenditure or turnover (revenue) above the ceilings set for the tax credit initiative. These disadvantages could be addressed through extending the scope of the 175% premium R&D tax concession in a variety of ways, such as:

3.3 Other Considerations to Boost the Australian Biotechnology Industry Several other issues and suggestions arose during AusBiotech’s consultative process. Three points that were made on several occasions and therefore are worthy of consideration are as follows: 3.3.1 Broadening the Pooled Development Fund (PDF) Rules: The PDF program was introduced in 1992 under the Pooled Development Funds Act 1992 (“PDF Act”). A PDF is a company that raises capital from investors and invests this capital in small-to-medium sized enterprises (“SMEs”). PDFs and investors in these funds receive concessional tax treatment. The taxable income of a PDF is calculated the same way as for other companies. However, the regulated taxable income of a PDF is taxed at 15%. PDF dividends are exempt from income tax and dividend withholding tax, although resident shareholders may elect to receive franked dividends. Any taxpreferred income received by a PDF retains its character when it passes through to shareholders. That is, where income that has not been subject to tax is distributed to shareholders, it remains tax-free. Furthermore, capital gains made by investors in selling their shares in the PDF are exempt from capital gains tax. PDFs can invest in SMEs with total assets of less than $50 million, whose activities are not retail operations or property development. A PDF is able to invest in an SME for the following purposes:

Some restrictions under the present PDF regime are as follows:

Recently, a prominent Australian PDF determined to invest in a US entity that owned certain technology that it deemed critical to its future success. Due to the restrictions discussed above, if it invested in the US Company, it would have risked its PDF status. Therefore, amendments to the PDF Act dealing with the above restrictions need to be considered in order to encourage increased take up of PDF’s as an appropriate investment vehicle. This consideration could be addressed through the introduction of legislation in relation to PDFs aimed specifically at the issues faced by investors in the startup phase of biotechnology companies. Current PDF legislation provides no protection against the potential down side risk associated with such investments. While an investor whose investment increases in value gains access to tax free capital gains and concessionary taxed income, no mechanism exists for an investor who makes a loss on their investment to utilise that loss against another investment income. Due to the level of business risk associated with the early stages of biotechnology ventures, such losses are common. 3.3.2 Intellectual Property (IP) Amortisation: The provision for the amortisation of Intellectual Property (i.e. write-down) in Australia is not competitive with international standards. Therefore, Australian companies, and consequently investors in IP, do not have the ability to write-off the value of IP (as an asset), a situation that is a disadvantage to Australian companies seeking investment to generate or acquire IP. Generally, the “write-off” level hasn’t changed for many years and, consequently, Australia is well behind other countries. This was evidenced by commentary in the Review of Business Taxation report commissioned in December 1998 entitled ‘An International Perspective - Examining how other countries approach business taxation’, in which the significantly more concessional tax treatment afforded to patents and goodwill write-offs by countries such as the United States, the United Kingdom and Sweden is shown. This consideration could be addressed by revising the amortisation provisions of Intellectual Property (i.e. write-down) in order to be competitive with international standards so that biotechnology companies have the ability to write-off the value of IP (as an asset). This will enhance their ability to attract investment into the development and acquisition of IP. 3.3.3 Cut-In Point for Maximum Income Tax Rate In order to be competitive and bring Australia into line with leading world economies, consideration must be given to a higher salary at which the maximum income tax rate cuts in. In the US, this figure is US$150,000, which is approximately 5 times the cut-in figure in Australia. The low cut in point in Australia really acts as a disincentive for people to earn more and of course discourages people to relocate to Australia from more “tax friendly” places. Obviously this is not a biotech-specific problem, but would have a significant impact on the Australian biotechnology industry, as well as other Australian industries. Acknowledgments AusBiotech would like to sincerely acknowledge the contribution made to this Taxation Paper by in excess of 100 AusBiotech members and biotechnology stakeholders throughout Australia. In particular, we would like to express a note of special thanks to Ernst and Young (Keith Hardy, Chris Ball, Eddie Pegoraro, and their colleagues at EY) and PriceWaterhouseCoopers (Tony Stephen and his colleagues at PWC) as well as Mark Santini from MLS Medical for the time they devoted to reviewing the several drafts of this document leading to the final version.

Copyright 2001 - AusBiotech |

| |||||||||