|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

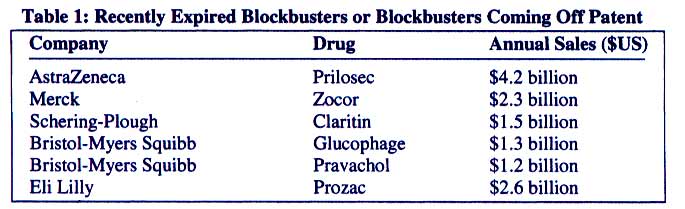

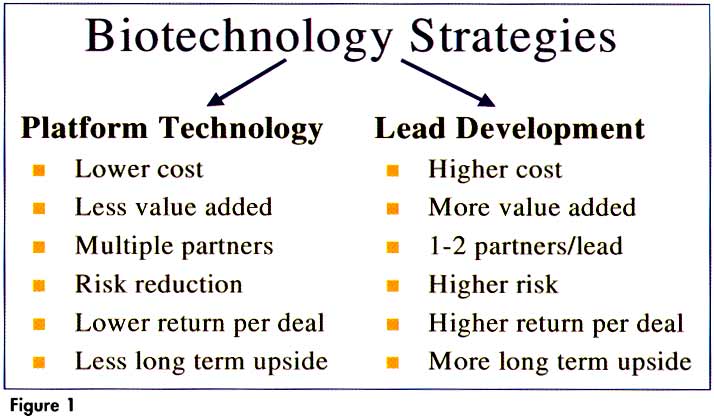

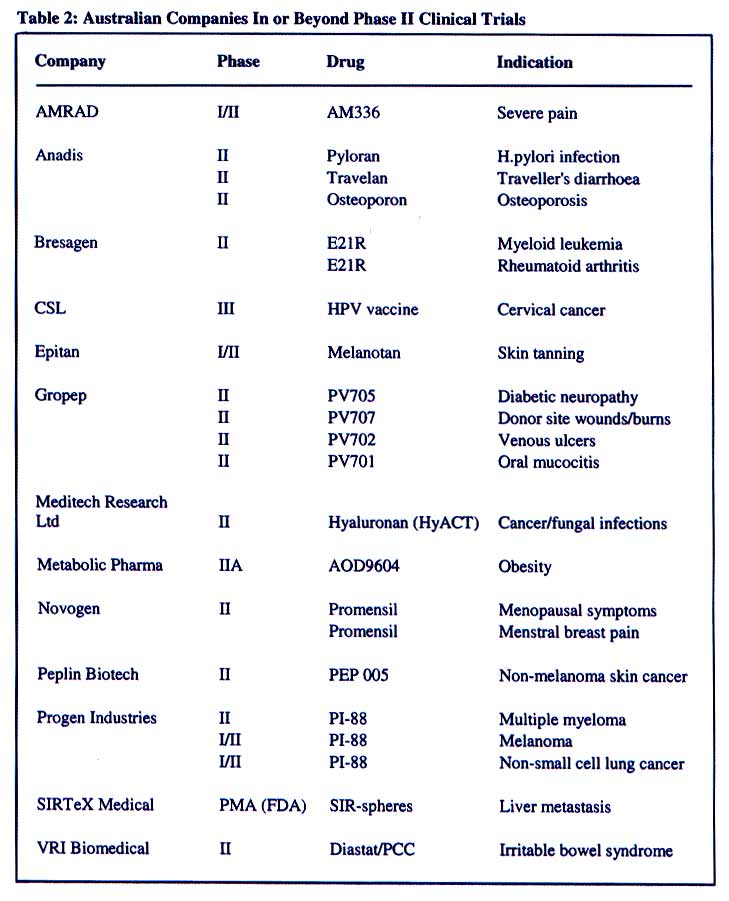

Australasian Biotechnology, Vol. 12, No. 4, Aug-Sept, 2002, pp. 52-53 PHARMACEUTICAL DEVELOPMENT WHY BIOTECHNOLOGY AND PHARMACEUTICAL COMPANIES ARE WORKING TOGETHER Peter Devine PhD MBA, Vice President Business Development, Progen Industries Ltd, Director, AusBiotech Ltd Code Number: au02027 Historically, pharmaceutical companies managed the entire drug development and production process, from inception to final product. However, today 20-30% of new drugs are biotechnology-derived, and over half of the drug leads undergoing preclinical or clinical research have been developed by biotechnology companies. So what has changed? The pharmaceutical industry is facing a number of issues: 1. Sluggish sales growth. 2. Product life cycles are becoming shorter. 3. R&D productivity is falling. 4. Increasing number of blockbuster drugs coming off patent. 5. Consolidation has its problems. As major pharmaceutical companies struggle to achieve organic growth in a highly competitive global market, they are increasingly relying on merger and acquisition (M&A) to achieve market share. GlaxoSmithKline (GSK) and Astrazeneca are examples of such activity. Examples from last year include Amgen's acquisition of Immunex for US$16 billion, J&J's acquisition of Alza for US$12.3 billion, and Bristol Myers Squibb's acquisition of Du Pont for $7.8 billion. This trend is continuing, with pharmaceutical giants GSK and Bristol Myers Squibb, and Pfizer and Pharmacia recently announcing M&A discussions. Unfortunately, consolidation creates a new set of problems, and it becomes increasingly difficult to innovate in a large multinational organisation. Consequently, pharmaceutical companies have been confronted with the need to increase dramatically the number and quality of drugs being released, and they have turned to biotechnology for new products and innovations. As a result, many pharmaceutical companies now spend 20-30% of their R&D budget on alliances with biotechnology companies. In many cases, pharmaceutical companies outsource discovery and early-stage development to biotechnology companies to allow their own enterprise to focus on downstream activities such as manufacture, clinical development, regulatory compliance and marketing. The total value of alliances between biotechnology companies and major pharmaceutical companies has increased steadily over the past five years. Alliance revenues were up 17% to more than US$2.8 billion at the end of 2001 - the fifth consecutive annual increase (Recombinant Capital, 2002). Australian biotechnology companies are also sharing in these deals, and alliances with international partners have risen from 38% in 1999 to 53% in 2001 (Ernst & Young Biotechnology Report, 