|

African Crop Science Journal

African Crop Science Society

ISSN: 1021-9730 EISSN: 2072-6589

Vol. 9, Num. 3, 2001, pp. 549-565

|

African Crop Science Journal, Vol. 9. No. 3, pp. 549-565

GENDER CHARACTERISTICS OF RURAL FINANCIAL INSTITUTIONS

IN UGANDA

IJOYI FENDRU* and E. ADIPALA1

Department of Agricultural Economics, Makerere University, P.O.Box 7062,

Kampala, Uganda

1Department of Crop Science, Makerere University, P. O. Box 7062,

Kampala, Uganda

Received 12 March, 1996

Accepted 10 October, 2001

Code Number: cs01074

ABSTRACT

The objectives of this paper are to describe the types and

socio-economic characteristics of rural financial institutions in Uganda and

to describe gender differences between men and women in the use or non-use of

these institutions (services). The paper first gives a brief description of

the sample, and this is followed by background social, economic, and demographic

characteristics of respondents. There then follows a discussion of the use or

non-use of financial institutions by respondents, and respondents' perceptions

about using financial services. Subsequently, there is a description of the

characteristics of informal financial services such as borrowing, lending, saving

and deposit activities, and the characteristics of informal financial groups

(IFGS). Finally, the implications of the findings are discussed.Of the total

respondents interviewed (527), 66 percent were women. Only 11 and 15% of women

and men had bank accounts. A higher proportion of rural men (57%) than women

(52%) borrowed from informal sources. The fundings indicate that there is limited

access to and low level use of rural finances by both men and women. Most rural

people tend to hold their savings in the form of non-monetary assets, but women

tend to have greater ability and propensity to save than men.

Key Words: Gender differences, rural financing, Uganda

Résumé

Les objectifs de cet article étaient de décrire les types et las

caractéristiques socio-économiques des institutions financières

rurales en Uganda et définir des differences entre les hommes et les

femmes dans l'utilisationn et la non-utilisation de ces institutions (services).

L'article donne en premier lieu une brève description d'un

échantillion, puis suivi d'une information sociale, économique

et les caractéristiques démographiques des respondants. Ensuite

une discussion sur l'utilisation et la non-utilisation des institutions

financières par des respondants et enfin des perceptions des respondants

sur l'utilisation des services financiers. Ensuite, il y a une description

des caractéristiques des services financiers informels tels que les emprunts,

les prêts, les épargnes et des mouvements de dépots et des

caractéristiques des groupes financiers informels (IFGS). Finallement,

des implications de ces résultats sont discutées. Sur le total

des repondants interrogés (527), 66% étaient des femmes. Seulement

11 and 15% des femmes et des hommes respectivement avaient des comptes en banques.

Une proportion importante des hommes ruraux (57%) plus que les femmes (52%)

empruntaient à partir des sources informelles. Les résultats montrent

qu' il ya des limites d'accès au bas niveau de l'utilisation

des finances rurales ensemble pour les hommes et les femmes. La majorité

de la population rurale a tendance à maintenir leurs épargnes

sous forme des avoirs non monétarisés, cependant les femmes ont

tendance à avoir une grande capacité et une expansion des épargnes

plus que les hommes.

Mots Clés: Differences de sexe, financement rural, Uganda

INTRODUCTION

Most of sub-Saharan Africa is in a crisis, with a majority of the population

living below poverty level. Recent financial reform programmes, especially

those spearheaded by the World Bank and International Monetary Fund, which

have "liberalised the economies", have tended to impact negatively on rural

development programmes, making the rural poor, poorer (Crook and Manor, 1994).

Carr (2001) describes the case of Malawi where as a result of financial reforms,

fertiliser subsidies were removed, and maize production, the main food staple,

declined by nearly 30%. The main victims were the rural population, who depend

on agriculture for a living, and the urban poor, who depend on maize for food.

To make matters worse, most of the reform programmes and formal banks (Hubner

and Fischer, 1992; World Bank, 1993) have tended to focus on urban areas,

leaving the burden of uplifting the rural communities to Non-Governmental

Organisations (NGOs) and resourcefulness of the rural communities. The biggest

bottlenecks though, is the absence of strong financial institutions, such

as banks, to support rural transformation programmes. Inevitably, the rural

communities rely on informal banking systems to fund their sustainance and

development.

Informal financial intermediaries (IFIs) provide alternative financial services

to the great majority of rural people who have virtually no access to formal

institutions. IFIs in Uganda comprise of both individual and group agents.

Individual intermediaries include relatives, friends, neighbours, and merchants,

while informal financial groups consist of savings groups and rotating savings

and credit associations (ROSCs). However, the gender characteristics of these

groups have not been well described, although it is known that women tend

to have more informal financial intermediaries.

In this paper we examine the role gender plays in operation of the informal

financial institutions, and whether or not this has any bearing on the abilities

to save and invest in Uganda. Based on the outcome of the study, we explore

possible policy interventions

.

Methodology

The data used in this paper were collected from an exploratory survey of a

stratified random sample of 527 respondents in the districts of Arua and Mukono

in Uganda during the 1992/93 agricultural season. Arua is situated in the

North-western region on the Democratic Republic of Congo (DRC) and Sudan borders,

nearly 500 kilometres from the capital city of Kampala while Mukono is located

in the Central region only 25 kilometres from Kampala. These two districts

were selected because they exhibit contrasting characteristics with respect

to agro-ecological conditions, farming systems, predominant ethnic groups,

degree of rurality, availability of communications services, access to markets,

and level of economic development.

Twenty two villages (11 from each district) were randomly selected for the

study. The size of the population of the survey villages varied widely from

as few as 167 residents to as many as 3,124 people with a standard deviation

of 800 and a mean and median of around 1,600 people. Also, the total sample

of 527 respondents were more or less equally divided between men (53 percent)

and women (47 percent). The equality in the sample was achieved through a

process of random proportional gender sampling at the household level.

The sample was dominated by two major ethnic groups: the Lugbara in Arua

and Baganda in Mukono. The Lugbara comprised nearly 50 percent (257) of the

entire sample, while the Baganda accounted for another 32 percent (170). Together,

the two ethnic groups constituted 82 percent of the total sample, and the

remaining 19 percent consisted of minor groups including Basoga (6 percent),

Kakwa (2 percent) and others (11 percent).

