|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

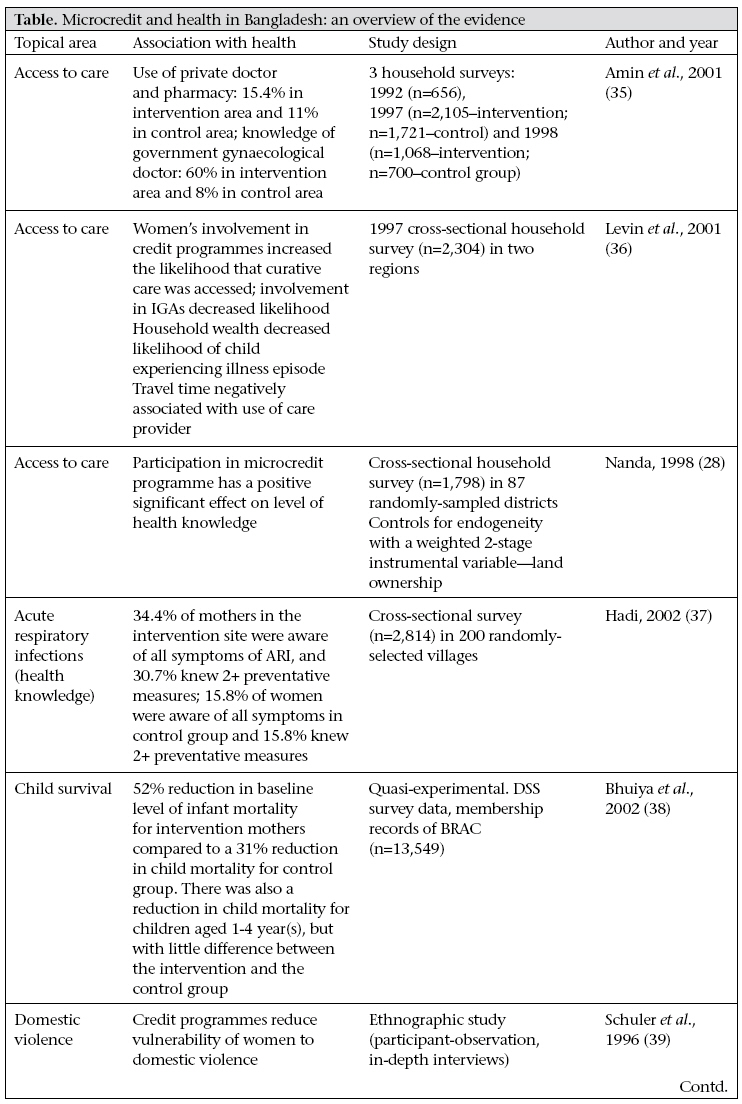

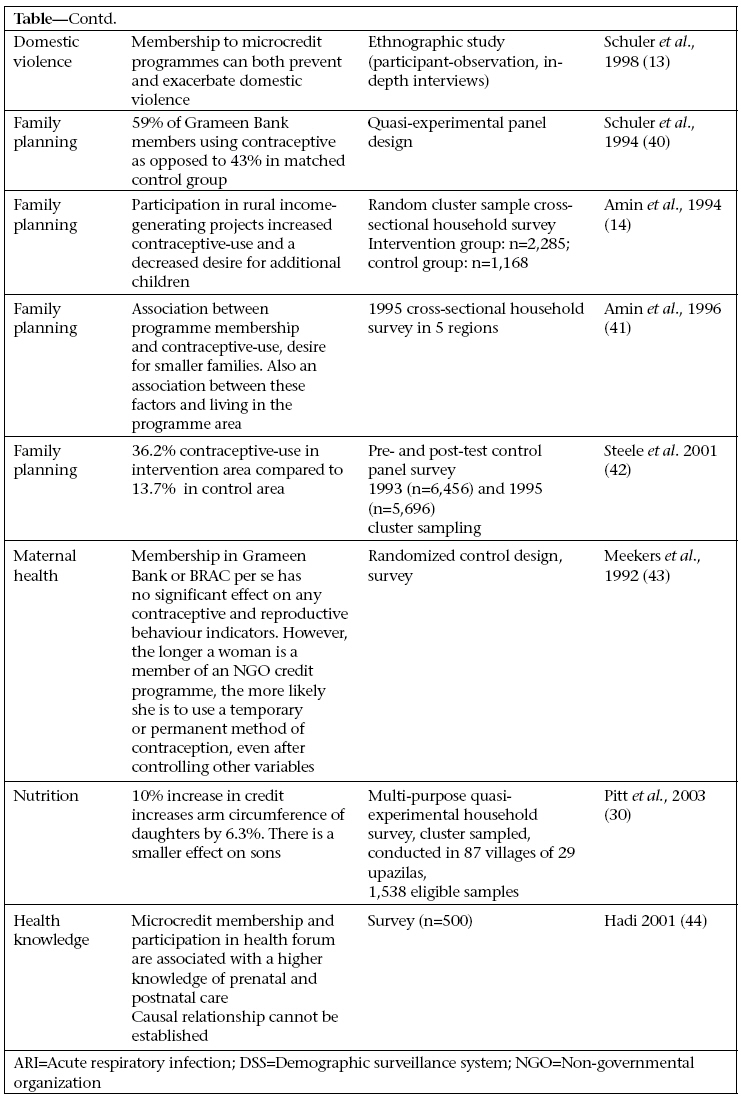

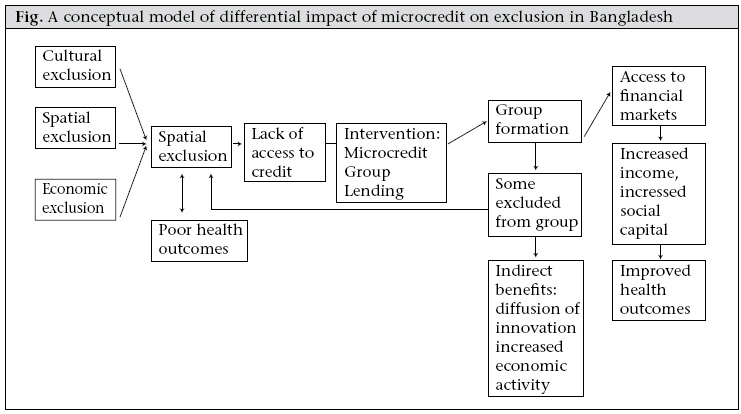

Journal of Health, Population and Nutrition, Vol. 27, No. 4, Aug, 2009, pp. 518-527 The Group-lending Model and Social Closure: Microcredit, Exclusion, and Health in Bangladesh Anna T. Schurmann1 and Heidi Bart Johnston2 1University of North Carolina, Chapel Hill, USA and 2ICDDR,B, GPO Box 128, Dhaka 1000, Bangladesh Code Number: hn09050 ABSTRACT According to social exclusion theory, health risks are positively associated with involuntary social, economic, political and cultural exclusion from society. In this paper, a social exclusion framework has been used, and available literature on microcredit in Bangladesh has been reviewed to explore the available evidence on associations among microcredit, exclusion, and health outcomes. The paper addresses the question of whether participation in group-lending reduces health inequities through promoting social inclusion. The group-lending model of microcredit is a development intervention in which small-scale credit for income-generation activities is provided to groups of individuals who do not have material collateral. The paper outlines four pathways through which microcredit can affect health status: financing care in the event of health emergencies; financing health inputs such as improved nutrition; as a platform for health education; and by increasing social capital through group meetings and mutual support. For many participants, the group-lending model of microcredit can mitigate exclusionary processes and lead to improvements in health for some; for others, it can worsen exclusionary processes which contribute to health disadvantage. Key words: Exclusion; Economic assistance; Health status; Group-lending model; Health equity; Microcredit; Social exclusion; Bangladesh INTRODUCTION According to social exclusion theory, health risks are positively associated with involuntary social, economic, political and cultural exclusion from society. Microcredit is a development intervention designed to reduce poverty through access to credit. While not explicitly designed to impact health as a poverty reduction strategy, microcredit interventions have the potential to empower borrowers, and through several different pathways, improve health. Microcredit programmes have been adapted to different contexts all over the world, in rich and poor countries, with an estimated 92 million clients in the developing world (1). The year 2005 was named the ‘Year of Microcredit’ by the UN’s Economic and Social Council. In 2006, Mohammed Yunus won the Nobel Prize for Peace for his work with the Grameen Bank. We use a social exclusion framework and draw on the available literature on microcredit in Bangladesh to explore associations between participation in microcredit programmes, social exclusion, and health status. We begin with a description of the multiple exclusionary factors that microcredit seeks to combat, specifically poverty, the traditional norms that govern women’s conduct in public, and urban-rural inequalities in wealth and development. We then explain the group-lending model of microcredit, and drawing upon the available evidence, suggest four pathways in which microcredit can impact health. Ultimately, we argue that while group-based microcredit programmes have the potential to help borrowers raise themselves out of poverty, these programmes can also replicate exclusionary processes in society and further health inequity. MICROCREDIT The microcredit movement in Bangladesh is an important story in contemporary development discourse, both because of its origins within the country and because of its reach in the population. The agricultural cycle in Bangladesh has always been closely tied to the provision of credit. Traditionally, small cultivators relied on money-lenders for agricultural inputs or consumption requirements until harvest (2). Provision of formal microcredit, with goals of sustainable poverty reduction, began in 1959 by Akter Hameed Khan in what was