|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

The African Journal of Food and Nutritional Security Vol. 1, No. 1, 2001, pages 46 - 59 The Cassava Processing Industry in Brazil: Traditional Techniques, Technological Developments, Innovations and New Markets

Gerard Chuzel UNESP-CERAT, CP 237, 18603-970, Botucatu, SP, Brazil Code Number: fn01006

ABSTRACT

The paper considers the evolution of cassava-based industrial production, processing and marketing in Brazil, in light of the great technological diversification to be found in Brazil. It discusses the private role of the small- and medium-scale food and related processing enterprises in the food industry, as they employ cassava in producing an array of products associated with the various domestic economic classes, as well as the export market. The paper discusses new products and markets and the development of the R&D establishment to support these new growth potentials.

Key Words: cassava, cassava derivatives, processing technologies, Centro da Raizes Tropicais (CERAT), Small and Medium-Scale Enterprises (SMEs), markets, agro- food industry, traditional farming, products, technological diversity Introduction The food industry, with a turnover of some US$45 million in 1993, has become one of the cornerstones of the Brazilian economy. The sector provides 10% of the overall gross domestic product (GDP), accounts for 17% of total export earnings, represents 23% of industrial establishments and employs 13% of the active population. The industrial fabric is predominantly made up of small and medium-scale enterprises (SMEs), the socio-economic impact of which is widely recognized and the development, for Brazil as for many other countries in the South, an issue of the first magnitude. These SMEs are little or poorly equipped to meet the technological challenges which they need to surmount, in order to develop in the face of:

Among the various sectors, that of cassava is highly representative of the great technological diversity to be found in Brazil, its deeply rooted traditions and potential. Brazil has always been a major producer of cassava, with a wide variety of farming systems, ranging from backyard cultivation, traditional farming by small-scale farmers in the semi-arid areas of the Nordeste (northeastern) or Amazon regions, to large-scale cultivation in southern Brazil. There, planting and harvesting are semi-mechanized and cassava is grown alongside soya beans, maize and beans. Whatever the agro-ecological zone type, cassava is a safe crop, which guarantees farmers a source of income, regardless of climatic ups and downs. The same diversity which is found in farming methods is also present in processing and marketing systems. The technological spectrum is extremely broad, from casas de farinha (flour houses) in the north, producing several hundred kilos of flour a day, to the starch mills of Paraná, which are able to process 500 tonnes of roots a day. The products derived from cassava vary widely from region to region, but farinha ( a sort of cassava flour used to accompany many traditional dishes), continues to be dominant. the cassava processing industrial sector is now seeking access to new markets, either through creating new uses for cassava derivatives or through developing new products. Nevertheless, until now, the sector has only received very little institutional support in terms of research and development (R&D) or technological assistance. The creation, under the auspices of the University of the State of Sao Paulo, Universidade Estadual Paulista (UNESP) of a tropical roots centre, Centro de Raizes Tropicais, (CERAT) brings together researchers, developers, local authorities and class associations, in attempt to provide the sector with a support instrument to assist its development. Following a brief overview of the Brazilian agro-food industry and the importance of SMEs and their attendant limiting factors, a presentation is made of the various cassava-processing technologies used in Brazil and the derivatives produced. Change in the industrial sector, its outlook and potential are then addressed, with due consideration given to markets and products, both traditional and new. Finally, CERAT's activities are presented, together with the strategies adopted in order to integrate these activities into an overall regional development policy. it is based on a high-performance cassava-processing industry, adapted to local socio-economic constraints.

Importance of SMEs in the Brazilian agro-food industry

The Brazilian agro-food industry is founded on a buoyant agricultural sector and presents an extremely varied panorama, ranging from large farms producing export crops (soya beans and oranges), to family-based agriculture, on which increasing attention is now being focused - due to its impact in terms of regional development.

The agro-food industry presents the following characteristics:

1. A structure largely based on SMEs

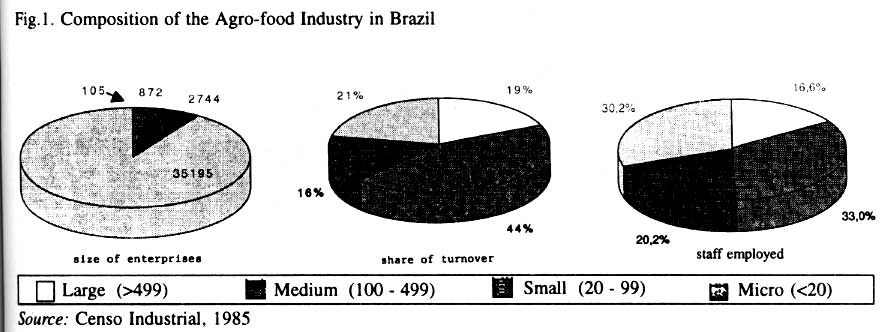

The industrial fabric is made up of a large number of micro, small and medium-scale

enterprises (Fig. 1). Out of approximately

43,000 establishments recorded, over 97% are micro-enterprises (with less than

19 employees) or small enterprises (with 20-99 employees), representing 37%

of the sector's turnover and employing 51% of its labour force. Medium-scale

enterprises (with 100-499 employees) are more strongly represented in terms

of the total turnover than large ones. It should also be noted that a considerable

number of agro-food activities remain within the informal sector, particularly

where meat and dairy products are concerned.

