|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

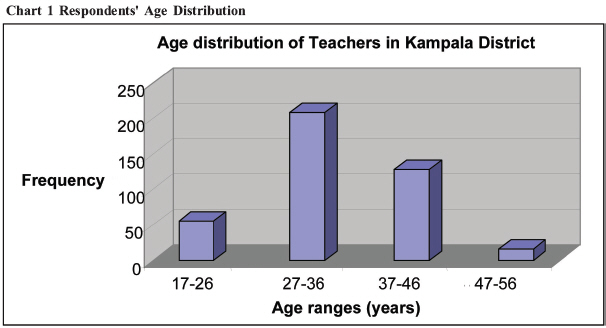

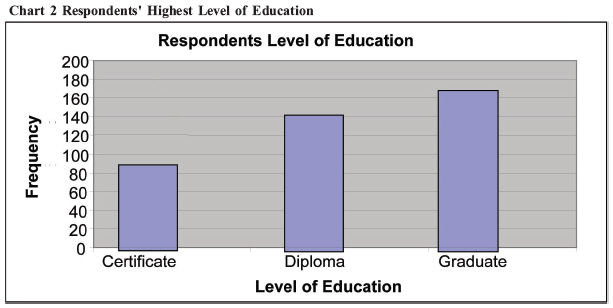

Health Policy and Development Journal, Vol. 7, No. 1, April, 2009, pp. 1-9 THEME: HEALTH INSURANCE The Knowledge and Views of Teachers in Government Educational Institutions in Kampala District on the Proposed Social Health Insurance Scheme in Uganda Aine Aloysious Byabashaija MBChB, M.Sc. E-mail: ainecares@yahoo.com Code Number: hp09001 Abstract The government of Uganda intends to introduce Social Health Insurance (SHI), starting with formal employees in the public and private sectors. For its successful implementation, key stakeholders need to be brought on board at the planning and design stage of the scheme. They need to understand and accept the principles, rationale and procedures of the scheme. Teachers, though low earners in the Ugandan setting, are the majority cadre of formal employees and thus key stakeholders in the proposed SHI scheme in Uganda. This study set out to find their knowledge and attitudes about the proposed scheme, just before the scheme started in July 2007. It was conducted on teachers in government educational institutions of the urban Kampala District, including primary and secondary schools and three universities. It was found that almost 60% of the teachers were ignorant about the proposed policy and the rest had scanty and often incorrect information. They did not want extra deductions from their meager salaries of between US$ 100 - 200 per month and the majority preferred single annual contributions, not monthly deductions. They felt they had been neither sufficiently educated nor consulted about the scheme. They were wary of a possibility of management of the scheme by the government and had no confidence in a government mechanism, due to recent history of corruption and mismanagement of public funds. They expected to get a wide benefit package for their entire families, which was beyond what is in the proposed scheme. The paper recommends intensified education about the proposed scheme for key stakeholders such as teachers, and their involvement in the design of their scheme, passing through their professional associations. It also recommends that government engages in confidence-building activities with the stakeholders of the scheme, to ensure acceptability of a government-mooted programme. Introduction Social health insurance (SHI) is a health care funding mechanism that allows cross-subsidization of the poor by the rich and the sick by the healthy (Anyaehie and Nwobodo, 2004). In Europe, SHI has a long history and, for every country, its structure is dependent upon the existing health problems and availability of resources to pay for health services (Donaldson et al., 1993). However, a typical SHI scheme is characterized by compulsory universal coverage, financed by employers (government or private) and individual contributions. Historically, this type of health financing was preceded by community based or co-operative health insurance, for example the mid-19th century Jyorei cooperatives in Japan, where members even made in-kind contributions for health services with agricultural produce (Ogawa et al., 2003). Although many European countries have adopted SHI, not all do entirely rely on it to finance their health systems. However, those countries using the SHI model are able to raise more money for health care than those relying on general taxation. General taxation has always not been enough to meet the health needs of the people. Moreover, its funds are not specific to health care needs alone. In many developing countries, direct out-of-pocket funding (user fees) were introduced in the late 80s and early 1990s. However, it was sonn realized that they were a barrier to access to health services and even yielded little funds. It was suggested that there is need for a mechanism that incorporates greater risk pooling and protection of the poor, such as health insurance. Social health insurance is a fairly recent concept in Africa. Community health insurance (CHI) schemes have featured the most in Africa (Criel, 1998). Their different forms include community involvement in user fee collection as in the Bamako Initiative in Benin and Senegal; community pre-payment scheme or Mutual Health Organizations in Thies in Senegal; and provider-based community health insurance as in Bwamanda in Democratic Republic of Congo and Nkoranza in Ghana. Others are pre-payment schemes attached to social health insurance or government run systems such as in Thailand and Indonesia (The Thai health card scheme and Indonesia ASKES respectively) (Jakab and Krishnan, 2001). The main problem of CHI schemes has been financial sustainability and the extent of coverage. Private health insurance is common in a few developing countries like South Africa, Namibia and Zimbabwe where it takes up a significant of their heath care expenditure (WHO, 2005). Of all the financing mechanisms, SHI can be a very powerful