called the ‘Comilla Model’ (after a town by the same name) by the Pakistan Rural Development Board (later named the Bangladesh Rural Development Board). However, this experiment achieved only isolated success due to elite capture and a lack of community buy-in. Over time, different strategies of microcredit have been explored, and different finance products developed (all under the broader term of ‘microfinance’). The movement has expanded in the last decades; there are now over 1,500 microfinance institutions in Bangladesh (1). The two primary providers of microcredit in Bangladesh are the Grameen Bank and Building Resources Across Communities (now BRAC, formerly Bangladesh Rural Advancement Committee), both of which started their operations in the late 1970s. These organizations work to tie social development goals with provision of credit. While BRAC uses various interventions to assist the poor and has a strong emphasis on consciousness-raising, Grameen Bank’s main focus is microcredit. Grameen Bank has over 2,247 branches, covering 72,096 villages, with a total of four million borrowers, and BRAC has an estimated 3.6 million borrowers through its 50,000 village organizations (1,3). There are a number of different models of microcredit delivery; however, both BRAC and Grameen Bank use the group-lending model—the model discussed in this paper. The main attribute of the group-lending model of microcredit is the use of social rather than material collateral. Loans are made to small groups or cooperatives, and peer pressure is used for ensuring that repayments are made. In Bangladesh, women are the primary beneficiaries of microcredit programmes—not necessarily out of a feminist impulse but because there is evidence that women are more sensitive to peer pressure and so are more reliable debtors. In the absence of material collateral and credit-rating systems, the group-lending model makes use of information ‘impacted’ in the village about who is a reliable borrower, and villagers reveal such information by using their judgement to select fellow debtors for the small groups. In this way, the group-based lending model both uses and builds upon the social capital of its borrowers. This makes group-based lending efficient and effective, with low transaction costs for the provider (4,5). Any extra income earned through participation in a microcredit scheme can be spent on what microcredit clients (or their households) see as their highest priority; so, the intervention can be viewed as less paternalistic and more enabling than other development interventions (6). While microcredit is an indigenous solution to local poverty in Bangladesh, many international actors were instrumental in its growth and expansion, including Chicago’s South Shore Bank, the Ford Foundation, and the World Bank. The many different donors have brought different priorities and ideologies, reporting procedures, and indicators that have shaped the practice of microcredit (7). EXCLUSION IN BANGLADESH In this analysis, we explore the available evidence on associations between microcredit and exclusion and health status. Processes that create inequities have traditionally been understood in terms of market exploitation, or the extraction of surplus value. However, market exploitation alone does not account for many inequity-producing processes. The social processes that ‘shut out’ certain categories of people from the benefits of participation could better be described as exclusion or social exclusion (8). This analysis explores the factors that have traditionally excluded certain groups from financial markets in Bangladesh. The principal factors identified are poverty (economic exclusion), regional disparities (spatial exclusion), and the low-status of women (cultural exclusion). This analysis presents each of these factors in isolation, but in reality, these factors compound each other as components of deprivation and exclusion and have causal and dynamic connections (9). The figure is a conceptual model depicting the relationship of social exclusion to poor health outcomes in Bangladesh as described in this paper. The