The bulk of the work force is employed by medium-scale enterprises, representing 44% of employees, compared with 21% for small units and 16% for large ones. Between 1980 and 199, job creation showed an annual growth rate of 1.2%, representing a cumulative increase for this period of 13.5%, compared with 6.6% for industry as a whole. However, over the following two years the work force has decreased by 3.5%, to reach a total of 745,000 persons. On the other hand, although average wages increased in real value by 7.8% in 1993, they remain extremely low when compared with some other countries. It is worth noting that the food sector has a higher staff rotation rate, averaging 4.4% as against 2.8% for all sectors taken together. The work force continues to be highly disadvantaged, far more so than in other industrial sectors, with over 75% of employees having left school before completing their primary education.

3. Sectorial segmentation

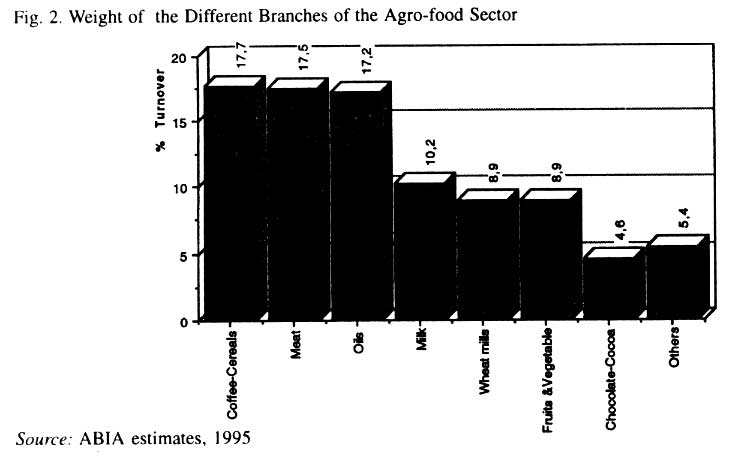

Micro and small-scale enterprises are found in the following main areas of activity: coffee (initial processing, roasting, grinding); cereals and derivatives; various flours, especially cassava; maize derivatives, except starch and oils; canning; the manufacture of sweets and candies; as well as the manufacture of pasta, biscuits and bakery products. It can also be observed that industry is heavily concentrated in certain spheres of activity dominated by the principal large-scale industries which account for most of the turnover. These are chiefly instant coffee, grinding or preparation of vegetable oils, powdered milk, canned meat, cornstarch, integrated factories producing sugar and fuel alcohol, as well as orange juice concentrates. Despite extensive and increasing diversification of food product processing activities, 95% of activity within the agro-food industry falls within eight major branches (see Fig. 2).

4. Unequal geographical distribution

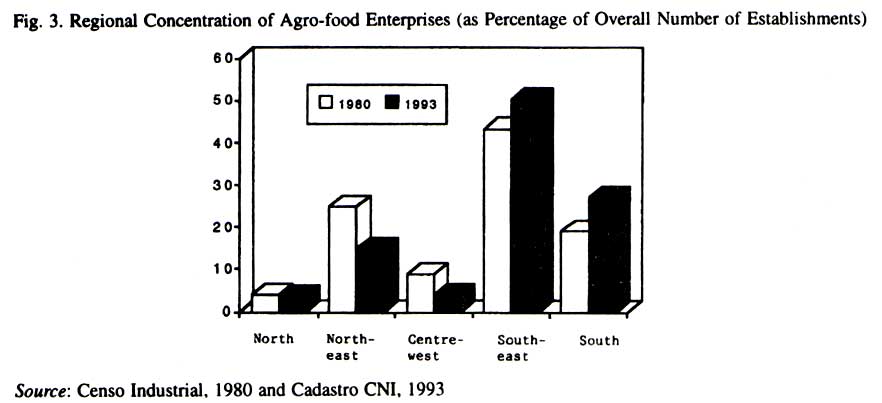

The food industries are unequally distributed within the country (Fig. 3), with over 60% of enterprises located in the states of Sao Paulo, Rio de Janeiro, Minas Gerais, Paraná and Rio Grand do Sul (southern and south-eastern regions, which generate 75% of Brazil's GDP), a tendency which was accentuated during the period 1980-1993. Nevertheless, compared with other industrial sectors, the agro-food sector is one of the most deconcentrated.

