|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

Health Policy and Development Journal, Vol. 2, No. 2, Aug, 2004, pp.144-150 HOW MUCH DO LAB TESTS COST? ANALYSIS OF LACOR HOSPITAL LABORATORY SERVICES Antonella Ninci 1 & Robert Ocakacon 2 1. AISPO Lacor Project. 2. Laboratory Department, Lacor Hospital Code Number: hp04027 AbstractAn analysis of the laboratory activity costs was done in the Laboratory Department of Lacor Hospital in order to calculate the global cost of each test and to evaluate the cost effectiveness of the service. The study is a retrospective analysis on the data related to the financial year 2002-2003. The costs that have been considered are: materials, salaries, equipment and general costs. A table has been outlined with the total cost of each test. The biggest contribution to the laboratory activity cost is given by general costs, which account for 45% of the total, followed by the materials (21%), and then by the salaries and equipment which contribute for 17% each. Most of the tests belong to the medium cost level, that is between 1000 and 2500 USH. Introduction

The analysis of the hospital costs has become more and more important in the last time and it is even more essential in developing countries where the limited resources impose considerable efforts in order to get a good quality of the health care service. St.Mary's Hospital Lacor, in Uganda, was the object of a study conducted by a team from Ngozi University in the financial year 2001-2002. The study identified several cost centres in the hospital and calculated the respective costs by computing all the expenditures for each of them. The Laboratory Department was considered among the ancillary cost centres. The aim of the present analysis is to estimate the burden of the Laboratory costs for each test done. A better knowledge of the actual costs is required for "the promotion of more rational utilization and better appreciation of health laboratory services by medical and public health workers" (Barker and Houang, 1983) (1). Materials and methods