tool for social protection of the poor if appropriately designed. In Africa, Kenya was the first country to introduce social health insurance in 1966, mainly for formal employees and their families and covered only in-patient services (Okeyo, 2004). With time, other African countries such as Tanzania, Nigeria and Ghana, Zimbabwe have developed social health insurance. Uganda's SHI is still in the design and policy formulation stages. Uganda has a high population growth rate (about 3.6% p.a.) and a population of about 31.9 million people with 87% of them living in rural areas and engaged in informal, subsistence agriculture. Despite a rapidly increasing population, financial support to the health sector from the government has been on a progressive decline. User fees which had been subtly introduced in the mid-90s were abolished in 2001 after they were shown to be a significant barrier to access by the very poor. Their abolition in 2001 resulted into an increase in the utilization of services (Burnham et al., 2000). The Uganda government has embraced SHI as its new strategy to improve heath sector financing. Although the scheme has high political support and its design is in high gear, it is not known whether key stakeholders have been sufficiently sensitized about its proposed operations and implications. One such category of stakeholders is that of teachers. Teachers form a key and wide social network in the country. They are highly believed in by most people especially in rural areas and can easily influence people's opinions about government policy. Through their pupils and students, teachers have access to the community. They have access to current and future generations through their teaching. In Uganda, even though they have low salaries (about $100 per month for certificate level primary school teachers and about $150 per month for graduate secondary school teachers) form the largest category (>50%) of formal employees. For successful implementation of the SHI policy, it is important that the government gains their support for the policy through educating them on the content of the policy, its operations and implications, because it has significant effect not only on their access to health care but also on their take-home salary. This study set out to find what the teachers already knew about the proposed SHI policy, 1 month before it was due to be implemented. It was done in June 2007 while the policy was proposed to begin in July 2007. An earlier feasibility study of the scheme done in 2001 recommended that the government of Uganda continues to investigate the views of the population about SHI since it was a totally new concept (Hsiao et al., 2001). Objectives The objectives of the study were to assess the level of knowledge, attitudes and expectations of teachers in Uganda regarding the proposed social health insurance scheme and to determine their willingness to contribute to the proposed scheme. It was considered that since SHI is a new concept in Uganda and given that there had been instances of failed insurance mechanisms in other sectors, stakeholders' views and inputs at the design stage are necessary for the success of this scheme. Social health insurance experience in Africa Most formal social security schemes are usually tied to formal employment, with contributions shared between employer and employee and the benefits are accessible to the employee and his/her immediate family. However, in Africa the number of people in formal employment being very small, this has limited the use of social health insurance as a significant financing mechanism. Instead, community health insurance schemes have thrived better (Atim, 1998). Though several African nations have proposed social health insurance, only Kenya has experience in implementing a nationwide social health insurance scheme. Its original SHI legislation was passed in 1967 and it established a government scheme, the National Hospital Insurance Fund (NHIF), to cover hospital services. The original law has been amended several times. In Tanzania the contribution of 6% of the salary to the National Health Insurance scheme (NHIS) which is shared equally between the employee and the government covers only central government employees including their spouses and up to four children or legal dependants. Public knowledge and views about social health insurance Studies have reported that low income households are initially reluctant to join insurance schemes because they do not readily accept the idea of paying for services they might not use (Brown and Churchill, 2000). This is mainly because of their little understanding of the concept of insurance but it has often been misunderstood to mean limited potential for social health insurance schemes. Differences in knowledge about insurance may also influence people's perceptions and willingness to pay for health insurance. However, three studies done in Ghana, Burundi, and Guinea Bissau suggest that households in rural areas are also risk averse