5. Still a largely national industry

The Brazilian food industry is characterized by strong involvement by national private enterprises (63%) rather than investment by foreign enterprises (37%). National public enterprises are absent from this sector.

6. An expanding domestic market

With a population which was projected to be 180 million by the year 2000, Brazil offers significant market potential. Per capita GDP remains low (US$ 2,796) and very unequal, only 4 % of the population is on a level comparable to that of the industrialized countries. However, implementation in July 1994 of the "Real plan", designed to stabilize the economy and curb hyperinflation, has helped regenerate consumption of food products by the classes with least purchasing power, since that of the higher income classes generally remains inelastic in the face of inflation. The Brazilian agro-food industry is currently reorganizing itself in response, on the one hand, to the new economic context of international openness, marked by the arrival of imported products and the creation of the Southern Common Market (Mercosur); and on the other hand, to the growing importance of large distribution companies. This has led to improved interaction between the production system and the primary transformation stage, increased external competition in manufactured or semi-manufactured goods and launching of more new products (425 in 1992, compared with 263 in 1991 in the 20 main food product sectors). Small and Medium Scale Enterprises (SMEs) have an important role to play in this new context, a fact which they are aware, although they also know that innovation and increased competitiveness are essential to their survival. They face many limitations, such as low profitability (around 6%) compared with other sectors of the industry (16-20 %), lack of financial resources, a large untrained work force, processing techniques rooted in tradition, scant concern for hygiene, lack of technical assistance with their equipment and technological information and inadequate business management. Furthermore, these limitations have, in a general way, been accentuated by uncertainty about the Brazilian economy and lack of confidence in the country's industrial policy. These are factors which are now being dispelled through the stabilization of the economy, notwithstanding the lack of links with universities and research centres. The initiatives which have been taken by the public authorities (tax deductions on investments in R&D), the contribution of parastatal institutions such as SEBRAE (Brazilian Support Service for SMEs) in providing technical and financial assistance to micro enterprises and SMEs and the sensitization of the university sector and its role in supporting the community are all favourable elements which can help eliminate these obstacles and promote agro-food development through micro, small and medium-scale enterprises.

Cassava Processing Techniques in Brazil

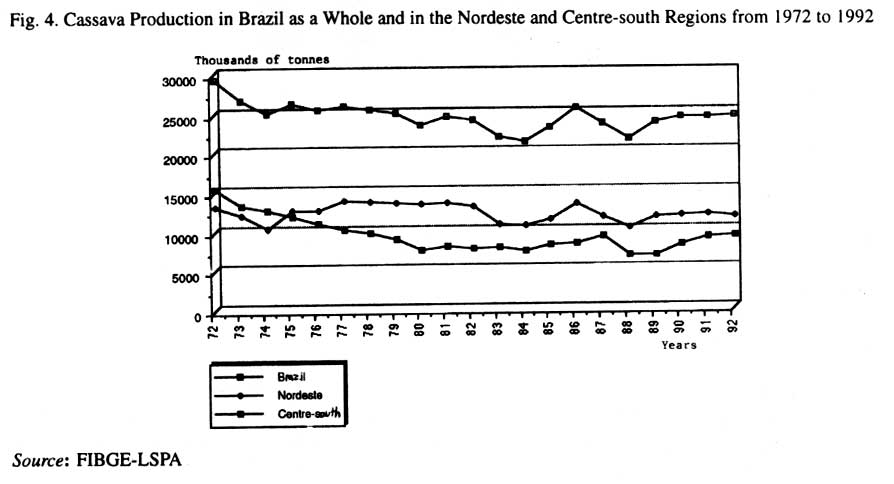

For the last 10 years, Brazil's cassava production has stood at between 22 and 25 million tonnes (Fig. 4) with an area under cultivation of 1.9 million hectares. This, however, falls short of the production level of 30 million tonnes reached during the 1970s. These differences between the 1970s and 1990s are due to various factors:

