|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

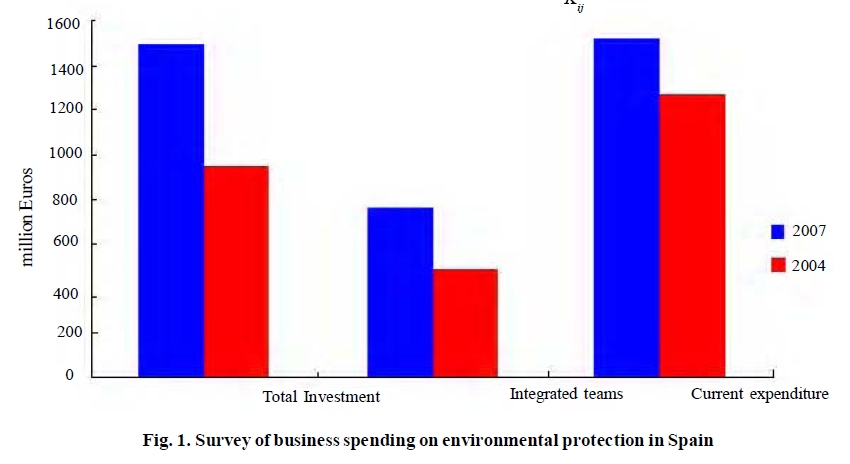

International Journal of Environmental Research, Vol. 4, No. 3, July-September, 2010, pp. 373-378 Article Environmental protection expenditure for companies: A Spanish regional analysis Vargas-Vargas, M. 1 , Meseguer-Santamaría, M. L. 1 , Mondéjar - Jiménez, J. 2* and Mondéjar - Jiménez, J. A. 2 1 Faculty of Economics, University of Castilla-La Mancha, Spain Date of Submission: 25-Dec-2009 Code Number: er10041 Abstract Environmental protection has become one of the main concerns in developed economies, which is why an increasing degree of commitment in the field is required from all public and private bodies. Environmental protection in firms must cease to be a secondary, barely profitable objective, involving the performance of sporadic remedial actions, and become just one more element of their organization which, though it may require investment, may also provide a firm with major opportunities and cost reductions. This paper looks at the latest trends in expenditure on environmental protection by industrial firms. The information available is from the Spanish National Statistical Institute (INE), provided for the Spanish regions. Then, using shiftshare analysis, we will seek to ascertain whether there are competitive advantages and each region's degree of specialization in the main lines of expenditure.Keywords: Environmental protection, Spanish, Shift-share and industries Introduction Firms currently face a clear and growing demand from society for the environment to be protected. In this context, firms must be receptive to such demands and obligations. Any one that is not, and that has vis-ibly negative environmental impacts, will be seriously compromising its future. The environment affects every company regardless of its size, and today it is a fact that the environment is a key requirement in achiev-ing long-term corporate success (Burnett & Hansen, 2008). For companies, in terms of reputation and achieving a competitive advantage, this involves assuming and internalizing a portion of social costs on their balance sheets (Porter & Kramer, 2002). But it needs to be recognized that the incorporation of environmental cri-teria must be from a strategic and integrating perspec-tive (Fuentes, 2006). This factor is also considered by consumers, with a positive perception of a "socially responsible" company, making them more likely to consume its products in equal cost conditions (Bigne et al., 2005). Combating pollution, both inside and outside in-dustrial plants and complexes, requires systematic en-vironmental management in companies. In Spain this task requires a major assignment of technical and eco-nomic resources, in order to achieve the desirable level within the European Union. Appropriate environmen-tal management in an industrial firm involves foresee-ing contingencies associated with corporate finances as regards cleanup techniques, staff organization and company psychology (Hidalgo, 1998). In this respect, companies have undergone a ma-jor environmental transformation, taking the form of a set of practices designed to prevent and correct the environmental impact of their activities (Gonzalez & Gonzalez, 2007). Thus we have gone from a reactive attitude to environmental transformation, confined to a minimal implementation of environmental practices forced upon firms by legislative requirements or the need to yield to the requirements of various pressure groups (such as public administration, environmental organizations or the media), to a proactive approach, as has been highlighted by numerous studies (Gonzalez & Gonzalez, 2007; Hunt & Auster, 1990; Winsemius & Guntram, 1992; Aragon, 1998; Buysse & Verbeke, 2003). On one hand, environmental practices may entail savings in manufacturing or distribution costs arising from the rational use of resources, the reduction of defects or the reuse of materials (Porter & Van der Linde, 1995). On the other, environmental practices constitute an attribute of firms' offerings that is in-creasingly appreciated by consumers, and so may help create a differentiated image that is attractive to the market (Reinhardt, 1998). Despite the previous spatial transformations, Spain began the early 80s with one of the best-preserved natural heritages in the Mediterra-nean and European areas. From a socioeconomic per-spective, the 80s began with a political transition and Spain's economy embarked on a period of growth, with-out any strong pressure on its ecosystems and with a productive system that in many cases remained exten-sive (Lomas et al., 2008). In order to establish environmental objectives and goals, below we list the main impacts of industry:

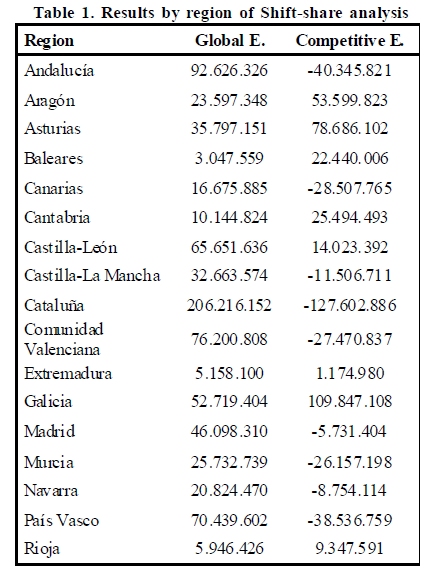

In this connection we may ask how Spanish firms are going to tackle this decade and the future. Spain's accession to the European Union, with the acceptance of all of its environmental regulations, and the strong pressure from society in the field, requires a huge ef-fort to implement measures enabling firms to cater for increasing environmental requirements. The situation of Spanish industry with regard to the environment shows a certain lag relative to that in the other Mem-ber States. Solutions must necessarily be based on shared responsibilities assumed by legislators, regional authorities, industrialists, traders and, finally, end con-sumers. We should keep in mind that the relationship be-tween environmental protection, economics and em-ployment has been interestingly addressed by the lit-erature. Analysts and politicians seem to agree from all perspectives that there is a strong relationship be-tween environmental protection and employment.Many studies have been conducted in the past two decades with the aim of estimating the economic and employ-ment effects of environmental protection. These stud-ies may be grouped into three types: (i) theoretical analyses and case studies, (ii) econometric simulations of political alternatives, and (iii) empirical studies, with estimations based on historical data (Bezdek, Wendling & DiPerna, 2008). Expenditure in the various regions in environmental matters has been studied from vari-ous viewpoints, but no useful studies have been made of expenditure in firms (Aguado & Echevarria, 2003). Finally, the concept of sustainable development has emerged to correlate the need to keep raising stan-dards of living and that for environmental protection. In the industrial sphere, things have moved more quickly. Thus, for example, many companies use waste as fuel, and have been the first to recognize its envi-ronmental significance. There should be a direct rela-tionship between expenditure and the environment; the trend to assign increasing amounts to environ-mental protection should make the environment cleaner and less polluted (Duran et al., 2009). Environmental protection from the business per-spective has traditionally been associated with expen-diture, costs or losses for the firm. Some studies con-sider two components of environmental expenditure: one arising from regulation, and a voluntary compo-nent (Johnston, 2005). The former, referred to as regu-latory expenditures, constitute a significant part of environmental expenditure and include the consider-able costs related to compliance with environmental legislation (Hamner & Stinson, 1995). Voluntary environmental expenses are those in-curred by a company as part of an effort to improve its corporate image or to enhance its environmental per-formance (examples of this are expenses incurred in making environmental studies, audits or voluntary emission reductions, implementing recycling programs, preparing annual environmental reports, or taking part in voluntary programs). Environmental management accounting represents a combined approach involv-ing a transition of data from financial accounts, cost accounts and balance sheets so as to improve materi-als efficiency reduce environmental impacts and risks, and lower environmental protection costs. Such stud-ies are conducted by private or public companies and have a financial component