with regard to health care (Arhin, 1996). Therefore obtaining the public's views and information about their willingness to pay would facilitate scheme design and implementation. Limited experience increases the probability of inappropriate perceptions and consequent reluctance to pay for what is thought as uncertain consumption. Therefore, instead of taking a marketing approach, strategies of basic education should be adopted to provide information on modalities of health insurance and to build population trust. For example exploratory discussions before introducing a scheme in one rural part of Ghana, found that the term "health insurance" was not associated with risk-sharing but instead referred to an unfamiliar product purchased mainly by the urban elite. The only risk-sharing arrangements familiar to the rural communities were described as "solidarity groups", that is, associations of people who assist each other when events associated with specific needs occur (Arhin, 1995). Also, in a study done in Kenya it was found that the general public was skeptical about a proposed National Social Health Insurance Scheme (NSHIS) because of a poor government record of mismanagement and poor delivery of services. There were also fears that the scheme could fall into the hands of officials involved in past corrupt practices associated with the National Social Security Fund (NSSF) and NHIF (Njeru et al., 2005). The above may not be any different from the Ugandan situation but the population requires re-assurance and trust-building in order to reduce the degree of skepticism. Regarding expectations of the employees about social health insurance, these have been found to differ from country to country and within the same country from region to region. For example in the pilot study done on the feasibility for implementation of health insurance for the informal sector in Gujarat-India, it was found out that members especially in the rural areas expected coverage of all illnesses and timely attention to be part of the scheme design (Gumber and Kulkarni, 2000). On the other hand members in the urban areas were most concerned about an affordable price. Almost all the members (90%) in the both the rural and urban settings expected hospitalization services to be part of the scheme. Hospitalization services included (Fees, Medicines, Diagnostic services, Hospital charges).In addition to the above the urban respondents expected specialist consultation to be part of the benefit package. About management of the scheme the rural based members preferred Non-governmental organizations (NGO), followed by public hospitals. In addition they suggested that even the village-level based institutions could be delegated the responsibility of running the health insurance scheme. About willingness to pay, generally all the members were willing to pay but much more surprising was that the urban respondents opted to pay slightly less than what the rural folks were willing to pay. Both the rural and urban respondents were willing to pay for services of hospitalization, chronic ailment and specialist consultation. A study carried out amongst big formal employers regarding willingness to pay for compulsory social health insurance in Tanzania demonstrated much support for the scheme. The employers argued that they were already paying much on health care for their employees (11%) of their payroll because the government services were too poor to meet the demands of their employees. They further argued that the scheme would also have the desirable economic effect of lowering employers' labour costs at the same time making it possible to improve the standards of the government health services (Abel-Smith, 1994). Methodology The descriptive cross-sectional study was conducted in the five divisions of the urban Kampala District namely: Kawempe, Nakawa, Rubaga, Makindye, and Central. Kampala District was selected because it has the highest concentration of educational institutions (public or private) in Uganda. It would therefore easily avail the required large numbers easily compared to rural areas. Moreover, being the capital, it was assumed that the teachers in Kampala would be best informed about any government policies that affect them because of easier access to information through the media and government offices, and that their opinions would be based on information rather than rumours. The study was mainly qualitative and it targeted all teachers in primary and secondary schools and tertiary educational institutions and Universities in Kampala District. Government teachers were purposively selected because it was easier to deal with them through district authorities than those of private institutions. Teachers in private institutions and volunteers were excluded because it deemed very difficult to obtain their full list and to access them since most of them are temporary and do not usually appear on a standard payroll (hence their salaries may not be affected). A sample size of 384 