RESULTS AND DISCUSSION

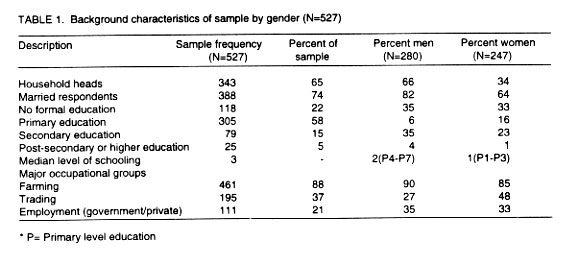

Background socio-demographic chara-cteristics of the respondents. Of

the total number of household heads (343) interviewed in this study, 66 percent

were male and 34 percent female (Table 1).

Previous studies (e.g., Jiggins, 1989) done in sub-Saharan Africa (SSA) have

estimated the proportion of female headed households to be around 30 percent.

About three-quarters (74 percent) of the sample were married, 82 percent (n=280)

of the male respondents were married men compared to 64 percent (n=247) married

women (Table 1). Contrary to popular

misconception, more than two-thirds (68 percent) of the married couples were

monogamous, whereas a relatively small proportion (32 percent) were polygamous

marriages.

The survey identified three broad occupational categories into which respondents

were grouped: farming, trading, and wage employment in the public or private

sector. These are, however, not mutually exclusive and exhaustive categories,

as a good number of respondents simultaneously engaged in two or three main

occupations in varying degrees. As shown in Table

1, the greatest proportion of respondents (88 percent) who reported farming

as a major occupation also mentioned trading and wage employment as their

other main economic activities. Similarly, another substantial percentage

of respondents (37 percent) who mentioned trading as their main source of

income were simultaneously engaged in farming and wage labour. The remaining

21 percent of the respondents said they worked as wage earners as well as

performed farming and trading activities to supplement their wages. Of the

total sample (n=527), 239 (45 percent), 28 (5 percent), and 20 (4 percent)

of the respondents reported farming, trading, and wage employment, respectively,

as the primary sources of income for their households.

A slightly higher proportion of male respondents (90 percent) were involved

in farming as their primary occupation as compared to female respondents (85

percent). Likewise, the proportion of men who were involved in wage employment

as one of their major sources of income (35 percent) is close to that of women

respondents (33 percent) who were also in the same occupation (see Table

1). Other studies (e.g., UNICEF, 1989) have estimated the proportion of

women employed in the middle and lower levels of the formal sector to be much

lower (as low as 16 percent). On the other hand, the proportion of women respondents

(48 percent) engaged in trading as one of their major activities is twice

that of men (27 percent) and also much higher than the overall percent of

respondents who (37 percent) are in that category (Table

1). This is primarily due to lack of diversification and specialisation

of economic activities.

With respect to educational background, respondents were grouped into four

categories: those who have had no formal education (22 percent); those with

primary education (P1-P7) (58 percent); 15 percent of the respondents had

attained secondary education (S1-S6); and 5 percent had completed post-secondary

or higher education. However, 46 percent of the 305 respondents who had gone

to primary school dropped out before completion and a mere 11 percent actually

managed to pass the Primary Leaving Examination. Even fewer respondents (20

percent) had gone through secondary and higher education.

The survey found that women without formal education out-number men in the

same category by a ratio of 3:1. In addition, the proportion (52 percent)

of men who had acquired some primary education was substantially higher than

that of women (42 percent). Likewise, fewer women (8 percent) than men (14

percent) had completed primary education. This means that nearly 80 percent

of the female respondents had no or little formal education compared to 68

percent of the males. Worse still, fewer than 10 percent of women had completed

primary education compared with 17 percent of men. The proportion of women

(2 percent) who had gone through higher education at the time of this study

was also much lower than that of men (7 percent) (Table

1).

These results compare well with those published by the 1988-89 Uganda Demographic

and Health Survey which reported that 40 percent of the women respondents

had never been to school in addition to 43 percent with only some primary

schooling. It also indicated that less than 20 percent women had secondary

education and even much fewer still (3 percent) went beyond this level (Uganda

Ministry of Health, 1989). Nationally, more than 50 percent of all women in

Uganda have never gone to formal school. The rate of illiteracy and innumeracy

is 50 percent higher among women than men (UNICEF, 1989)1.

Gender differences become even more revealing when we consider rural-urban

statistics in education. The proportion of respondents in rural areas without

formal education (25 percent) was found to be 5 times higher than that in

urban areas (5 percent). Interestingly, the proportions of rural men (71 percent)

and urban women (70 percent) with some primary education are very close. However,

the picture is different when we compare higher levels of education. The proportion

of women with secondary (25 percent) and post-secondary education (8 percent)

are considerably higher than those for rural men who have been to secondary

school (14 percent) and higher institutions of learning (4 percent). Likewise,

the proportion of female respondents who have had no formal education in rural

areas (40 percent) is much higher than that for women without formal education

in urban centres (98 percent). Furthermore, 25 percent of urban female respondents

have been to secondary school, compared with only 11 percent of the women

with secondary education in rural areas. This means that at the time of this

study, the rate of illiteracy and innumeracy was much higher among rural women

than men.

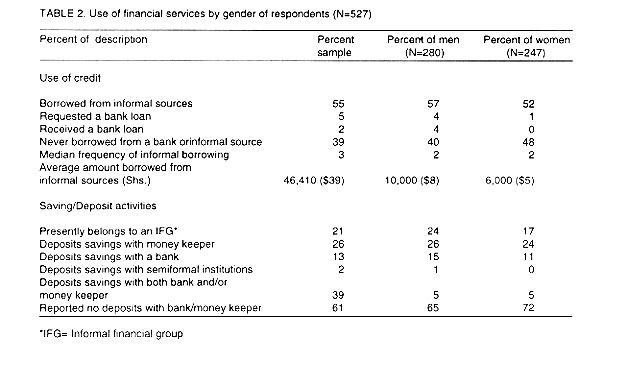

Respondents' use of financial services. Table

2 shows that few rural people actually make use of formal or semi-formal

financial institutions, particularly banks. For instance, the survey found

that only 13 percent and 2 percent of the respondents, respectively had accounts

with banks and semi-formal financial institutions such as credit unions. The

proportion of women who had bank accounts (11 percent) is smaller than that

of men with bank accounts (15 percent). There were no female respondents with

accounts in semi-formal financial institutions. The proportion of respondents

who had asked for a bank loan in the past is small (5 percent). Fewer women

(1 percent) than men (7 percent) have ever requested for a bank loan. Only

about 48 percent of the few respondents who applied for bank loans were successful.