and also a physical one (Jasch, 2003). Management accounting constitutes a vital tool for internal management decisions, such as setting product prices, and is not regulated by law. Such an internal information system seeks to answer two questions: what are the production costs of the firms' various products, and what should those prod-ucts' sale price be? The main figures concerned in cost accounting are various managerial post holders (e.g. executives, product and production managers). The concern for environmental protection is steadily increasingly, as is the interest in environmen-tal accounting (Beets & Souther, 1999; Deegan, 2002; Gray, Kouhy & Lavers, 1995; Mathews, 1997). The business community's response has been to gather more information about environmental activities for the interested parties. Materials & Methods This study is intended to make a specific but po-tentially useful examination of the trends in projec-tions of future expenditure for reducing environmental impacts, like other similar studies in the literature (Cormier & Magnan, 1999, Cormier et al., 2005; Patten, 2005), but by focusing on the case of the Spanish re-gions, according to the EU-regulated subdivisions set out in the Nomenclature of Territorial Units for Statis-tics (NUTS-II). If we consider the three main expenditure items (from a total of 19) in the environmental protection expenditure survey (Spanish Statistical Institute, 2010), expressed in millions of Euros, representing 63% of total expenditure, we can see how the items have un-dergone growth from 20% in current expenditures up to more than 50% in equipment, highlighting the im-portance that companies accord to environmental pro-tection [Figure - 1]. The trend for the last three years according to the available data reveals that one region has undergone a truly notable increase in investment: the Balearic Is-lands have seen corporate expenditure on environmen-tal protection increase fourfold. Moreover five Spanish regions (Aragon, Asturias, Cantabria, Castilla y Leon y La Rioja) saw such invest-ment double in recent years. On the negative side, such investment in the Basque Country was similar to that in the last period analyzed, while the Canary Islands and the Region of Murcia saw an appreciable decrease in firms' expenditure on environmental protection. To further study industries' capacity for investment in the environmental field along with the spatial distribu-tion thereof, we opted to make a shift-share analysis, a technique used in regional statistical analysis and which allows the effects associated with the different structure of the Spanish regions to be quantified (Vargas et al., 2009). Shift-share analysis was developed by Dunn (1960) as a method for calculating the components that explain the variations in economic magnitudes. Accord-ing to Dunn (1960), "the essential component in this statistical technique is to calculate geographical changes in the evolution of the economy". If K ij . is used to denote the initial expected capital cor-responding to measure i (i=1,…,s) ) for the county j (j=1,…,r) ) in the initial instance and K' ij the capital committed in this measure and county in the final in-stance, then the variation recorded (degree of finan-cial implementation) may be expressed by the follow-ing equation (Mayor and Lopez, 2005): K’ij - Kij = Δ Kij= Kijγ + Kij( γi - γ) + Kij(γij - γi) where:

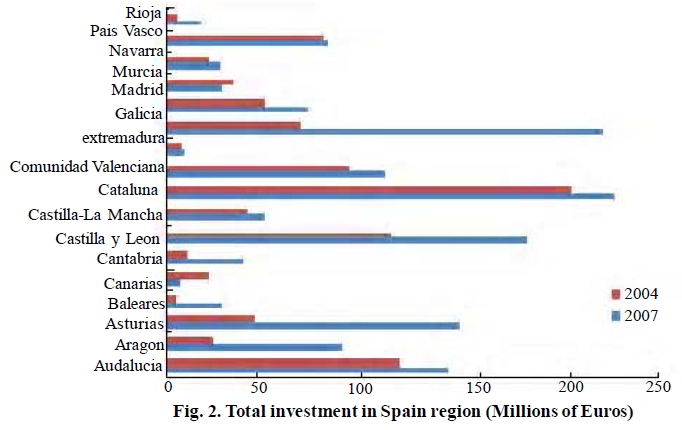

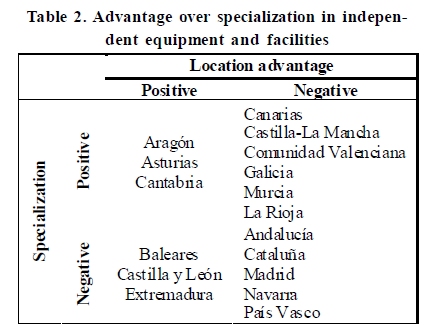

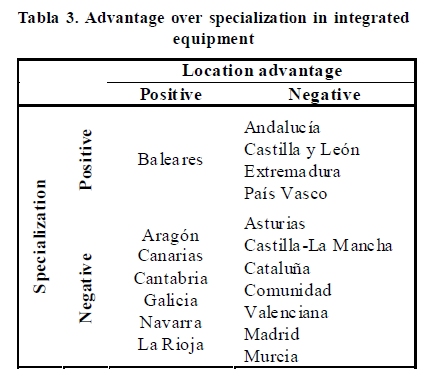

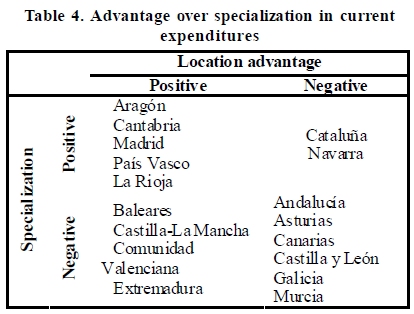

and the three addends into which the global variation of the magnitude under study may be broken down receive the names: Global Effect EG ij = K ij r Structural Effect EG ij = K ij (r i - r) Competitive Effect EG ij = K ij (r ij - r) Using this technique we will obtain the overall ef-fect and the competitive effect, normally called net ef-fect, showing a region's particular dynamism relative to the national level in each expenditure item, and there-fore forming a measure of the region's "success" in investment in environmental protection. Results & Discussion Environmental practices are a source of competi-tive advantages, and taking a proactive position in the field involves going beyond the functional areas com-prising a company and integrating environmental cri-teria into the definition of corporate competitive strat-egy (Barnejee, 2001) and generating diverse motiva-tions (Bansal & Roth, 2000). The classic dichotomy between cost strategy and differentiation strategy serves to identify two generic sources of competitive advantage potentially associated with environmental pro-activity. Orsato (2006) classifies environmental strategies in two dimensions: on one hand, an emphasis on lower costs over differentiation. On the other, an emphasis on organizational processes over a stress on product and service design. By calculating the effects of the classic shift-share model and aggregating them by re-gion, we will obtain an estimate of overall and competi-tive effects, set out in [Table - 1].A proper interpretation of the data requires a detailed analysis of overall and competitive effects: thus the competitive effect has a negative value in nine of the seventeen Spanish re-gions. For its part, the structural effect -smaller than the competitive one in many regions-has a more het-erogeneous result by region, not allowing behavior patterns to be inferred, though it is positive in all cases. The data show an especially notable overall effect -in excess of two hundred million Euros- in the region of Catalonia, highlighting the importance of this measure of investment in environmental protection [Figure - 2]. Finally, if we group the regions according to whether they show competitive advantages or not, and also to whether they are specialized or not, we obtain a double-entry table (Alavi & Yasin, 2000), for each mea-sure of environmental protection [Table - 2],[Table - 3],[Table - 4]. in which we see the position of each region in the various measures (independent equipment and facilities over integrated protection equipment), classified by spe-cialization and the existence of location advantages. Conclusion The challenge for firms in the environmental field is to anticipate changes and identify the opportunities that they involve, and to act in line with this approach. To this end, they may act with their own resources or apply for State grants for environmental investment projects or fiscal subsidies, etc., and use other eco-nomic instruments that may arise from environmental needs themselves. In this context, firms should be re-ceptive to these demands and obligations. Those which are not, and which harm the environment, are seriously compromising their future. With the results obtained, we may observe a grow-ing awareness, highlighting industries' commitment to respect for the environment, which has ceased to be a secondary factor and become a primary one that is part of most corporate operating strategies. We also see that the bigger the company, the more consider-ation there is for the environment.In this connection the relative importance for the regions of investment in environmental protection becomes clear: in 14 of the 17 regions, the increase experienced is positive. With regard to the uneven distribution of investment, it is true that the starting levels were not taken into account and the data used were not weighted (for ex-ample, by population), though the information used does allows us to broadly map profiles by region. This is one of the future lines of research arising from our study.To complete this overview, the application of shift-share analysis allows us to break down environ-mental investment into various effects:

References

Copyright 2010 - International Journal of Environmental Research The following images related to this document are available:Photo images[er10041f2.jpg] [er10041t1.jpg] [er10041t2.jpg] [er10041f1.jpg] [er10041t4.jpg] [er10041t3.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}