model depicts that cultural, spatial and economic exclusions are encompassed under the umbrella of ‘social exclusion’. Economic exclusion The poverty levels in Bangladesh have always been high. Post-independence levels of income poverty in Bangladesh in the mid-1970s were estimated at 70-80%. With rates of economic growth over 5% annually, poverty rates in Bangladesh have been declining by about 1% a year since the 1990s (10). According to the 2005 estimates, the poverty level is 40% in urban and 44% in rural Bangladesh. This overall decline in poverty masks the concurrent increase in income and asset inequality, with rural areas at a particular disadvantage. The Gini coefficient for consumption expenditure for rural areas rose from 0.28 in 1991-1992 to 0.31 by 2000. In urban areas, it climbed from 0.36 to 0.41 (9). The poor are not a homogenous group. While estimates vary, about 10% of the poor can be classified as ‘ultra-poor’ as measured by indicators, such as low consumption, low height-for-age, no formal education, high rates of infant mortality, and lack of access to essential services (10). This segment of the population is particularly vulnerable to factors that will increase deprivation: loss of assets (due to flooding for example), health emergencies, unstable livelihoods, and poor sanitation. Such chronic insecurity often leads to livelihood strategies that prevent mobility out of poverty, such as irregular day labour, begging, or sex work (11). Spatial exclusion The rural poor are not only excluded from economic growth through lack of financial resources and assets but also through their distance from opportunities in the urban economy. There is also spatial disadvantage within rural areas associated with low ‘geographic capital’: uneven distribution of services and infrastructure, low agricultural or resource potential, and weak economic and transport linkages (9,11,12). Data on rural poverty levels since 2000 vary from 61% in Rajshahi to 40% in Barisal (11). However, the importance of place to variation in health is not just a matter of geography but also dynamic social and political relationships (11,12). For example, particular electorates may be favoured as vote-banks during the election cycle. Cultural exclusion—purdah Purdah is a social and Islamic religious tradition that prohibits women from mixing with men who are not blood relatives, after the onset of menarche. Norms vary but generally purdah denies women access to productive capital and markets (13); women in purdah are not allowed to work, touch money, or go to the market. While restrictions are, to an extent, negotiable (2), adhering to purdah grants status and privilege, and conversely, violating purdah means loss of status and can be a sign of downward economic mobility. Typically, purdah confines women’s work to the domestic sphere where it is under-valued and not remunerated. For example, if women work outside the household during the peak agricultural season, they would normally be paid in kind, not in cash to avoid violation of purdah (14). Restriction to the domestic sphere limits social networks, participation in civil society, and a voice in policy dialogue. TARGETING THE EXCLUDED In the previous section, barriers to inclusion in financial markets are described. Microcredit interventions need to overcome these barriers to reach those in need to be able to claim success. The clientele for microcredit are generally subsistence level, economically active, poor rural women. However, the programmatic targeting practices vary according to the priorities of the lender. If more reliable debtors are targeted, the transformative potential of microcredit to help the poorest is lower, but the profitability and sustainability are higher. This section describes how microcredit fares in targeting those most in need as it balances the contrary imperatives of reach and sustainability. Targeting the ultra-poor Borrowers with assets and skills are able to make better use of credit and provide lenders with higher returns (15). In his study of characteristics of poverty dynamics in Bangladesh, Sen found that rural