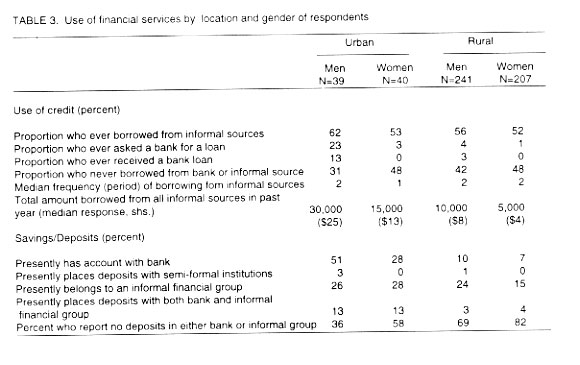

Male and female respondents in both rural and urban areas also exhibit substantial

differences with respect to loan and saving characteristics. As shown in Table

2, there is a higher proportion of rural men (57 percent) than rural women

(52 percent) who reported ever having borrowed from informal sources. While

13 percent and 3 percent, respectively of the urban and rural men who applied

for formal credit were successful, no women applicant in rural or urban areas

received any bank loan (Table 3).

It is also evident from Tables 2 and

3 that there were proportionately more

male than female respondents who participated in saving and deposit activities

both in rural and urban areas. Clearly, a large percentage of the respondents

do not use formal or semi-formal financial institutions. Thus, 87 percent

and 98 percent of the total sample respectively reported no bank deposits

and no bank borrowing. Similarly, the great majority of men (85 percent) and

women (89 percent) had no bank accounts.

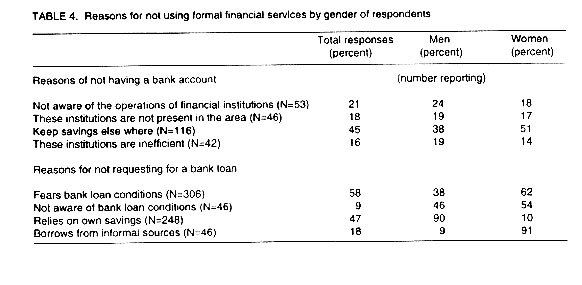

When asked why these respondents had no bank accounts and no bank loans, they

gave several explanations for this. A substantial proportion (45 percent)

of non-bank customers reported they had no bank accounts because they kept

their savings with informal money keepers (Table

4). This explanation was given by a much higher proportion of women (51

percent) than men (38 percent). About a quarter of the respondents (21 percent)

confessed that they did not understand the operations, conditions, and uses

of banks. This response was given by fewer women (18 percent) than men (24

percent). About less than a fifth (18 percent) of the respondents pointed

out that neither banks nor credit unions were present in their areas. Another

16 percent of the respondents said they feared to deal with these institutions

because the latter are inefficient, ineffective, corrupt, and serve only certain

groups.

The majority of the respondents (58 percent) did not request for a bank

loan because they were afraid of commercial loan conditions. Surprisingly,

the proportion of men who feared bank loan conditions (75 percent) is substantially

higher than that of women (62 percent) who gave the same response. Further,

47 percent of the respondents (35 percent and 42 percent of men and women,

respectively) did not borrow from banks because they relied on their own personal

or domestic savings. Another important explanation for not applying for a

bank loan was the lack of awareness of loan conditions. This was reported

by 8 percent of all non-users (16 percent men and 29 percent women).

From the foregoing results, it follows that a very large part of the agricultural

sector neither depends on formal financing nor benefits from it. Reports on

formal financial institutions in Uganda (e.g., Hubner and Fischer, 1992; World

Bank, 1993) indicate that commercial banks in the country have historically

focused on the provision of short-term credit for financing the processing

and marketing of export crops and external trade, while leaving development

finance and long term loans to the so-called development banks, which lack

the necessary capacity.

Banks lack interest in rural areas because they often claim that rural people

do not have the capacity to save and deposit with them. They fear that they

cannot make lucrative profits in these areas due to high transaction costs

of doing business there. Overall, commercial banks have made minimal contribution

to crop finance. For example, in 1989 agricultural credit accounted for only

5 percent of the monetary agricultural GDP and a mere 2.3 percent of the total

agricultural GDP (Yaron, 1990, 1991). The bulk of this credit was provided

by foreign donors and most of it went to finance export crop processing and

marketing and the remainder was used for production finance. For example,

in 1989 processing and marketing credit accounted for 38 percent of the monetary

cash crop agricultural GDP. Between 60 percent and 80 percent of the share

of total crop finance consisted of marketing credit (Yaron, 1990).

A lion's share of the crop finance was advanced to the Coffee Marketing

Board (CMB), co-operative unions, and private processors to handle coffee

processing and marketing. In contrast, in the same year crop production finance

accounted for only 1 percent of the monetary food crop agricultural GDP. According

to Yaron (1990), the high and increasing share of crop marketing finance tends

to be a reflection of the low turnover and inefficiency of credit.

Several factors are responsible for the minimal use of formal finance by

the poor. The most critical of these include the location of financial institutions

in distant urban centres which are far away from potential customers in rural

areas; high borrowing and lending transactions costs; prohibitive bank loan

collateral requirements; the preference of banks to put their funds in more

secure investments that yield profitable and dependable returns; risks associated

with carrying out financial transactions with a large number of poor customers

who are widely scattered in rural areas which are not easily accessible; lack

of public confidence in banks arising from currency depreciation and escalating

inflationary pressures that caused serious losses of income and liquid assets

across social groups; and the rather poor viability of the financial institutions

themselves due to poor infrastructure, lack of managerial capacity and liquidity

crisis. Overall, the financial system has a weak infrastructure with a sparse

branch network, poor deposit facilities, a small volume of undiversified transactions,

instruments, and products. The cost of intermediation for the entire financial

system is estimated to be as high as 24 percent of the overall transactions

costs (World Bank, 1993). In addition, it is extremely difficult for financial

institutions to plan meaningfully, as statistics are woefully lacking and

unreliable when available. The military, political, and social upheavals that

afflicted Uganda in the 1970s and 1980s led to decimation of the data base

and records, thereby leaving large gaps in statistics.