teachers was calculated but we decided to study 400 teachers to cater for cases of possible non-response. For universities, 10 lecturers were chosen purposively. Stratified sampling was done basing on the three levels of education as the strata. The total number of teachers in government institutions in the district were 2697 (Primary: 1473, secondary: 1124 and tertiary institutions: 100). There are also 3 government universities in the District (Makerere, Kyambogo and Makerere University Business School). Given a sample size of 400 teachers, the number of teachers to study was determined by using the relative proportions of teachers in each category except for the universities where only the 10 key respondents were studied. A total of 219 primary teachers, 166 secondary teachers and 15 tertiary institution teachers were therefore studied. The number of teachers to study in each category for each division was determined by using the proportion of schools in that division. The division with the highest number of schools had the highest number of teachers selected for the study. For lecturers, 4 were taken from Makerere University, 3 from Kyambogo University and 3 from Makerere University Business School purposively. Knowledge of the teachers about the proposed Social Health Insurance scheme was assessed by asking them a set of 10 questions about social health insurance using a self-administered questionnaire. The questions covered whether they had ever heard about SHI before; what they understood by it; the contributors; the frequency of contribution; the amount to be contributed; the source of the funds; the benefit package (inclusions and exclusions); the providers; and the management of the scheme. A 5 level Likert scale was used to measure an individual teacher's knowledge about SHI. A teacher who scored <20% was regarded as not knowledgeable about the scheme, 21%-40% was regarded as less knowledgeable on the scheme; a score of 41%-60% as knowledgeable, 61-80% as more knowledgeable and 81%-100% as very knowledgeable. Attitudes were defined as what the teachers think or feel about the proposed Social Health Insurance. They were asked 5 questions on whether they thought the proposed SHI would improve the quality of health services; what they felt about the government decision to introduce SHI as a mode of health financing services (whether it was a good idea); what they felt about the decision to deduct some money from their salary for the scheme; whether they thought the proposed scheme was well designed; and what they felt about those who would not be able to join because they cannot pay. They were also asked 5 questions regarding their expectations from the proposed scheme. They covered the scope of services they thought should be provided; who should manage the scheme; what should be the role of the government in the scheme; the desired number of beneficiaries; and what should be done for the poor. On the willingness of the teachers to pay into the scheme, again 5 questions were put to the respondents to assess their readiness to embrace the proposed scheme. They focused on whether the teachers were willing to contribute to the proposed scheme; how they would want to make their contribution; how much they would be willing to contribute; how frequently they would want to contribute; and how else, apart from financial contribution, they thought they could contribute to the scheme. Results The majority (29.8%) of the 410 respondents came from Rubaga Division, followed by Makindye Division (24.1%), Kawempe Division (21%), Nakawa Division (16.8%), and Central Division had the least (8.3%). Most of the respondents (224/410 or 54.6%) were males while females were 186 (or 45.6%). Most of the respondents (60%) were aged between 17 and 36 years, reflecting early entry into the teacher training institutions with subsequent early recruitment into the teaching profession. The age range of the teachers spanned 40 years, which would be a significant duration for contribution as a formal employee. As seen above, university graduates and Diploma holders were the majority (77.6%) while certificate holders were slightly less than 30%. Most of the respondents (229/410 or 55.9%) had four or less dependants, while 128 (31.2%) had more than four dependants and 53 (or 12.9%) did not give the number of their dependants. It was not clear how many of the stated dependants were eligible to benefit under the proposed scheme. Knowledge on Social Health Insurance Most of the respondents (51%) fell in the category "not knowledgeable about the proposed SHI Scheme", while 35% were "less knowledgeable", 13% were "knowledgeable", only 1% was "more knowledgeable" while no teacher could be classified as "very knowledgeable on the scheme". Asked whether they had heard about the proposed Social Health Insurance scheme in Uganda, more than a half of the respondents (235/410 or 57.3%) had never heard about it, 167 (or 40.7%) had heard about it and 8 (or 2%) gave no response. Those who had