The central-south region, which produced farinha de raspas (dried, ground and sieved cassava chips) for the bread-making market and farinha de mandioca (table flour) for consumption in the Nordeste region, therefore saw its cultivated area diminish by over half between 1970 and 1980, the hardest-hit states being Sao Paulo (74.5%), Rio Grande do Sul (63.4%) and Santa Catarina (61.7%). Production, which had stood at 15-16 million tonnes during the 1970s, compared with 12-13 million in the Nordeste, has shrunk to around 8 million tonnes in recent years. The impact at national level was less noticeable, with a reduction in the cultivated area of 8-9%. However, this period also saw a decrease in yield per hectare, principally in the Nordeste. With the decrease in cultivated area in the central-south region, the Nordeste has currently become the main cassava-producing area, with 58% of the area under cultivation and 45% of national production, compared with 24 and 34%, respectively, in the central-south region. There is still a marked disparity between the two regions in terms of farming methods and technological level of productivity, with respective average yields of 9.5 and 17 tonnes per hectare. From 1992 onwards, an increase in cassava farming took place in conjunction with the installation of new starch manufacturing plants and farinheras (flour mills), mainly in the states of Paraná and Mato Grosso do Sul. This renewal has been accompanied by the adoption by farmers of new technologies (e.g., varieties and farming practices), leading to a significant increase in yields of as much as 40 tonnes per hectare over 10 months. The best example is that of the state of Paraná, which regained its 1970s production level (2.2 million tonnes, after having dropped to only 800,000 tonnes during the 1980s). In contrast, the state of Santa Catarina, which produced over three million tonnes during the 1970s, today produces only one million, due to climatic conditions (viz., cold continental climate) under which the local varieties have a long growth cycle (16-18 months). Within the Nordeste region, although the state of Bahia is still the largest producer at national level (4.2 million tonnes), it should be noted that there has been a boom in cassava production in the states of Para (from 850,000 to 2.6 million tonnes) and Plaiul (from 540,000 to 1.1 million tonnes), while production has declined in the states of Ceara (from 1.9 to one million tonnes), Amazonia (from 2 million to 1.7 million tonnes) and Pernambuco (over 1.6 million tonnes). These changes in production levels are systematically linked to the appearance or disappearance of markets focused on the region, as the case may be.

Cassava Derivatives in Brazil The main cassava derivatives found in Brazil are:

1. Fresh cassava

Fresh cassava is sold on the local markets for direct consumption. Various industrialized products are targeted principally at urban markets reaching the middle and upper social strata through distribution to supermarkets, of frozen products such as cassava chips and ready-to-use doughs.