ascendent households had greater access to credit than chronically poor and descendent households, suggesting that access to financial capital was an important element in the climb out of poverty (11). At the same time, the ultra-poor and descendent individuals and households typically face barriers to joining traditional microcredit programmes, such as lacking the initial endowment (material and non-material collateral), high opportunity costs, and limited capacity for labour substitution. Even when included in microcredit programmes, some groups, such as landless casual labourers, are less able to benefit because they do not have a regular income that would enable them to commit to repayments, including interest. A loan for such borrowers only means increased insecurity and risk (5). It is generally acknowledged that traditional group-lending microcredit programmes are not appropriate for the ultra-poor, see for example, the World Bank’s Consultative Group’s ‘Key Principles’ (16). By benefiting only the marginally poor, microcredit can further isolate the ultra-poor by increasing inequality. In response to this, BRAC has developed a programme specifically to target the ultra-poor with the aim of enabling them to gain the resources necessary to gainfully participate in traditional microcredit programmes (17). When the ultra-poor are specifically targeted as clients, conditionalities are often more generous; for example, the loans may be small with no interest and no repayment timeframe (17). Targetting rural areas Microcredit programmes in Bangladesh have generally concentrated in rural areas and have achieved many successes. However, as mentioned earlier, Bangladesh has many rural areas that are vulnerable to flooding, have poor transport infrastructure, and are otherwise economically less viable. As programmatic sustainability is more difficult in such areas (18,42), these are less attractive to microcredit programme implementers and are avoided. Residents of areas with low geographic capital still face barriers to accessing financial markets (18). Targeting women Targeting is also gendered since microcredit generally focuses on women as efficient agents for the welfare of the household and as low-risk borrowers. Women present less credit risks, with default rates of only 3% compared to 10% for men (19). As debtors, women are seen as more passive, submissive, and vulnerable, making them more liable to make repayments (18). Repayments and debt collection can put significant pressure on women because they do not necessarily directly control household resources (20). While the burden of repayments are borne by women, the loan itself and income from microenterprise are often passed onto husbands or sons (21). This means that the ability of microcredit to empower women cannot be measured through client lists or timely repayments. Kabeer, instead, suggests that the measurement of empowerment needs to be within the local context, taking into account the perceptions of the beneficiaries themselves (2). Of course, impact is unlikely to be even. Women are not a homogenous group, and their contexts differ. Different individuals in different situations are likely to take advantage of different opportunities in different ways, or not at all. As previously mentioned, those with assets and skills, those closer to towns with access to opportunities for commerce, and those with more support from their families are more likely to benefit from microcredit. To participate in microcredit activities, women must negotiate purdah barriers and balance microcredit obligations with childcare, subsistence, and other domestic duties. Compared to entry into the formal labour sector (e.g. a job in a garment factory), microcredit is easier to accommodate with purdah restrictions and household and childcare commitments. Thus, microcredit can serve as an intervention to assist women and households in the transition from the declining agricultural sector into the formal sector. SOCIAL CAPITAL AND SOCIAL EXCLUSION Through regular group meetings, group-based lending models of microfinance programming can develop