heard about the proposed scheme reported that they had read about it in local newspapers (38.0%), from fellow staff (26.9%), from radios only (20.4%), from Television only (7.4%), from both Television and Radios (4.6%) and from workshops (2.8%). Regarding the proposed contributors to the scheme, 84 (20.2%) said it is government employees, 259 (63.2%) thought it is government and private employees, 25 (6.1%) thought it is private company employees while 42 (10.2%) gave no response. Regarding the proposed frequency of contributions the majority of the respondents (186/410 or 45.4%) thought they were to make a single annual contribution, while only 136 (33.2) correctly knew they were to make a monthly contribution. Of the rest, 41 (10%) gave thought they would contribute once in six months while 47 (11.5%) gave no response. On the knowledge of the proposed level of individual contribution, most of the respondents (164/410 or 40%) thought they were expected to contribute less than 4% while 80 (19.5%) expected to contribute more than 4% and 56 (13.7%) said they did not know the amount. Only 110 (26.8%) respondents gave the correct response of 4%. However when asked where the contributions will be drawn from, most of the respondents (257/410 or 62.7%) correctly gave their salary as the source, while 16 (3.9%) of the respondents thought they would get it from their private business and 51 (12.4%) gave other sources while 86 (21%) gave no response. Regarding the providers of care, 178 (43.5%) correctly mentioned both government and private facilities as the proposed providers while 130 (31.7%) thought that only government facilities would provide care and 66 (16.1%) thought only private facilities like NGOS would provide care to the scheme members and 36 (8.8%) did not give any response. Regarding the management of the scheme, only 125 (30.5%) knew correctly the proposed management arrangement of an independent institution, while 194 (47.3%) thought it will be managed by the government, 44 (10.7%) thought it would be managed by a private enterprise and 47 (11.5%) did not enter any response. On the benefit package, only 12% correctly knew the scope of services (included are in-patient and out-patient services, emergency services, orthopaedic and obstetric surgery while cosmetic surgery, transport expenses, burial expense and treatment abroad are excluded) while 50% gave incorrect responses and 38% gave no response at all. When cross-tabulation was done, it was found that respondents with higher education were more likely to have heard about the proposed scheme than their lower cadre counter parts. We observed that 55.8% (or 96/172) of the graduate teachers, 33.6% (or 49/149) of the diploma holders and 28.3% (or 26/92) of the certificate holders had heard about the scheme. Attitudes towards the Social Health Insurance Scheme On whether the respondents thought the proposed scheme would improve the quality of services in Uganda, 256 (or 62.4%) thought it would while 86 (or 21.0%) thought it would not, while 68 (or 16.6%) entered no response. One optimistic respondent said: "If managed well, the scheme will improve the services. There will be enough money to buy dugs and the doctors will then work hard and treat us well" (Diploma holder, Makindye division) However, one pessimistic respondent said: "If the government is just watching as the hospitals are rotting, yet they get a lot of money from the Revenue Authority, what is it that they want our money for? They removed cost-sharing to bring drugs in hospitals, now what you can only get in a government hospital is just a prescription form" (Graduate teacher, Nakawa Division) Regarding the government's decision to deduct some money from their salaries, 365 (89%) were opposed to the deduction while 45 (11%) supported the deduction. Those in favour of the deduction argued that: "We need to support the government although it should think about us so much and at least increase our salaries. May be the services can in the hospitals can improve". (Graduate teacher, Kawempe Division) Those opposed to the idea argued that: "This is another form of tax. Government is not serious. AIDS patients' money was stolen before. How can they convince us that our money will not be stolen?" (Certificate holder, Kawempe Division) Most respondents also suggested that that the government should have a plan to subsidize or waive contribution from the poor who may not be able to pay for the scheme, but ensure that they also access the same package of services. Teachers' expectations from the Social Health Insurance Scheme Most of the respondents (289/410 or 70.5%) expect the scheme to cover both in-patient and out-patient services while 35 (or 8.5%) expect in-patient services only, 23 (or 5.6%) expect out-patient services only and 21 (or 2.1%) expect other services like costs of transport, costs of the coffin and burial expenses to be covered. On who, in their opinion, should manage the scheme, 137 (or 33.4%) thought an independent institution