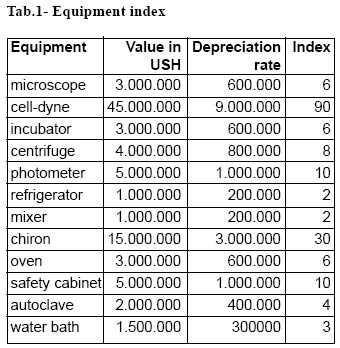

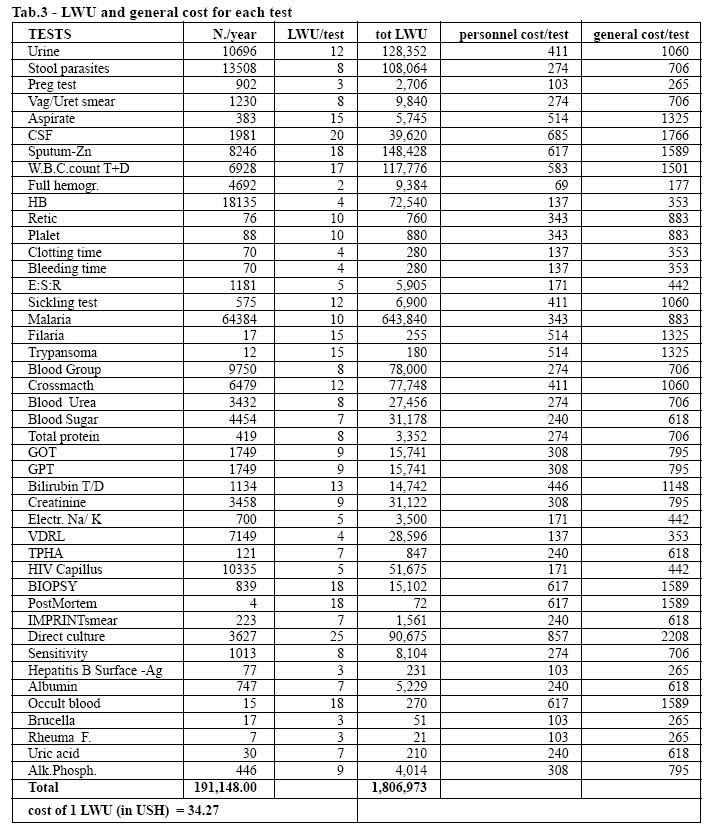

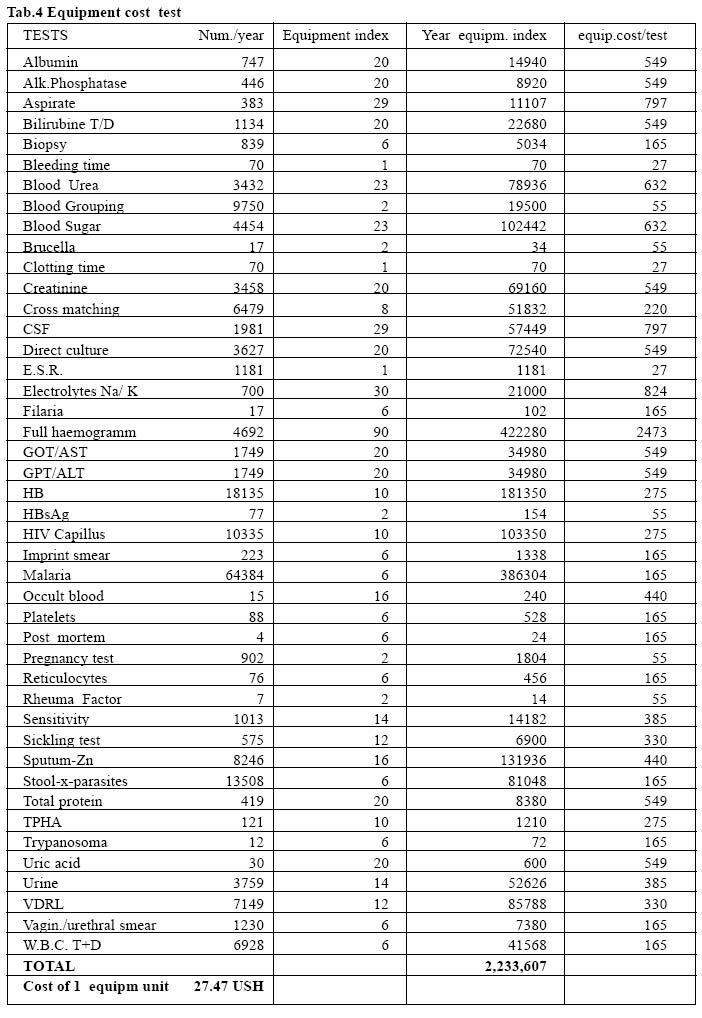

The analysed costs are referred to the tests performed in Lacor Hospital's Laboratory in the financial year 2002-2003, excluding the Health Centres of Pabo and Opit. These costs can be fixed or variable: salaries, materials and consumables are here referred to as variable costs, while equipment and general costs are referred to as fixed costs. The fixed costs were extracted from the Ngozi study concerning the financial year 2001-2002, by assuming that these figures cannot change so much after one year.(2) Salaries: This figure was given by the Personnel Office. It represents the total sum paid by the Hospital for the salaries of technical and auxiliary staff working in the Laboratory and Blood Bank. In this amount also the NSSF and the insurance costs are included. The evaluation of the personnel cost for each test was done through the LWU (Laboratory Workload Unit), an index that has been elaborated by Houang L. for laboratories in developing countries (3). One of these units is equal to 1 minute of technical, clerical and aide time. The LWU counts the time from the reception of the specimen to the issuing of the results but it doesn't consider incubation and waiting time. A LWU value was assigned to each type of test. By knowing the number of tests done in the year, the yearly workload was calculated, first for each test, then for the whole activity of the year (4). The monetary value of each LWU came out by dividing the total expenditure for salaries by the total number of LWU. At the end, multiplying this monetary value by the number of the LWU needed for each test we got the cost of the test in terms of personnel. Materials: To calculate this value, the cost of the materials needed to perform each laboratory test has been computed. The following materials have been considered: diagnostic kits, plastic-ware, glassware, staining reagents, chemical products, culture media. Some items, which are recycled, were considered as 10% of their original value. At the end, the cost of each test was multiplied by the number of test run in the year. An increment of 20% was added to the materials cost for all the tests as rate of reagents "misused" by the students of Lab. Assistant Training course for their practical education. An alternative method to get this cost could have been by summing the amount of the invoices for the Laboratory during the analysed year, but not all the invoices were available and, in addition, some items used in this year were bought in the previous one. Equipment: The expenditure for equipment and for general cost came from the Ngozi's study and it is related to the financial year 2001-2002. This data represents the depreciation of equipment, assuming that they can last five years as internationally recommended for medical equipment, though our equipment lasts much longer. The Ngozi team calculated the annualised value basing on an updated inventory. This amount doesn't include the costs for maintenance and repairing equipment, which was included under "Maintenance", in "General costs". We had to find a way to establish the burden of equipment for the different tests, as some of them are very simple, others require very expensive equipment. We assigned an index to each instrument, derived from its current cost and its depreciation, as it is showed in Tab.1. The following method was used in calculating the equipment use index for each test on the basis of the instruments used to perform it, by summing their related indexes. Successively we got the total equipment use index for all the tests run in the year. The yearly expenditure for maintenance was divided by this total index in order to get the monetary value for one unit of this equipment index. The cost of each test in terms of equipment was found by multiplying the monetary value by the equipment use index of that test (Tab.5). General costs: Under "General costs", the following have been included: administrative costs, security, buildings, maintenance, and pharmacy. The administrative cost is made up of the expenditure for administration management, transport, stationery, guesthouse and it was allocated to the Laboratory for the 7% of the total, according to the number of personnel. Security consists of the annualised cost of the perimeter fencing assigned to the Laboratory for 5% of the total, according to the occupied area. Buildings were computed as annualised value of the premises assuming that they would last for 30 years and they include the lagoon and the incinerator for the management of solid and liquid waste. Under "Maintenance" the costs of electricity, gas and water supply were computed, besides the cost of spare parts and repairing interventions. This cost was allocated to the Laboratory for 5.6% of the total. Pharmacy includes sundries, gloves, needles, syringes, and other disposable items, but not reagents. Results