Respondents' perceptions about financial services. Respondents

were first asked to express how concerned they were about getting into bank

debt through commercial borrowing. The majority of the respondents (75 percent),

i.e., 72 percent men and 78 percent women expressed great concern about bank

debt. These high proportions are indicative of people's unwillingness

to obtain commercial credit because they fear to get into debt. There was

just about an equal proportion of men (12 percent) and women (13 percent)

who indicated that they were somewhat concerned with bank debt. However, the

proportion of male respondents who claimed that they were not concerned about

bank debt (15 percent) was slightly higher than that of women (11 percent)

in the same category.

Respondents were further asked to indicate specific attitudes regarding

borrowing chances from commercial banks, use of credit, and bank debt. The

responses were pre-coded on a three-point Likert scale and the results are

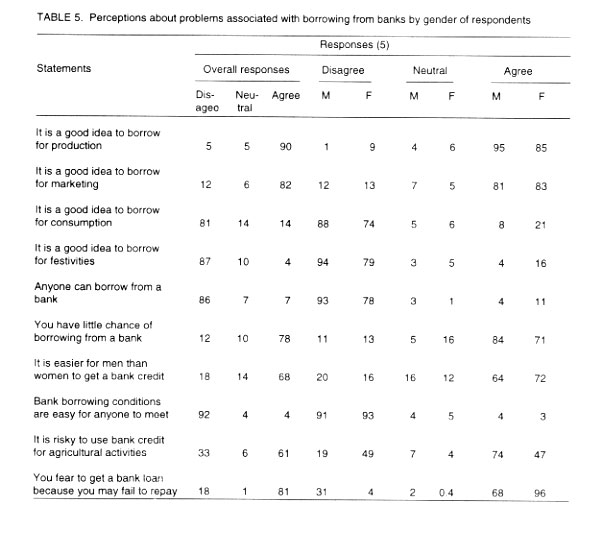

summarised in Table 5. When asked whether

they thought anyone could obtain a bank loan, 86 percent of the respondents

disagreed with this statement, with a larger 6 percentage of men (93 percent)

than women (78 percent) disagreeing with this statement.

Likewise, nearly 80 percent of the respondents stated that people like them

had little chance of borrowing from a bank. Again, a higher proportion of

men (84 percent) than women (71 percent) agreed that they had limited opportunity

of borrowing from a bank. An overwhelming majority of the respondents (92

percent) disagreed with the statement that it is easy for anyone to satisfy

bank lending conditions. While a large percentage of the total sample (81

percent) indicated that they were afraid to get a bank loan because they may

fail to repay the loan, a much higher proportion of women (96 percent) than

men (68 percent) perceived this problem. This substantial difference between

male and female respondents' attitudes toward bank credit seems to indicate

that women are more sensitive about getting into debt than men. It may also

show that women are more risk averse than men.

With respect to differential gender access to bank loans, 68 percent of

all the respondents agreed that it is easier for men to obtain a bank loan,

but a larger number of women (72 percent) than men (64 percent) perceived

this to be the case (see Table 5). Furthermore,

respondents were asked to express their perceptions about using bank credit

for certain purposes. As shown in Table 5,

a great majority of the respondents (90 percent) said it was 'a good

idea' to borrow bank money for production. Whereas about two-thirds

of all the respondents (61 percent) were of the opinion that it is risky to

use bank credit to finance agricultural activities, the proportion of men

who shared this viewpoint (74 percent) is close to twice that of the women

(47 percent) with the same perception. On the other hand, a more or less equal

proportion of all the respondents (82 percent), men (81 percent) as well as

women (83 percent) indicated that it is a good idea to utilise bank credit

for marketing or trading. However, the majority of men (88 percent) and women

(74 percent) dismissed the idea of borrowing for consumption purposes. Similarly,

both men (94 percent) and women (79 percent) did not consider it is wise to

borrow money for festivities (Table 5).

These responses indicate that both men and women have clear perceptions about

the general problems associated with bank borrowing and credit.

Characteristics of informal financial intermediaries (IFIs). About

70 percent of the respondents owned some animals. Numerically, poultry is

the leading type of livestock kept by the respondents (55 %) , followed by

sheep and goats (45%) and cattle (22%). Traditionally, cattle are kept as

physical assets or wealth, and are also used as a hedge against risk and inflation.

However, local cattle or other types of livestock can not be pledged as security

for commercial loans, because banks do not readily accept them as conventional

collateral.

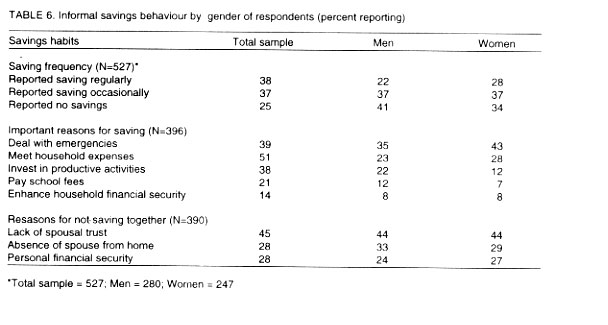

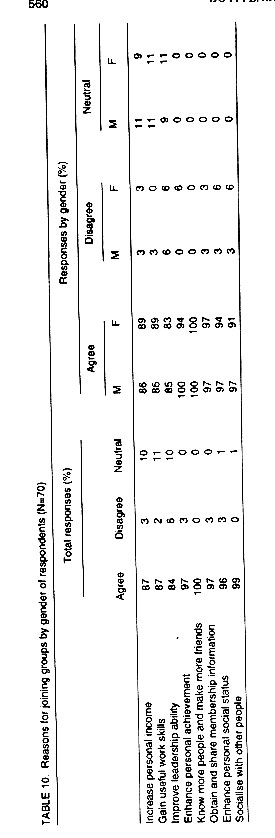

In order to characterise respondents' saving behaviour, they were asked

to answer questions about their saving habits, purposes of saving, and reasons

for not saving jointly with their spouses. The responses were disaggregated

by gender so as to ascertain differences, if any, in saving behaviour between

men and women. The results are shown in Table

6. About 75 percent of the sample responded that they did engage in saving

activities. The remaining 25 percent of the respondents did not save at all.