2001). Biotechnology companies involved in drug development have traditionally employed two strategies - developing platform technology or lead drugs. These approaches are compared in Figure 1. In terms of alliance deals worldwide, the platform-technology strategy has been the preferred option. This strategy reduces risk through multiple licensing partners and provides for earlier cash flow. In 2001, technology platform companies pulled 63% of alliance revenue (genomics, chemistry, gene therapy, screening), while disease-based alliances (cancer, infection) made up 29% (Recombinant Capital, 2002). However, this trend has been changing on an international scale, with many platform-based biotechnology companies rediscovering themselves as lead-development companies - Celera, Human Genome Sciences, Millenium and Incyte being more notable examples. In fact, genomics companies have laid off more than 1500 staff since January 2001 (GenomeWeh, 2002). In terms of pharmaceutical development, Australian companies pursuing platform technologies include Alchemia, Progen Industries, Bionomics and Autogen. Alchemia's technology platform, known as Versatile Assembly on Sugar Templates or VASTTM produces carbohydrate-based combinatorial chemistry libraries. Progen received a START grant in 2001 to develop a technology platform based on chemical scaffolds (glycomimetics) that allow the design of drugs that inhibit heparan sulphate binding proteins. Bionomics is using its platform technologies of wholescreening, linkage analysis, positional cloning, gene functional studies, high-throughput mutation analysis and DNA microarray to identify genes which can be used as validated drug targets for the development of new drugs. Like Bionomics, Autogen is also focused on genomics platforms. However, these companies plan to use these platforms not only to partner with other companies, but to also feed their own development pipeline. Despite the majority of international alliances being based on technology platforms, big pharmaceutical companies are shifting their focus toward disease-based (lead-driven) alliances to feed their pipelines (Windhover, 2002). A number of Australian companies are focused on a lead-development strategy (Table 2). Most aim to take leads through to the end of early stage (Phase I/Il) clinical development, and then partner with a large international pharmaceutical or biotechnology company to take the drug through Phase III trials, regulatory approval and onto the market. Successful partnering, development and marketing of at least some of these leads is crucial to the success of the Australian biotechnology industry in terms of investor confidence and credibility. References

Copyright 2002 - AusBiotech The following images related to this document are available:Photo images[au02027t2.jpg] [au02027f1.jpg] [au02027t1.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}