new social capital and networks for participants. The mutual support and solidarity of the group provides an atmosphere of collective selfinterest (4). As a result, those who traditionally have been marginalized may become more organized and gain a stronger voice, which can lead to higher levels of political awareness and participation (2). However, the transformative potential of enhanced social capital should not be overstated. Success of microfinance depends on peer pressure (social collateral) as a substitute for material collateral and insurance against late or non-payment. Peer pressure, in turn, depends on membership to the group, or social inclusion. Peer pressure is used both as a disciplinary and support mechanism within microcredit, and the balance between these two functions is a fine one. Goetz finds that the emphasis on peer pressure as a disciplinary force in BRAC microcredit groups has undermined trust and support and increases the likelihood that the poor and most vulnerable will be excluded (20). People who lapse on their payments are punished with reclamation of their assets but, more importantly, non-payment results in social sanction. In an ethnographic study, Todd provides a further account of social relationships within microcredit programmes (22).Todd foundthat groupsolidarity is tenuous and does not usurp or disrupt traditional kin or patron-client networks, where stronger loyalties tend to reside. Indeed, such relationships are key to women’s survival and success in microcredit programmes. Todd points out “these (kin and patron-client) relationships are vital to women because they are dependent, but they can also be used to negotiate their independence.” Todd also reports that successful members of credit groups are highly intolerant of less successful group members, even when the lack of success was clearly not their fault. Failure to meet group norms can lead to social exclusion (22). While microcredit counters the exclusion of the poor from access to formal lending, it does not cater to those who are subjected to high levels of exclusion. The logic of relying on social collateral rather than materialcollateral inherently meansthat there will always be some who are excluded (for example, widows, migrant labourers, single mothers, people with stigmatizing illnesses). Inequalities in social collateral lead to unequal access to microcredit and its potential benefits (8,21). Unfortunately, women are not judged on their own merit alone, but often risk being denied participation in lending groups if their husbands drink or gamble, or otherwise pose a credit risk (18,21). In these instances, microcredit reinforces existing social processes of exclusion (8). MICROCREDIT, MEASUREMENT, AND HEALTH STATUS Participation in microcredit programmes is associated with positive health behaviours and outcomes in numerous studies (Table 1, 1 cont'd) (for a meta-analysis, see also Morduch J, 2001). However, these data need to be viewed with some caution. The socially-embedded nature of microcredit group makes causality difficult to prove (7,23). Membership in credit groups depends and builds on social capital, which may itself be correlated with education and healthcare-seeking behaviours. Women who join microcredit programmes likely have access to more social capital from the outset. This point is demonstrated by Steele et al. (1998), who used a quasi-experimental panel design to identify the characteristics of women who chose to join microcredit programmes (21,24). Theyfound that the women who joined were relatively educated and socially independent compared to those who did not join. However, after controlling for this selection bias, they still identified a positive impact with regard to children’s education, age at marriage, and use of modern contraception. On the other hand, Mahmud suggests that selection bias goes the other way, with the least empowered women being the most likely clients of microcredit (24). Either way, selection bias provides a hurdle to proving causality, even with multivariate analysis. One must consider that microcredit may only help those who are