2. Farinha de mandioca

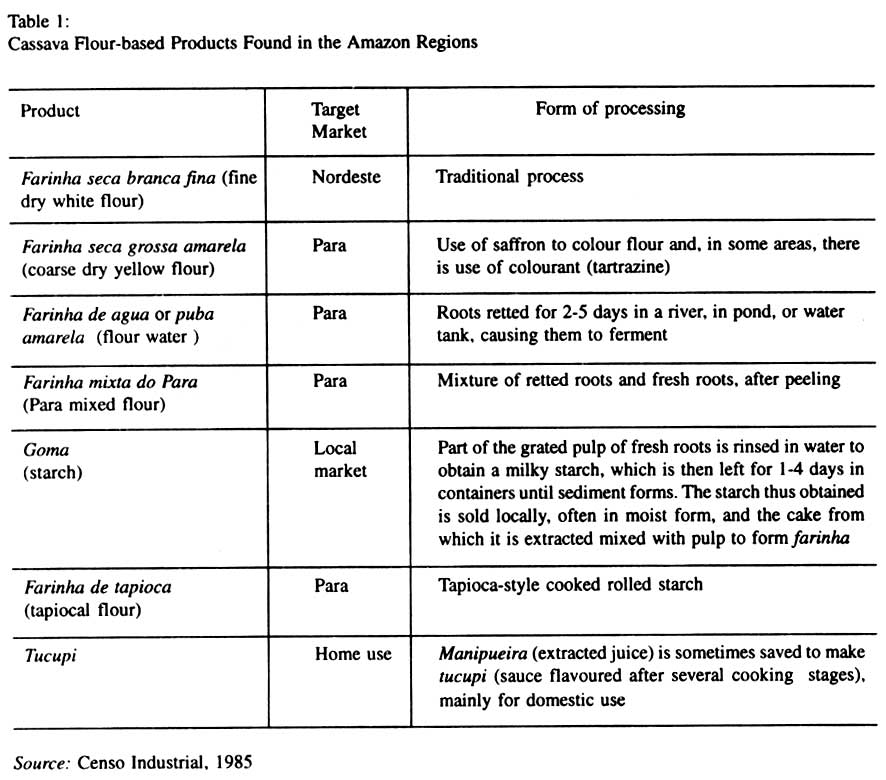

As mentioned previously, farihna continues to be the main product obtained from cassava. However, it is difficult to categorize farihna as a single product, either in terms of the finished article, which varies widely in appearance (particle size, colour) and flavour (crunchiness, roasting, slight fermentation, cooking level) or in terms of the different levels of technology employed in casas de farihna (flour houses) of the Nordeste and in farinheras (flour mills) in the south of the country. The procedure does, however, involve the same stages: washing, stripping, peeling (in the most rustic production units), grating, pressing and sieving, cooking or roasting and possibly grinding and sieving. In the Amazon regions, whole roots may be retted (as farinha de agua, or as flour water) or the pulp fermented. Table 1 illustrates this diversity of technique and possible uses of the by-products in the state of Para. In the southern regions, apart from farinha branca fina (fine white flour) for markets in the Nordeste and Sao Paulo, farinha branca grossa (coarse white flour) and beiju ( toasted flour in pancake strips), are also to be found. Farinha production in northern Brazil takes place in casas de farinha (flour houses), of which there are estimated to be around 400,000 in the country. These are usually family-run enterprises, with the capacity to produce two to three 60 kg sacks of flour a day in the case of the smallest ones, while the largest produce up to 2,000-3,000 kg a day. Pressing is done in traditional wooden presses from one day to the next. Small units are disadvantaged when it comes to the drying/toasting stage of the process, since this involves hand-tossing the farinha on a circular steel plate, requiring 3-31/2 hours for a batch of around 90 kg of farinha. However, many casas de farinha have ovens in which the pulp is mechanically fed and tossed. Families which do not have their own casa de farinha, take their cassava to a neighbouring unit, paying the owner in kind, with part of the end product. In southern Brazil, all operations are mechanized, with the capacity to process up to 50 tonnes of fresh roots a day. The equipment used is locally built or put together by the entrepreneurs themselves, involving a continuous rinsing process, grating, hydraulic presses, grinding-sieving equipment and planetary ovens. The machinery is by no means recent in design and even the newest farinhera still uses this technology. Thus, in the state of Sao Paulo alone, farinha is produced by some 110 enterprises, employing over 1,500 persons, with output of 190,000 tonnes per year. Some enterprises have specialized in the beneficiamiento (processing) of farinha, which they buy from isolated producers in order to treat (grind, sieve, grade) and market it. A major problem linked with farinha production is environmental contamination by waste water from the pressing process (manipueira), with about 300 litres being generated per tonne of fresh roots treated. Disposal takes place either directly into the environment or into lakes. Manipueira is highly toxic, with a chemical oxygen demand (COD) of between 6,000 and 50,000 mg/1, a biochemical oxygen demand (BOD) of 1,500-35,000 mg/1 and a cyanide content of up to 500 parts per million (ppm). Various options have been researched in an effort to solve the manipueira problem, whether through treating the effluent by anaerobic means, using it as a substrate to obtain metabolites (citric acid) by fermentation or oleaginous protein biomass, or spreading it either as ferti-irrigation or as an agricultural barrier. Whatever level of technology is used, the fluid yield remains around 30%. It is interesting to note that, in contrast to findings in African countries, the residual cyanide content of farinha is less than 20 ppm, even in the case of bitter varieties. The fact that the roots are only scraped, leaving the outer skin, which despite having a higher cyanide content is also richer in linamarase, must affect the detoxication process. The farinha market undergoes considerable fluctuation (prices range from US$120 to US$250 per tonne), depending on production in the Nordeste, which is also one of the largest centres of consumption, with significant repercussions on the price of farinha and, by extension, the raw material. Per capita consumption is estimated at 46.1 kg in Belem (Amazonian region), 14.7 kg in Recife (Nordeste) and 1.3 kg in Sao Paulo, although in view of its size, the latter represents a market of around 200,000 tonnes of farinha.

3. Farinha de raspa

This area of production, which until the 1970s was significant due to the use of cassava flour in breadmaking, is now almost non-existent. Only around 200 small-scale units, mostly in the state of Ceara in the Nordeste, produce cassava flakes for animal feed, with an estimated annual output of 8,000 tonnes.