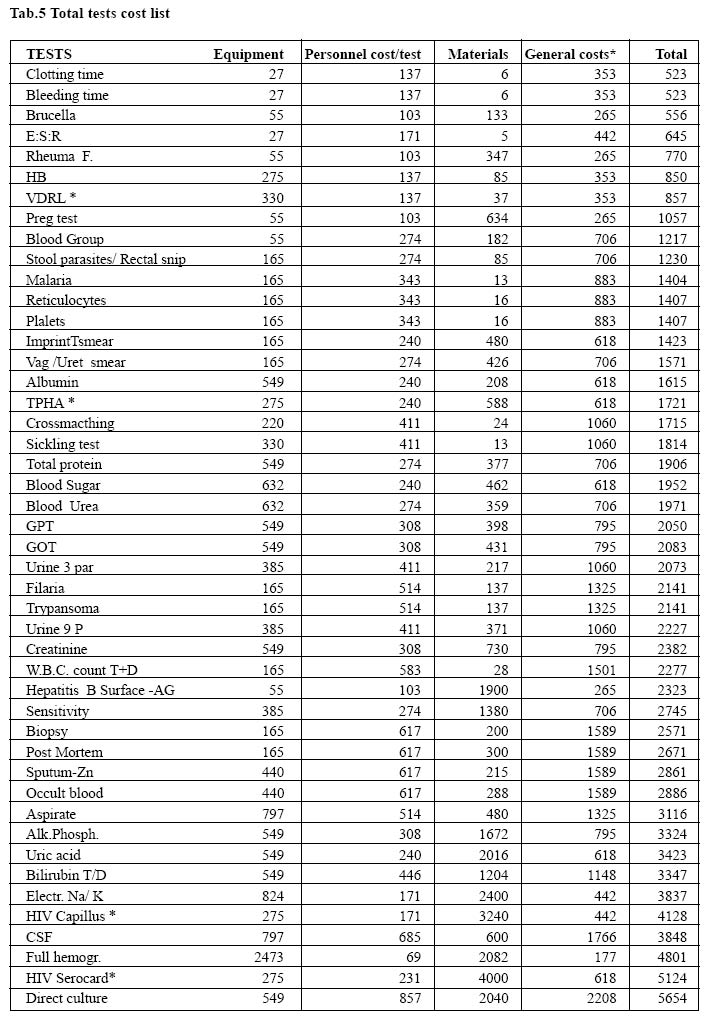

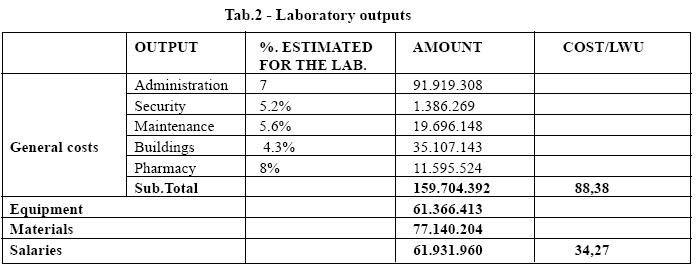

The yearly expenditures for the analysed factors, related to the year 2002-2003 are shown in Tab.2. All the calculations were made on the statistic of the laboratory activity of the same year.