More women (66 percent) than men (59 percent) reported some savings, while

fewer women (34 percent) than men (41 percent) reported no savings at all.

When asked why they saved, the 396 interviewees who responded listed meeting

household expenses (51 percent), dealing with emergencies (39 percent), and

investing in productive activities (38 percent). Two other important reasons

for frequent saving mentioned by respondents were saving to pay school fees

(21 percent) and enhancing household financial security (14 percent). Both

men and women listed the same three top reasons for saving (Table

6). In comparison, however, women tended to be more concerned with saving

for emergencies (43 percent) and household expenses (28 percent), while more

men (22 percent) than women (12 percent) were interested in saving for investment

purposes. On the other hand, an equal proportion of men and women (8 percent)

were concerned with saving for household financial security.

As to whether or not respondents kept their savings together with their

spouses, over a quarter (26 percent) responded in the affirmative, while nearly

three-quarters (74 percent) said they had separate savings accounts. When

probed to explain why they did not save jointly, a large proportion of both

men and women (44 percent) gave lack of trust between the spouses as the primary

reason. Other important explanations for keeping separate accounts were the

prolonged absence of spouses from home, mentioned by 33 percent of the male

and 29 percent female respondents, and guaranteeing personal financial security

mentioned by 24 percent of men and 27 percent of women.

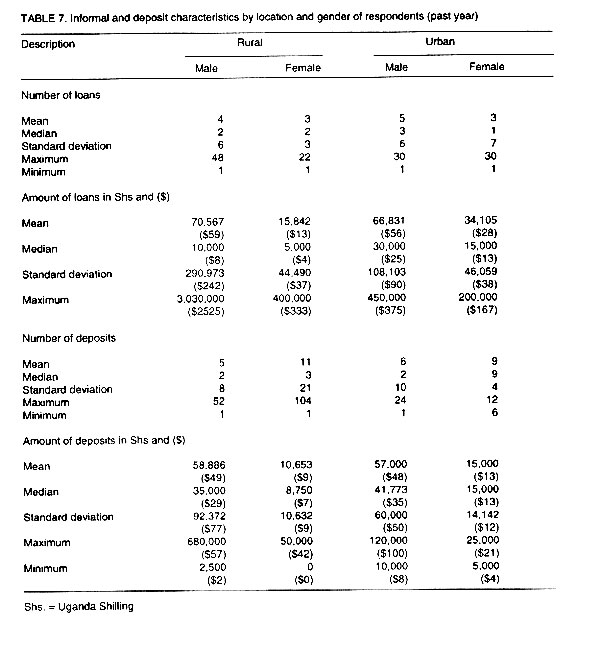

The survey information further revealed that 55 percent of all the respondents

had borrowed from informal sources in the past year. A slightly higher proportion

of men (57 percent) than women (52 percent) reported borrowing from informal

lenders. Relatives, neighbours and friends accounted for 93 percent of the

total number of informal loans. Relatives alone were responsible for 46 percent

of all loans; friends and neighbours supplied another 47 percent, while merchants

provided only 7 percent of the total number of loans. Generally, men averaged

a higher number of loans than women both in rural and urban areas. Also, the

mean total amount (value) of loans was greater for men (Shs. 68,699 or $57)

than for women (Shs. 24,973 or $21). Furthermore, the average value of loans

for rural men was about five times (Shs. 70,000 or $58) that for rural women

(Shs. 15,000 or $13), while in urban areas men's mean amount of loans (Shs.

67,000 or $56) was twice that of women (Shs. 34,000 or $28) (Table

7). The maximum amount of loans taken by men in rural areas is seven and

a half times (Shs. 3,000, 000 or $2,500) that granted to rural women (Shs.

400,000 or $334), while the maximum amount borrowed by urban men is two and

half times (Shs. 450,000 or $375) the value obtained by their female counterparts

(Shs. 200,000 or $167). Similarly, urban men had on average 5 loans, while

urban women had an average mean of 3 loans.

The mean number of informal deposit transactions made by respondents in

the past year was about 8. On average, female respondents made about 10 deposits,

compared to 5 deposits by men. Also, women in both rural and urban areas,

on average, had more deposits than men (Table

7). Conversely, men, on average, held greater amounts of deposits than

women whether in rural or urban areas. The maximum values of men's deposits

in rural areas (Shs. 680,000 or $567) and urban centres (Shs. 120,000 or $100)

were even much greater (14 and 5 times higher) than the maximum amounts held

by women.

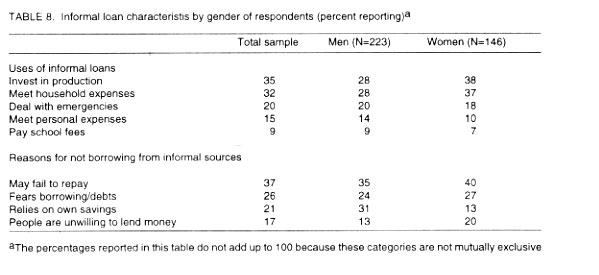

Informal borrowers used their loans to finance both production and consumption

activities. Most respondents (65 percent) used loan funds to purchase consumer

goods and services. However, the highest proportion of respondents (34 percent)

borrowed funds in order to finance productive activities, 32 percent used

their loans to offset household expenses, and 20 percent obtained credit to

deal with emergencies (Table 8). Other

frequently cited uses of consumer loans were meeting personal needs (15 percent)

and paying for school fees (9 percent). More women (38 percent) than men (28

percent) used their loans for production purposes. In contrast, a greater

proportion of men (71 percent) than women (61 percent) bought consumer goods

with their borrowed money. However, men and women were more or less evenly

distributed on the use of borrowed money to meet household expenses (28 percent

and 27 percent) and pay for emergency needs (20 percent and 18 percent) (Table

8).