would provide better management, 119 (or 29.0%) preferred government management while 122 (or 29.8%) preferred a public-private mix in management. The rest gave no response. Asked on what the role of the government in the scheme should be, the majority (173/410 or 42.2 %) felt that the government should do the regulatory and advisory roles only, while 41 (10%) thought the government should get involved in the operational management and 130 (31.7%) preferred the government doing the advisory, regulatory and the day-to-day running of the scheme. Only 34 (8.3%) gave no response. The reasons given by those who wanted the government to have only an advisory role were that "Most of the government officials are corrupt and if allowed to get involved in this scheme our money will disappear like Global Fund money did. Government only minds about votes and our money will go to buy votes and not medicines. The planners in government have no skills and may never plan anything for us" (Graduate teacher, Nakawa Division). Those who preferred an independent management argued that: "With independent management we may get value for our money". "We may get services like those in Nsambya, Mengo,or Rubaga hospitals, we are tired of 'sick hospitals' like Mulago" (Diploma holder, Rubaga Division) Those who want government to manage the scheme said that: "After all, government manages every thing. We cannot push the government away from its programmes we should allow it to manage the scheme but if they mismanage it then they should refund our money" (Certificate holder, Central Division). About how many people should be covered by the scheme, 248 (60.5%) said they preferred the scheme to cover more than 4 people, 58 (14.1%) said it should cover less than 4 people, while 104 (25.4%) approved of the government's proposal of covering only 4 people per family. Willingness to pay to the SHI scheme Regarding willingness to contribute to the proposed Social Health Insurance scheme, 169 (41.2%) said they were willing to contribute to the scheme, 125 (30.5%) said they are not, 97 (23.7%) said they had not made up their mind while 19 (4.6%) did not enter any response. Most respondents (150 or 36.6%) preferred to contribute through payroll deductions. The majority (159 or 38.8%) are willing to contribute less than 4% of their salary, 67 (16.3%) were willing to contribute 4% of their salary as has been proposed by the government, 51 (12%) were willing to contribute more than 4% of their salary while 133 (32.4%) gave no response. Those willing to pay more than 4% suggested that contributing too little money may not help at all and may still leave them with the burden of having to buy drugs from the drug shops. Most of the respondents (162/410 or 39.5%) were only willing to contribute to the scheme annually, while only 82 (20%) were willing to contribute monthly as proposed by the government and 40 (9.8%) were willing to contribute every six months. Many (126/410 or 30.7%) did not respond to this question. Those who preferred annual contribution argued that with their meager income, they can only save enough to be able to contribute in a year. Only 41 (10%) felt they could assist the scheme in any other way, and mainly through disseminating information to other categories of people, especially fellow teachers. Discussion The study showed that most of the respondents were aged between 17 and 36 years of age. This was also the same age group with little awareness about the scheme. The finding is consistent with common knowledge about insurance, that the young and energetic are less inclined to know and be interested in health insurance matters since they are still well and strong. There was an upward gradient in the number of teachers who knew about the proposed scheme, starting with a lower proportion in primary school teachers and rising to most of the university lecturers. In addition, most of the Graduate teachers and Diploma holders had heard about the proposed scheme while most of the certificate holders knew little or nothing about it. This suggests that the more educated teachers had better access to sources of information about the scheme. More than 50% of the respondents did not understand the scheme properly. Given that teachers are the majority of formal employees, this is not good news for the proposed scheme. Also considering that this study was conducted in the capital where access to current information is easier through electronic and print media, and workshops, it may be right to think that the situation in the countryside may be worse off. The above further implies that the scheme has not been well publicized and there has been little involvement of the key stakeholders. In spite of the compulsory nature of the scheme, the stakeholders need to understand its basics. Otherwise, their participation will not be full and this affects the success of the scheme. In fact, the Federation of Uganda Employers (FUE) has warned that the scheme is destined to fail unless its intended