4. Sour starch

Sour starch is a typically Latin American product, found in Colombia, Ecuador, Bolivia, Paraguay, northern Argentina (almidon agrio) and Brazil (polvilho azedo). It is cassava starch extracted by the wet method, naturally fermented in tanks for three to six weeks and dried in the sun. This process gives cassava starch bread-making qualities, also organoleptic and functional properties, which render it irreplaceable in the elaboration of traditional cheese breads. It is produced mainly in the state of Minas Gerais, where there are around 350 processing units in the centre of the country and in the states of Paraná and Santa Catarina, in the south. Estimated annual production is 22,000-24,000 tonnes. The technology used is also very varied, with some units processing 2-5 tonnes of fresh roots a day, while others process as much as 100 tonnes. Once the cassava roots have been washed, they are ground or grated and the starch extracted by the wet method. Different extraction equipment is used, depending on the level of technology: either by the discontinuous method using a revolving drum covered in canvas nylon or bronze mesh and fitted on the inside, with blades to mix the pulp with extraction water or by the continuous method using extractors with a trough-shaped sieve 6-8 metres long, fitted with a series of brushes attached to a rotating axis along its whole length, or batteries of centrifugal extractors, possibly completing the process by rinsing the starchy milk in a vibratory sieve. The starch is separated by settling, either in sedimentation tanks in the case of small plants, or in zig-zag settling troughs measuring 100-150 metres in length. Whatever the technological level, the two key stages in the process - fermentation and drying are carried out in a similar fashion: the starch is fermented in tanks of 1-5 m3 capacity for 20-30 days and dried in the sun on drying surfaces or racks, which can stretch over a distance of 20 kilometres. Apart from being sold for direct household consumption, sour starch is a commodity used in secondary processing industries and bakeries, cake shops and cafes. In large urban centres, cheese breads (pao de queijo, biscoito) are popularly eaten as an accompaniment to coffee, as snack food or as treats during the day. Numerous fast-food outlets have sprung up alongside traditional shops, specializing in cheese breads, often in the form of franchise networks targeting the middle and upper classes. In addition, new products based on sour starch (frozen dough, instant mixes, etc.), are marketed to counter the problems of availability facing urban consumers. The sour starch market also undergoes huge fluctuations, with prices varying from US$136 to US$ 638 a tonne in the state of Minas Gerais in 1993, while the raw material varied by as much as US$26.70 to US$ 57.30 a tonne.

5. Cassava starch

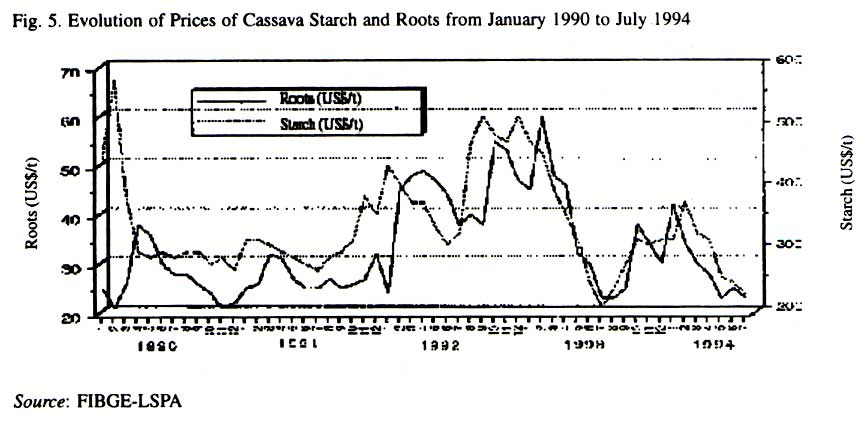

Production of cassava starch was developed during the 1970s in southern Brazil, mainly in the state of Santa Catarina, as an alternative for the bread flour market. Since the flour enterprises were sited close to water sources, which provided energy, some of them were able to use their proximity to water to branch out into starch extraction. This activity later shifted into the neighbouring states of Sao Paulo and in particular, Paraná, which now produces over half the national output, as well as more recently Mato Grosso, which offered more favourable cassava-growing conditions (a variety of short cycles with yields of up to 40 or more tonnes per hectare). This has encouraged the establishment of some 20 new starch enterprises in the last 10 years. Estimated production is around 250,000 tonnes, but only represents 22% of Brazil's starch consumption, which is based on cornstarch produced by multinationals. Forecasted production by the year 2002, given existing capacities and the pace at which new enterprises are starting up in the south, was in the region of 450,000 tonnes of starch. The industrial fabric of cassava starch producers is far more fragmented, with some 60 family-run businesses and agricultural cooperatives. Their processing capacity is considerable: around 100-500 tonnes of fresh roots a day, with locally-made advanced technology (continuous extractors, turntable centrifuges, vacuum filters, flash-dryers). Furthermore, since the equipment used was developed by some of the sour starch extracting companies, these now also build equipment for cassava starch plants and also sell their technology to neighbouring countries. Unlike the country's cornstarch producers, cassava starch producers chiefly market native starch for the food, cardboard and textile industries. Production of modified cassava starch is still modest (around 40,000 tonnes) and restricted to only three or four enterprises (pre-gelatinized starches, dextrines, oxidized and cationic starches). Development of these modified starches to provide a better response to specific consumer demands is the challenge currently facing the cassava starch sector. Industrialists are aware of this, and this secondary processing needs to be the second stage in the industrialization of this sector, over the next two to three years. Price variations in the raw material, which have some repercussions on starch prices, represent a major handicap for the cassava starch sector (Fig 5.), compared with cornstarch, which remains relatively stable since it is tied to the international market. Furthermore, these variations are often more extreme than in the north of the country due to the seasonal nature of the harvest. They are exacerbated by competition with the farinha industries to meet demand from the Nordeste, changes in agricultural policy and the classic cycle of strong demand-high prices - extensive cultivation of one year, followed by large supply-reduced prices - reduction of cultivation, the next year. Starch producers are increasingly tending towards self-sufficiency, to counter the problem of fluctuations in the price and quantity of raw material and as a means of integrating agricultural supply through planned cultivation.