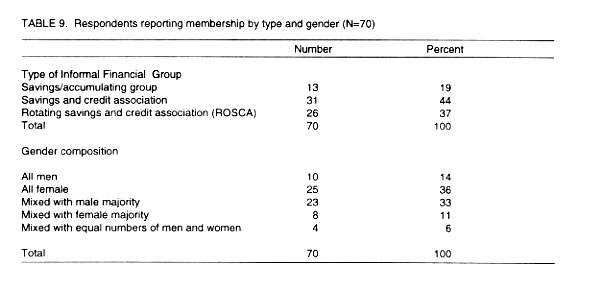

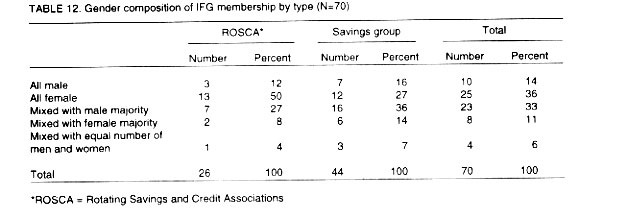

Characteristics of informal financial groups (IFGs). A sub-sample of

70 members were interviewed in order to explore the general IFG membership

characteristics and the results obtained are reported in Tables 9,

10, 11

and 12. Informal financial group members

belong to two main types of group savings that tend to occur commonly in the

country: savings groups and rotating savings and credit associations (ROSCAs).

Savings groups predominate, as they constitute about 63 percent of the total

membership of IFGs. These groups are comprised of accumulating or savings

associations (19 percent) and saving and credit association (44 percent) (see

Table 9).

Membership composition of a given group is based on a set of varied personal

and social characteristics of individual members (Slover, 1991). The composition

of IFG membership tends to be homogeneous with respect to such characteristics

as gender, age, education, occupation, income, community, ethnicity, geographical

location, and religion but is heterogeneous in terms of socio-economic status

(Cuevas and Graham, 1988; Slover, 1991). This means that various IFGs are

composed of people who are socially connected by various common bonds such

as sex, education, occupation or income, region, ethnicity, and religion.

In his study, Slover (1991) cited occupation, community, and ethnicity as

the main characteristics that bonded group members together, while gender

and religion did not contribute much to the common bonds.

There is a fairly wide variation in the membership size of IFGs reported

by respondents (see Table 11). Of the

70 members interviewed, over a third (37 percent) of them were in IFGs with

10 or fewer members, while 23 percent belonged to groups having 11-20 members,

and another 40 percent were in IFGs with more than 20 members. Thus, over

two-thirds (63 percent) of the IFGs had over 11 members. Rotating savings

and credit associations were generally smaller than savings groups with an

average membership size of 6, and ranging from as few as 2 to 11 members (Table

12).

According to the World Bank (1993), ROSCAs in Uganda have much larger memberships

than elsewhere, ranging from 25 to 50 people. The results obtained in this

study, however, show that about 40 percent and 73 percent of the entire ROSCA

membership consisted of 5 or less and 10 or fewer members, respectively. Savings

groups in Uganda, on the other hand, have larger memberships, ranging between

2 and 26, with an average mean of 11 members. Compared with ROSCAs, about

84 percent of all savings groups have greater than 10 members with nearly

60 percent of them exceeding 20 members. These results are strikingly similar

to the findings of previous studies done in sub-Saharan Africa (e.g., see

Bouman, 1977; Slover, 1991).

Similarly, IFG membership sizes reported in the literature in different

parts of the world range from as few as 5 members to as many as 152 people

(Bouman, 1977; Seibel, 1986). For sub-Saharan Africa the membership size of

IFGs has been estimated to vary between 10 and 152 patrons (Bouman, 1977;

Seibel, 1986).

Group composition is either based on separate or single social bonds, or

transcends several types of bonds. For example, the membership of a group

may be made up of single or mixed sex participants (see Tables

11 and 12), or people from the same

occupation or same locality. It is not uncommon for a person who belongs to

one type of group having one set of goals to be simultaneously a member of

another kind of group with quite a different set of objectives. There are

a number of differences between men's and women's groups with respect to the

place of social bonds (affective/emotive ties or social solidarity) in group

formation and patrons' socio-economic activities.

Purely male groups are fewer in number and tend to be smaller than all female

groups ( Table 12). They also have multi-village

memberships, concentrate their efforts on mainly economic projects, and reinvest

their savings into income-generating activities. In contrast, all female groups

are larger in size, are more numerous (25 or 36 percent), and consist primarily

of village residents, but engage in both economic and extra-economic community-oriented

activities such as health, social welfare, and handicraft works that do not

have readily available markets.

However, mixed-sex groups dominated by males have larger membership sizes

than purely men's groups. Likewise, they are more numerous, as they constitute

33 percent of the total membership relative to female dominated mixed groups

which make up only 11 percent of all IFGs (Tables

11 and 12). There are also a few

groups (6 percent) with equal sex composition in their membership ranks. It

is not clear from the survey why some groups are all male or all female. Some

researchers (e.g. Slover, 1991) have suggested that single-sex groups enable

their members to maximise membership information, as homogeneous groups have

a greater information advantage or possess more perfect knowledge over heterogeneous

groups. He has also suggested that members of single-sex groups may enjoy

a higher degree of trust than mixed groups.

Whereas gender plays a key role as a factor of primary group affiliation,

both among men and women, male groups tend to be more discriminatory with

respect to membership recruitment. According to Tripp (1994), primary affiliation

through formation of effective ties is not the driving force behind the initiation

and endurance of women's groups in Uganda. This is because female members'

primary motive for coming together is economic survival and improvement of

social welfare through mutual support activities. In contrast, she claims

that men's groups are often based on sectarian considerations such as

ethnicity, clanism, region, partisanism, class, and even religion. This is

typical of men's cultural and burial groups (e.g., "Munomukabi" groups

in Buganda) whose members are brought together by descriptive affiliations

based on primary affinity such as kinship. Even men's groups that are

formed primarily for economic purposes still tend to base their membership

recruitment on certain kinds of discrimination.