already economically ascendant. Similarly, the pathways from microcredit to health are not always explicit. This analysis draws on the literature to suggest four broad pathways in which microcredit could have a positive impact. For the purpose of this analysis, these are presented as unique pathways. In reality, the pathways cross and intermingle, their individual impact difficult to tease out. First, microcredit serves as a medium to communicate health messages. When borrowers participate in regular repayment meetings, they may be (depending on the programme) provided with health education or service provision, increasing their knowledge of and access to formal healthcare. The regular meetings associated with the group-based lending models of microfinance programming provide a forum for education and training. BRAC programmes, more often than Grameen Bank, capitalize on this opportunity to provide regular contact with a health educator. Grameen Kalyan (the healthcare arm of Grameen Bank) now provides primary healthcare services in operational areas and ancillary health services, such as health insurance (25). Providing learning opportunities alongside credit is not just altruism on the part of the lender; increasing general capacity of the poor cultivates more capable clients (4). Ill-health is the most common reason for loan defaulting, which benefits neither the lender nor the borrower. Microcredit participants are likely to be influential within their social network due to their upward mobility (typical ‘innovators’), and new health knowledge and behaviours are likely to diffuse quickly from group participants to the rest of the community (26). Second, microcredit can improve the general quality of life of borrowers by increasing disposable income, reducing vulnerability through diversifying income sources, strengthening financial shock-coping mechanisms (insurance, savings), and building assets. A large literature demonstrates the bi-directional relationships between health and economic status (27). Nanda documented that income from microcredit increased women’s perceived and actual contribution to the household. This resulted in a positive impact on their decisions to seek quality healthcare (28). Evidence has also shown that women are more likely than men to spend earned income to benefit the entire household on items, such as food, education, and asset building (29). Pitt et al. found that access of women to credit from group-based credit programmes had a large and statistically significant effect on the health of both boy and girl children whereas access of men to credit had no effect (30). There is also evidence that increased income for women improves child and maternal health through increased school attendance and increased contraceptive use (Table 1, 1 cont'd). Third, availability of credit can assist the poor with financing health emergencies, such as ill-health of the main breadwinner. The main difference from the point above is the immediacy of a need to finance a curative health emergency as opposed to a slower process of building a healthier and more secure household. Health emergencies are strongly related to impoverishment in Bangladesh. Costs of treatment and medicines can easily consume an entire household budget, especially if the household members do not have a regular source of income. Sale of productive assets to pay for healthcare often leads households into downward trajectories, pushing families into the category of ‘ultra-poor’ (8,31). The final pathway is building social capital through group meetings and mutual support, which has been demonstrated to improve health in and of itself (32). The social interaction in the group meetings has been found to play an important role in the diffusion of innovative behaviours such as contraceptive-use (23). However, as Portes has pointed out, social capital can equally function in both an exclusive or inclusive way—with positive welfare effects from some and negative for others (33,34). This paper suggests that this is the likely outcome of group-based lending interventions; with economic and social benefits