beneficiaries, including teachers, have been involved at the consultation stages (Kiriro wa Ngugi, 2007). Most of the respondents lacked basic information about the scheme e.g. how frequent the contributions would be, how much they will contribute, the benefit package, who will manage the scheme and who will provide the services. All the above is essential and basic information that the all the scheme's stakeholders need to have at their fingertips. Attitudes to the Social Health Insurance Scheme The equivocal attitude of the respondents towards the proposed scheme could be taken for objection. This could be because of lack of sufficient knowledge about it. If it were true, then it would be in agreement with findings from other countries where it was found that little knowledge about an insurance scheme influenced people's attitudes towards it (Brown and Churchill, 2000). As seen earlier, the misunderstanding could also simply come from a different interpretation of the terminology, as happened in rural Ghana with the term "insurance" (Arhin, 1995). However, the seemingly neutral attitude could also be pragmatism on the part of the teachers, who prefer to approach new government proposals cautiously, having observed recent cases of corruption in the National Social Security Fund (NSSF) and the mismanagement of the Global Fund to fight AIDS, TB and Malaria (GFATM). Similar attitudes have been reported in Kenya, where members were also skeptical to join a similar scheme (Njeru et al., 2005). Since as many as 89% of the respondents did not welcome the idea of having their salaries deducted to fund the scheme, there is need to sensitise the teachers more about the scheme and to build their confidence in government systems before they can feel free to participate. Expectations from the Social Health Insurance Scheme Most respondents expect the scheme to cover outpatient, in-patient and laboratory services as well as medicines. These have already been catered for in the draft proposal. The above expectations are also in line with the findings of a study done in Gujarat, India (Gumber and Kulkarni, 2000). Moreover, the majority of the respondents (33.4%) preferred an independent institution to manage the scheme for transparency and perceived better management and accountability. In fact, the 2001 SHI feasibility study had already noted that, "unless the SHI is structured to be securely insulated from politics, it could be a means of political corruption and patronage and at the end, people would pay higher for SHI and not get value for it" (Hsiao et al., 2001 p. iv). This study revealed that less than 50% of the respondents were willing to contribute to the scheme. However, 59.3% of those who had heard about the scheme were ready to contribute and 38.2% noted that they are willing to contribute less than 4% of their salaries and the majority prefers annual contribution. Conclusions and recommendations Most teachers in Kampala District's government educational institutions were not knowledgeable about the proposed SHI scheme. There had been no formal sensitisation exercises specifically targeting teachers yet they are the majority of the formal employees. Most of those who knew about the scheme had a negative attitude towards it, partly due to historical association of government programmes with corruption, wastage and mismanagement of public funds. They also felt that the scheme was an extra tax coming to further erode their little income. Teachers expected the scheme to provide a wide package of benefits covering all family members for in-patient and outpatient services. They also expected government to have a minimal role in its control, limited to advisory and regulatory aspects. Although they are willing to pay into the scheme, most of them expect annual rather than monthly contribution. The study shows general ignorance about the proposed scheme in a key category of stakeholders, indicating poor sensitization. It is recommended that the Ministry of Health engages key stakeholder categories such as teachers further in education sessions to build their knowledge and appreciation of the scheme, for successful implementation. In particular, teachers have a multiplier effect because they have a ready audience of their students who can even serve as an entry point to their families. They could be approached through their professional bodies or unions like the Uganda National Teachers Union (UNATU) and their local governments, such as Kampala City Council. There is still need for further consultations with stakeholders to obtain their views about the design of the scheme. There is also need for the government to build public confidence in the scheme by designing it properly and keeping it free of possible political intervention. References

© Copyright 2009 - Department of Health Sciences of Uganda Martyrs University The following images related to this document are available:Photo images[hp09001c1.jpg] [hp09001c2.jpg] |

| |||||||||

{kind=link}

{kind=link}