According to Tripp (1994), purely women's groups, especially in urban

areas, are more encompassing as the composition of their memberships usually

cuts across occupational, ethnic, political and religious boundaries. In practice,

women generally reject male-dominated sectarian associations. Tripp(1994)

reported that the membership of a typical non-sectarian female association

consists of women from different ethnic groups, political persuasions, religious

convictions, educational levels, and occupational status. She found only a

few women's groups in Kampala city that were based on purely ethnic

ties. She goes on to point out that even in rural areas female savings clubs

include members from various groups. Our survey results confirm these observations.

Female IFGs tend to be further bonded together by occupation and residence.

Women find it much easier to come together and get along with one another

because they are often restricted from joining male groups that are formed

around some primary affinity such as savings clubs or affiliates of larger

already existing bodies like church groups, viz. Mothers' Union, which

may be composed of women from several different ethnic groups, various religious

affiliations, as well as diverse types of occupations and remuneration levels.

Such groups are formed by women of diverse backgrounds and transcend affective

relationships, including work mates, business associates, neighbours, friends,

and others, thereby providing a new lease of life for the community.

Discussion and policy implications

Findings of this study indicate that there is a limited access to and low

level of use of rural finance by both female and male respondents. The majority

of the men and women who use informal financial arrangements have virtually

no access to formal financial institutions, but there are a few people (mainly

men) living largely in urban areas who use both types of finance. The overall

proportion of male respondents with bank accounts is very small (13 percent),

while those men who hold deposits with semi-formal institutions form miniature

proportions.

The number of male respondents who have requested and obtained bank loans

constitute even smaller proportions (5 and 2 percent) of the total sample.

Virtually, no female respondents applied for and obtained any bank loan, or

had any deposits or savings with either formal or semi-formal institutions.

Clearly, the formal financial sector does not cater for the credit and savings

needs of poor people, particularly of women. The pronounced absence of formal

financial institutions in the rural economy has consequently reinforced the

critical importance of the informal financial sector for the well-being of

rural households, especially female-headed families.

The results further reveal that most rural people tend to hold their savings

in the form of non-monetary assets such as various types of livestock, stocks

of harvested or standing crops, and stored inputs. Although some people hold

their savings in monetary assets, these savings are small. Recent studies

done in Tanzania (Temu and Hill, 1994) and Gambia (Zeller et al., 1994)

also report that both means of savings are widely practised by rural people.

The tendency of rural people to hold most of their assets in physical rather

than liquid form has resulted, among other things, from lack of commercial

deposit or savings facilities and incentives, as seen above. Likewise, this

is associated with the loss of popular confidence in the banking system due

to currency reform (devaluation), inflation, and negative real interest rates

coupled with mismanagement and corruption perpetuated by bank officers.

It is also evident from the results that both men and women are willing to

save and do save even from their low incomes. Most respondents (75 percent)

reported either saving regularly or whenever their income and expenditure

budgets permitted them to do so, although the savings tend to be small. A

higher proportion of women (66 percent) than men (59 percent) reported some

savings. Also, female respondents both in rural and urban areas made many

more deposits than male respondents, but the average value of men's

savings was higher than women's. These differences imply that women

are more conscientious and concerned about the welfare of their families than

men, as suggested in the Women in Development literature (see Blumberg and

Clark, 1989). However, these results are contrary to the Women in Development

literature which asserts that women tend to spend a larger proportion of their

income on household welfare than men.

In addition to monetary savings and loans, rural people may even draw on

their physical assets in order to enhance their households' consumption

during hard times. According to Zeller et al. (1994), during such periods

rural households in general use both their physical and liquid assets as a

mechanism of self-insurance to hedge against future food and other forms of

insecurity. Similarly, Townsend (1994) has found exchange of gifts among villages

in Southern India to play an important role in smoothing income fluctuations.

These researchers argue that apart from personal or household savings and

informal borrowing, rural people need commercial credit to boost their consumption

smoothing strategies and hence increase their capacity to bear risks. That

is, households use informal credit to smooth their annual income fluctuations

and seasonal shortages of food stuffs as well as to finance productive activities.

The foregoing results suggest that women may be saving and investing more

than men because they are more concerned about their households' long-term

food and financial security than men. When the non-borrowers (45 percent)

were asked to explain why they did not borrow, they provided a number of reasons.

The most common explanation was the inability to repay loans (37 percent of

the non-borrowers). This was also the reason most frequently given by both

men (35 percent) and women (40 percent). The fear of debt was the second main

reason for not borrowing and was mentioned by 26 percent of the respondents.

But there were proportionately more women (27 percent) than men (24 percent)

who gave this explanation.

Since early 1970s men's incomes in the formal sector have declined,

as a result of political instability coupled with economic repression in Uganda.

This has exerted mounting pressures on Ugandan women to use alternate (non-traditional)

sources of household sustenance, mainly in the informal sector, where they

had been pushed by male and state discrimination. As such, women, more especially

in urban areas, are using rising proportions of their incomes to meet household

expenses for food, clothing, health, and educational expenses (Tripp, 1994)

which used to be provided by men and the state.

The results furthermore indicate that poor people save for rational socio-economic

reasons. As in the case of informal credit, most of the respondents reported

using their cash savings for purposes of smoothing consumption such as during

family emergencies (death, funeral rites), paying school fees and meeting

household expenses, but a substantial proportion of savings are also used

for investement activities like production and trade. Men and women also differed

with respect to their primary motives for saving. Proportionately, more men

(22 percent) than women(12 percent) saved for investment purposes, while more

women saved for meeting family emergencies (43 percent) and household expenses

(28 percent).

Important policy implications emerge from the results of this study. First,

there is an urgent need to establish effective facilities for rural people

to deposit their savings as well as opportunities for them to invest these

savings into productive activities. In this regard, development finance planners

and policy makers need to recognise a growing body of empirical evidence which

indicates that poor people in general and women in particular are able and

willing to save when they are availed the necessary opportunities (Lipton,

1988; Morris and Meyer, 1993). This calls for incentive economic programmes

to mobilise saving, lending, and investment capacity in the rural economy.