for those included within the lending group, and a denial of benefits to those purposefully excluded from the group. In this way, the mechanisms of group closure are re-aligned according to group credit membership (23). However, the impact of exclusion from microcredit on health requires further study as most studies compare microcredit participants to a control group, not to those who were excluded from joining a microcredit group. DISCUSSION A substantial body of literature about microcredit in Bangladesh shows that participation in a microcredit programme is associated with improved health behaviours and outcomes. Using social exclusion theory and drawing upon the literature around social capital, this analysis unpacks the relationships between microcredit and health, suggesting that microcredit has the potential to improve the health of participants. However, typical of a market-based solution, it is not equitable. By excluding individuals through the social processes of group formation, individuals and households are also excluded from the compounded benefits of microcredit, including the social support it engenders (Fig.). In this way, it replaces the economic exclusions of the market with exclusion through social processes. For this reason, it cannot be relied upon to ensure health equity. Social exclusion analysis helps reveal the exclusions perpetuated by microcredit. While it can be an effective and transformative intervention, it should not be implemented at the expense of other interventions, such as infrastructure projects, service provision, or targeted subsidies. It cannot replace a vibrant public sector in providing capabilities to the poor for development. However, this article does not suggest a rejection of marketbased solutions to poverty and health inequity. This article argues that complementary interventions are needed to buffer exclusionary impacts of microcredit. CONCLUSION In this paper, we sought to answer whether participation in group-lending reduces health inequities by addressing social exclusion. We applied a social exclusion framework to the available research on microcredit in Bangladesh. We described the exclusionary factors that microcredit attempts to combat, specifically poverty, the traditional norms that govern the conduct of women in public and urbanrural inequalities in wealth and development; we then suggest four pathways in which microcredit affects health. Ultimately, we argued that improving health is one of the most unambiguous benefits of microcredit in Bangladesh. However, microcredit is not an inclusive approach and for this reason is best accompanied with other complementary interventions. Our analysis of microcredit, exclusion, and health is exploratory in nature. The analysis evaluates the impact of microcredit, a poverty-reduction strategy, on health outcomes, while health is not necessarily planned for in the design of the microcredit programme. None of the studies drawn on for this analysis were designed to inform a social exclusion analysis. More research into these relationships is required. Such research will be useful for the continued critique and modification of microcredit in designing new interventions for capability enhancement inclusive of social development and for greater health equity. ACKNOWLEDGEMENTS This work was funded by the World Health Organization (WHO) and undertaken as work for the Social Exclusion Knowledge Network established as part of the WHO Commission on the Social Determinants of Health. The views presented in this manuscript are those of the authors and do not necessarily represent the decisions, policy, or views of WHO or Commissioners. The authors thank the following people for review of and feedback on earlier drafts of this paper: Lisa Basalla, Shelley Golden, Anne Martin Staple, Ruchira Naved, Syed Masud, Wendy Werner, and Jeffrey Motu. REFERENCES

Copyright © International Centre for Diarrhoeal Disease Research, Bangladesh The following images related to this document are available:Photo images[hn09050t1b.jpg] [hn09050t1a.jpg] [hn09050f1.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}