Almost 45% of cassava starch is marketed through wholesalers, with retail sale going mainly to the food (22.5%), meat (11.2%), paper (7.6%) and textile (4.1%) industries.

6. Sago

Sago, often called tapioca, is a rolled, pre-cooked cassava starch. It has a "pearl-like" appearance and is used for desserts and baby foods. Annual production, 80% of which comes from five companies, is estimated at 8,000 tonnes and is mainly marketed through supermarket chains. The Sao Paulo market absorbs 45% of sago production. This product is an interesting diversification for starch producers, enabling them to widen their product range and giving added value to the starch they produce.

New products and markets

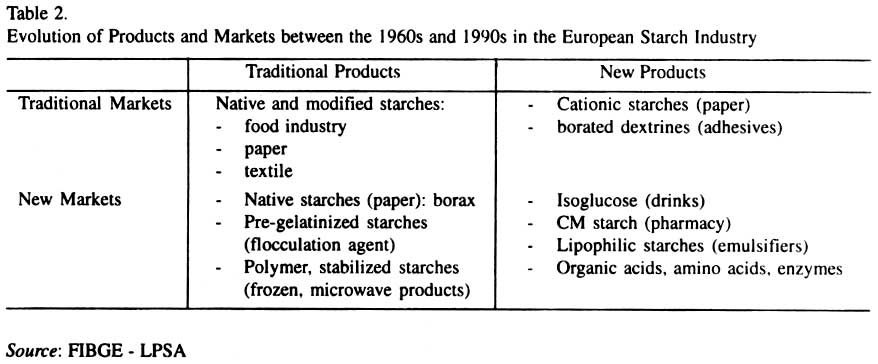

The diversity of products which can be obtained from cassava and their possible applications in the agro-food, industrial, and animal feed sectors, offer prospects of a wide range of outlets for both new and traditional products, on both existing and potential markets, as these develop. An approach based on the "traditional products/new products" versus "traditional markets/new markets" matrix, should lead to a clearer definition of an appropriate product development policy and the role to be played by the various economic agents of each subsector. Examination of the starch industry in Europe, provides a good example of a successful industrial sector at the forefront of innovations in response to evolving markets. From ancient times until the early nineteenth century, the sole product was wheatstarch for non-food uses such as papyrus, paper glue and textiles. During the industrial revolution in the 18th century, the advent of beetroot and glucose, transformed traditional starch extraction activities into an industry offering a wide range of starch applications. The discovery of dextrines in 1820, lintners in the 1890s and more recently, modified starches in the 1940s, has resulted in the industry as it is today. In recent decades from the 1960s to the 1990s, the European industry has seen

an increase in starch consumption, with an average annual growth rate of 3.8%.

Larger amounts (48 to 52%) of starch are being used for non-food purposes and

far-reaching market changes, such as development of paper industries, demand

from the fine chemical and pharmaceutical sectors and a significant decline

in the traditional textile market.

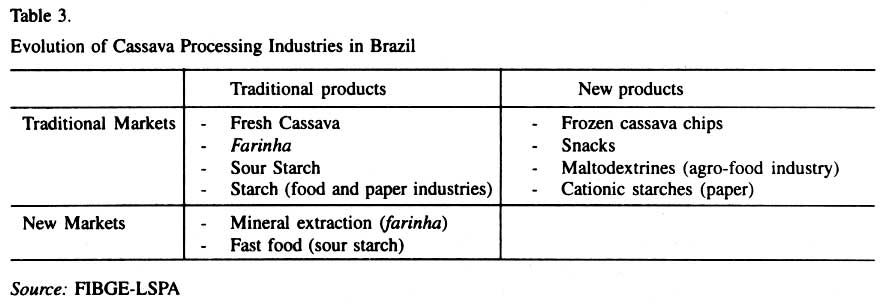

1. Traditional markets/new products

The development of cationic starches with increased retention capacity, has made it possible to strengthen the traditional market in the paper industry.