A minimal solution to this problem is to provide effective and efficient facilities

as well as a safe socio-economic environment for savers, borrowers, and investors

in the rural areas.

Second, available research evidence clearly indicates that rural people require

credit to simultaneously meet both their households' production and

consumption requirements. This means that the theoretical distinction between

production and consumption activities is not practical. Because of its fungibility,

credit used for consumption purposes also does contribute to productive activity

(Adams, 1978; Adams and Vogel, 1986; Adams and Fitchett, 1992; Zeller et

al., 1994). In practice this means that for credit programmes to work

more effectively and efficiently, loans should be advanced to both small-scale

male and female borrowers both for production and consumption purposes, including

smoothing household income fluctuations and seasonal food shortages.

Third, administrators also need to take cognizance of research evidence showing

that women tend to have greater ability and propensity to save than men (Cuevas

et al., 1990; Morris and Meyer, 1993). It has been demonstrated by

previous research (see Morris and Meyer, 1993) that generally women have better

repayment records than men. This evidence calls for women's special

credit and savings needs to be seriously taken into account by formal financial

institutions. Likewise, policy makers and planners should pay more attention

to women' needs for financial services by translating rhetoric into

action in gender-aggregated rural development programmes.

Finally, policy makers should consider using informal financial intermediaries

as conduits for delivering badly needed financial services to rural people.

In particular IFGs should provide a viable vehicle for this purpose. The experiences

of the Grameen Bank in Bangladesh and other successful experiments in other

East Asian countries demonstrate the feasibility and viability of the group

based approach to the provision of financial services to poor people. The

current Government policy of extending soft loans to rural communities through

the "Entandikwa scheme", if properly managed, is a step in the right direction

(Ministry of Finance and Economic Planning, 1995).

REFERENCES

-

Adams, D. W. 1978. Mobilizing household savings through

rural financial markets. Economic Development and Cultural Change

26:547-560.

-

Adams, D.W. and Fitchett, D.A. 1992. Informal Finance

in Low-Income Countries. Boulder, Colorado, Westview Press.

-

Adams, D. W. and Vogel, R.C. 1986. Rural financial markets

in low income countries: Recent controversies and lessons. World Development

14:477-487.

-

Blumberg, R.J. and Clark, M.H. 1989. Making the case

for the gender Variable: Women, the Wealth and Well-being of Nations.

Washington, D.C., USAID.

-

Bouman, F.J.A. 1977. Indigenous savings and credit societies

in the Third World: A Message? Savings and Development 1:181-220.

-

Carr, S.J. 2001. Changes in African smallholder agriculture

in the twentieth century and the challenges of the twenty-first. African

Crop Science Journal 9:331-338.

-

Crook, R. and Manor, J. 1994. Enhancing participation and

institutional performance: democratic decentralization in South Asia and

West Africa. A Report to ESCOR, the Overseas Development Administration

on Phase Two of a Two Phase Research Project.

-

Cuevas, Carlos, E. and Graham, D. H. 1988. Development

Finance in Rural Niger: Structural Deficiencies and Institutional Performance.

Economics and Sociology Occassional Paper Number 1471. Department of Agricultural

Economics and Rural Sociology, The Ohio State University, Columbus, Ohio.

-

Hubner, U. and Fischer, M. 1992. Supporting Self-Help Groups

in Uganda. Revolving Loan for Non-Governmental Organisations. Kampala.

-

Jiggins, J. 1989. How poor women earn income in sub-Saharan

Africa and what works against them. World Development 17:953-963.

-

Lipton, M. 1988. The Poor and the Poorest: Some Interim

Findings. World Bank Discussion Paper No. 25. Washington D.C.

-

Ministry of Finance and Economic Planning (MFEP) 1995. Entandikwa

Credit Scheme Operational Guidelines. Uganda Government Printery, Kampala.

-

Morris, G.A. and Meyer, R.L. 1993. Women and Financial

Services in Developing Countries: A Review of the Literature. Economics

and Sociology Occasional Paper No. 2056, Columbus, Ohio, The Ohio State

University.

-

Seibel, Hans Dieter. 1986. Rural finance in Africa: The

role of informal and formal financial institutions. Development and Cooperation

6:2-14.

-

Slover, Curtis. 1991. Informal Financial Groups in Rural

Zaire: A Club Theory Approach.

-

Temu, A.E. and Hill, G.P. 1994. Some lessons from informal

finance practices in rural Tanzania. African Review of Money Finance

and Banking 1:141-165.

-

Townsend, R. 1994. Risk and insurance in village India.

Econometrica 62:539-591.

-

Tripp, Aili Mari. 1994. Gender, political participation

and the transformation of associational life in Uganda and Tanzania. African

Studies Review 37:107-31.

-

Uganda Ministry of Health. 1989. Demographic and Health

Survey 1988-89. Entebbe, Uganda, 1989.

-

UNICEF. 1989. Children and Woman in Uganda: A Situation

Analysis. UNICEF, Kampala, Uganda.

-

World Bank. 1993. Uganda Agriculture. A World Bank Country

Study. Washington D.C., The World Bank.

-

Yaron, J. 1990. Rural Finance in Uganda. World Bank/Bank

of Uganda, Kampala, Uganda.

-

Yaron, J. 1991. Uganda: Financial Sector Review: Green Cover

Report. Unpublished Memorandum, World Bank.

-

Zeller, M.J., Von Broun, K. J. and Puetz, D. 1994. Sources

and terms of credit for the rural poor in the Gambia. African

-

Review of Money. Finance and Banking 1:167-185

© Copyright 2001, African Crop Science Society

The following images related to this document are available:

Photo images

[cs01074f6.jpg]

[cs01074t7.jpg]

[cs01074t5.jpg]

[cs01074t3.jpg]

[cs01074t4.jpg]

[cs01074t11.jpg]

[cs01074t10.jpg]

[cs01074f7.jpg]

[cs01074t8.jpg]

[cs01074t9.jpg]

[cs01074t12.jpg]

[cs01074t1.jpg]

[cs01074t6.jpg]

[cs01074t2.jpg]

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}