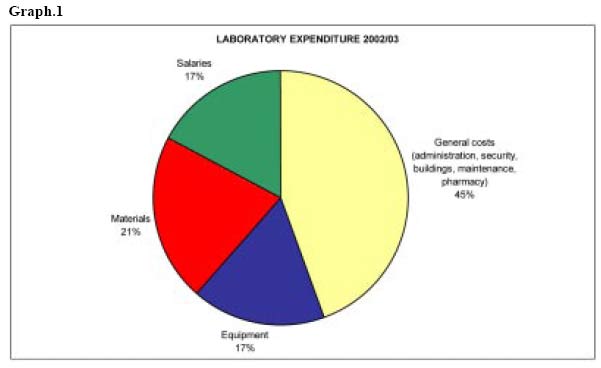

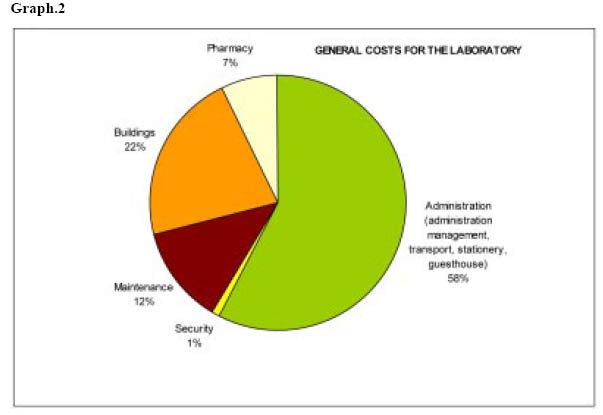

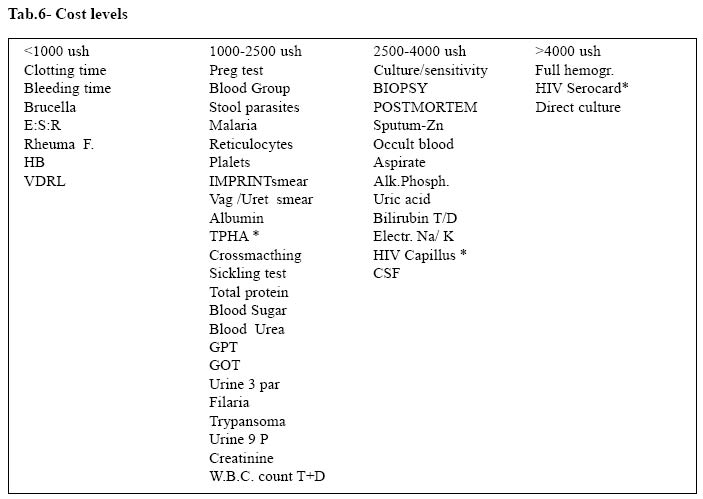

The number of tests done in that period was 191.148, with an increment of 23% compared with the previous year. The LWU value for each test is listed in the attached table n.3. The cost of each LWU was found to be 34 USH. The same table reports the cost of each test in terms of personnel and in terms of general costs. The burden of the general costs was divided up among the tests on the basis of LWU needed for each test; each LWU was given a value of 88 USH in terms of general costs and a value of 34 USH in terms of salaries. For the estimation of the equipment cost, we calculated the monetary value of one unit of the equipment index which was found to be 27 USH. The cost of each test for what the equipment is concerning is listed in the attached table n.4. At the end the contribution of each factor was computed and the total cost for each test was listed in the attached table n.5. The global contribution of each factor to the laboratory which contributes for 21% of the total and then thetests is better showen by the graph.1 . The bigger costs of personnel and equipment which have the same expenditure is due to the general costs which account burden, 17% of the total.for 45% of the total. This is followed by the materials, which contributes for 21% of the total and then the costs of personnel and equipment which have the same burden, 17% of the total. The general cost, however, includes many elements and all its components are represented in graph.2. The administration costs accounts for 58% of the total. The incidence of buildings is estimated for 22%, followed by maintenance expenditure for the 12% and by the costs of pharmacy for 7% of the total. Security depreciation accounts for 1%. According to their total cost, the laboratory tests can be grouped in four cost levels (Tab. 6): < 1000 USH, 1000-2000 USH, 2500-4000 USH, >4000 USH. Most of the tests belong to the intermediate level (1000-2500) CONCLUSIONS

The present analysis is conceived to be a tool of monitoring yearly laboratory expenditure and, consequently, its cost effectiveness. It shows that a relevant part of the laboratory tests costs is due to general costs that represent 45% of the total. This is a common finding also in western hospitals. The cost of each LWU is lower than the one found in the previous year. This is due to the increment in the number of tests and, at the same time, to the reduction of personnel. The Laboratory Department is running a School for Laboratory Assistants, and the running cost for the School have been roughly considered in the current analysis. Because of scarcity of such analysis there is no opportunity to compare the cost of individual laboratory test in Lacor Hospital with the same test in other hospitals in Uganda. References

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}