2. Traditional products/new markets

The food industry has greatly evolved in recent years, presenting new market opportunities for modified starches, such as:

3. New products/new markets

The development of isoglucose has opened up significant markets, particularly that of carbonated beverages in the United States. Fermentation techniques using starch as a substrate have also opened the doors of the chemical and pharmaceutical industry. The same dynamic can be observed during the 1990s, whether in connection with new uses of starch in the packaging (biodegradable plastics), detergent industries, or with new products (thermoplastic starches, biopolymers, fat substitutes, cyclodextrines). At the close of the twentieth century, this approach has enabled the starch sector to consider in its R&D and marketing policies, new user concerns and demands linked with nutrition, health, quality and environmental preservation. Based on this approach, it is interesting to note that, although farinha remains the main outlet for cassava, the Brazilian cassava processing industries have taken a certain number of initiatives to diversify their markets (Table 3):

4. New markets for traditional products

These include the use of polvilho azedo (sour starch) in food preparations for fast food outlets in urban centres, or the use of farinha in the mining industry.

5. New products for traditional markets These include the use of native or modified starches in the food industry, frozen cassava chips for direct consumption, etc. These diversifications which remain limited, indicate on the one hand that these new products or applications rely on markets which are already clearly identified and on the other hand, that the Brazilian industry has not yet tackled the new products/new markets approach. This latter approach involves much higher risks and calls for efforts in terms of research/development policy, market identification, marketing strategies and by extension, human and financial resources, which the Brazilian cassava processing industry does not at present have at its disposal.

CERAT: A Support Centre for the Cassava Sector A certain number of Brazilian institutions have carried out and continue to engage in R&D on cassava, but their work has been isolated and without mutual consultation or programming. At the initiative of the University of the State of Sao Paulo (UNESP), which has experience in the field of cassava processing and in the treatment and utilization of cassava by-products and waste, a centre has been created within the university, known as CERAT (Centro de Raizes Tropicais, Tropical Roots Centre), in order to provide necessary assistance to the roots and tubers sectors in general and to cassava in particular. The Centre brings together some 50 researchers from UNESP and other universities and research centres and involves institutions supporting development of the industrial sector. It has a multidisciplinary approach, which enables it to address the sector as a whole, embracing aspects of production, processing and commercialization. With the creation of this Centre, an instrument now exists to facilitate liaison with the cassava processing industrial sector. It has a roster of experts able to contribute to the different spheres affecting the sector (agricultural production, processing, commercialization and markets) and offers a number of services in the form of routine analyses. Furthermore, it publishes a bimonthly "fax journal," which establishes a privileged point of communication among economic agents, researchers and developers, providing information of an economic (price of raw material and cassava derivatives in Brazil, market news, global trends) and technical nature (innovations at international level, technology being developed, current lines of research/development) and a question-and-answer service. These activities make it possible to create, a common language uniting researchers and industrialists and mutual trust, both of which are essential if a joint effort is to be made in finding solutions to identified technical problems and in developing technological innovations. At the same time and in consultation with the industrial sector, around 15 lines of research have been established at CERAT to look for innovative products or procedures likely to respond to changes in consumption patterns or to new market opennings. These include:

These lines of R&D, therefore, belong to a new products/new markets dynamic.

6. Conclusions

The agro-food SMEs, which have a major socio-economic impact in Brazil, are facing new challenges. They only have extremely marginal access to scientific and technical information and lack sufficient resources to be able to establish their own internal R&D service. If a policy of innovation is to take off, it is necessary both for the SMEs to become aware of the need for it and agree to play a role as partners in research and development and for there to be an adequate structure of researchers and developers, who are open to the industrial world and ready to listen. This research-industry connection will be a key factor in the development of today's SMEs and of tomorrow's agricultural and food industry. This need is strongly felt in Brazil and numerous actions have already been initiated. The creation of CERAT within the UNESP, which is directed at the cassava sector in particular and the tropical roots sector in general, falls within the context of providing support to both of these sectors. great differences exist between the northern and southern regions in terms of cassava production and processing technology, but they will face identical challenges over the coming years in their efforts to make more effective use of this plant. These include diversification of traditional markets, opening of new markets with secondary process products or new products responding to new consumer demands and changing dietary habits in urban centres and diverting into non-food uses, particularly in the case of starch. Another equally important challenge is to find alternative solutions to the problem of solid and liquid waste, generated by the cassava processing industries, through adequate treatment, which is also economically viable for these micro or small enterprises and better utilization of by-products. The production and processing sectors are aware of these challenges and are attempting to make their professional organisations more dynamic, to mobilize funds to support research, promote cassava and its derivatives and develop a more aggressive marketing policy.

FURTHER READING

Copyright © Quest and Insight Publishers and Friends-of-the Book Foundation, 2001 The following images related to this document are available:Photo images[fn01006f3.jpg] [fn01006f5.jpg] [fn01006t2.jpg] [fn01006f1.jpg] [fn01006f2.jpg] [fn01006t1.jpg] [fn01006f4.jpg] [fn01006t3.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}