|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

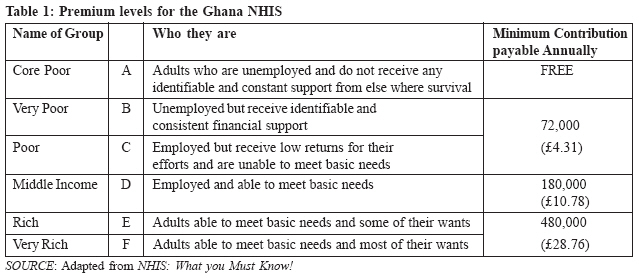

Health Policy and Development Journal, Vol. 7, No. 1, April, 2009, pp. 23-34 A Content Analysis of the Ghana National Health Insurance Scheme Robert. B. A Kuganab Lem Executive Director, African Centre for Development Initiatives, P. O. Box TN 2041 Accra, Ghana. e-mail: kuga_robert@hotmail.com Code Number: hp09004 Abstract Several African countries are contemplating the introduction of national health insurance and a few have already started implementing. It is a popular understanding among these countries that by moving away from fee-for-service to a system like national health insurance, the poor and marginalised who are most often the sickest will be protected. The issue of National Health Insurance (NHI) as an alternative health financing system was a popular option in Ghana. However, the desire for NHI and its popularity was not determined by a critical look at the technicalities involved in setting up such a system. Attention was not paid to the fact that the implementation of national health insurance is constrained by a country's economic, social and political context and the inherent technical limitations of health insurance. To determine feasibility in the context of existing constraints, detailed work ought to have been done on the administrative capacity available to technically design the scheme, manage the process and thereafter manage the schemes. Earnings especially of the informal sector, the collection of contributions and the existing health care infrastructure and the commitment and incentives for health providers to make such a complex system work needed equal attention. Careful assessment is critical in producing a policy that is not only desirable but also feasible. It is apparent that the reasoning behind the Ghana Scheme was more towards a general look at risk pooling and providing access by reducing the individual financial burden than a close look at cost containment, efficiency and sustainability. KEY WORDS: National Health Insurance; Ghana Scheme; Sub-Saharan Africa; Insurance Council Introduction In most African and South American countries, economic problems have resulted in decreased government funding of the health sector and reduced access to health care for most of the population. For example in Nigeria, WHO (2006) reports that public spending per capita for health is less than $5 and can be less than $2 in poorer parts of the country. Situations like this have prompted governments of low-income countries to explore alternative forms and sources of health sector financing. In many European countries social health insurance is one of the principal methods of health financing and has a long history (Carrin et al. 2004). In Central and Eastern European countries, social health insurance has recently been developed as part of their economic transition and health sector reforms. Most of the eastern European countries in transition are eager to replace their National Health Service that has been dominant in the past with national health insurance schemes (Berman, 1998). The Czech Republic and Hungary established national health insurance in 1992 and 1993 respectively. Poland promulgated a national health insurance law in 1997, which was not implemented by 1998 (Berman, 1998). Bulgaria on the other hand, is facing problems of lack of political consensus on the direction of health financing reforms (Balabanova and McKee, 2004). However, there is some evidence that large-scale implementation of health insurance schemes is a complex task and in some instances perpetuates the very inequities it is intended to correct (Berman, 1998; McIntyre et al.., 2003; Nguyen 2003). This paper is a result of a largely a desk study augmented with interviews with key stakeholders who were purposively sampled and two focus group discussions from one selected region of Ghana. National Health Insurance National or Social Health Insurance is one of the widely recognised forms of health care financing. It is a contract between the State and contributors to the insurance scheme, the citizens. The theoretical basis for national/social health insurance is that there are positive externalities in the consumption of more health care by the poor and that market failure makes it impossible for private health care providers to come forth sufficiently, creating the need for State or government involvement in the provision of health insurance. Governments note that pooling risks can reduce individual risk because although an event like illness is unpredictable for any single individual, its occurrence is predictable for a large group of people. Glaser (1991) and Kutzin (1997) rightly noted that should an unpredicted adverse event like illness occur, an individual is most likely to be at risk of forfeiting financially much more than a group. This is because individuals cannot predict when they will get ill, the magnitude of the illness and how much of health care they will need and the implications of this need to their financial ability. Abel-Smith (1994) writes that the advantage of all types of insurance is that it is less of a burden to pay regularly when well, than to pay suddenly and without negotiation when sickness strikes. McIntyre et al. (2003) have observed that social health insurance appears in many different shapes and sizes across the world. They note however that that there are a few key features that are common to all social insurance schemes. These features are:

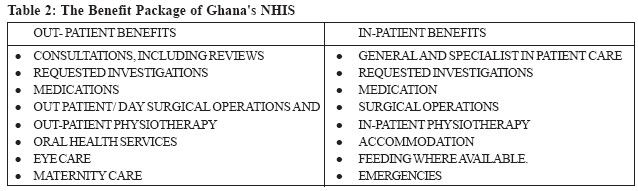

Social health insurance could have sustainable benefits if these key features were the norm in most instances. For instance if payment is based on ability to pay or at least based on visible earnings, social insurance can achieve the goals of providing health care on the basis of need while paying on the basis of income. In some countries, the principle of non-exclusion is undermined by the exemption from membership of richer people (Jacobs et al., 2002). This means the rich who in general are the healthiest of the population do not share in the subsidy of services for the poor members of such schemes. Such situations seriously reduce the degree of solidarity and equity on which social insurance thrives. The Success of Insurance There have been reports of relative success of social/national health insurance schemes in developed countries including developing countries such as Mexico, Costa Rica and South Korea (Carrin and James, 2004). However, Dror and Jacquire (1999), proponents of mutual health insurance schemes, argue that these schemes also have the potential to increase access to health care. Mexico has, since the 1980s, implemented various initiatives to extend the coverage of its social health insurance scheme to poorer groups of its population (Frenk et al., 2005). Mexico's supposed success has been paraded as part of current global debates and advocacy for social health insurance. Lloyd-Sherlock (2006) notes that the current popularity of social insurance is related to the fact that it fits into the current development paradigm of social protection and risk management, which highlights the vulnerability of poor households to catastrophic health spending. However, there is some evidence that social/national health insurance alone cannot significantly contribute to increased coverage rates, provide a wider risk pool and hence increase access to health care. There is equally anecdotal evidence to suggest that poorly designed schemes can have very negative consequences. Studies by Bennett et al (1998), Criel (1998) and Atim (1998) have expressed a similar view and are even less optimistic of community health insurance. They argue that their risk pools are often too small, adverse selection problems are frequent and the schemes are heavily dependent on subsidies, which are most often infrequent and unreliable. Jütting (2003) notes that the schemes that experience managerial and financial difficulties the most are those in the environment of rural and remote areas where unit transaction costs of contracts are often too high. The financial viability of social/national health insurance schemes is also a matter of concern. For example, Mossialos et al. (2000) report that France's social insurance contributions reached an untenable 55% of wage costs and the government had to propose a gradual shift to taxation, which is being implemented. Argentina was a major focus of externally funded social health insurance schemes. Lloyd-Sherlock (2006) notes that the Argentine reforms are now universally recognised to have failed, with the World Bank viewing the large public sector deficits generated by Argentina's insurance schemes as a major factor in the country's financial collapse in 2001. Jütting (2001) in a study of community schemes in Senegal also noted that community health schemes offer financial protection to those otherwise excluded but he also noted that the poorest of the poor are usually not covered. Such findings raise questions as to the extent to which national or social health insurance can be efficiently and effectively ran to provide adequate health care cover for all segments of the population and especially for the poorest and most vulnerable. African Experience With Health Insurance The health financing reforms that are taking place in Africa aim largely to address the problems of affordability and access to health care. Most African countries have positive expectations for social/national health insurance and this view has been largely propagated by the World Bank and other multilateral and bilateral organisations. In sub-Saharan Africa, the countries implementing national health insurance include Kenya, Tanzania, Nigeria and Ghana. Zimbabwe and South Africa have been debating health insurance policy for a while now. Most of the countries that have started implementation are even still in infantile stages of design and redesign and going through very preliminary experiences. Jacobs et al. (2002) warned countries contemplating insurance that social health insurance is no quick fix solution to the financial and access problems facing health care systems. Jacobs notes that to some extent the development of social health insurance in some developed countries, including Germany, was unplanned. The evolution of the system in Germany owed much to the pattern of industrialisation, the growing influence of organised labour and the development of Germany as a united but decentralised country. These are not common features of sub-Saharan African countries. It is worthy of note that there is no universal model for the design of national health insurance schemes and that explains why countries like Germany, France and the Netherlands that started social health insurance schemes almost a century ago are still evolving design paradigms that would ensure equity as well as financial viability of the schemes. It is equally important to note that Sub-Saharan African countries vary greatly in their development agenda and priorities, populations, national politics and systems of government, economics and other endogenous factors. These factors can greatly inform the design of social schemes and the provision of services. With these variations, any design of a national health insurance scheme offers opportunities and experiences worth considering by other countries in the health financing reform process to minimise obvious design pitfalls by adapting tested models to their own unique political, social and economic context. The schemes of these countries are further discussed in the subsequent sections. Kenya National Health Insurance Fund Kenya has the oldest health insurance scheme in sub-Saharan Africa. It was launched in 1965 as the National Hospital Insurance Fund. Eligibility was limited and compulsory for formal sector workers earning a certain amount per month. Contributions were made through a percentage deduction of the salary of the formal sector employees. The deductions started at a minimum of 2% of an employee's salary. Non-salaried persons can join the scheme on voluntary basis. The fund did not make any provision for financially disadvantaged groups. The benefit package was limited to in-patient medical care and did not include hotel services. The policy was considered inadequate as it excluded the majority of the population. In 2004, a new health insurance policy was formulated, forming the National Social Health Insurance Fund which has universal coverage for the Kenyan population. The main thrust of the policy as in Ghana is to ensure access to outpatient and in-patient care for the general population and to significantly reduce the out-of-pocket health care expenditure of households, especially of the poor and vulnerable (Ngilu, 2004). IPAR (2005) reported that the Kenyan National Social Health Insurance Fund is faced with various challenges and inefficiencies. Key among these is poor quality service delivery, inefficiency in premium collections, limited coverage, bureaucratic obstacles, tedious claiming processes and a high transaction cost that is fuelled by fraud and abuse. IPAR concluded that Kenya lacks the prerequisites for a sustainable universal social health insurance scheme and recommended a gradual rollout of the scheme alongside an expansion of health care infrastructural capacity. Tanzania National Health Insurance Tanzania is one of the poorest countries in the world, with more than half of the population living on less than $0.70 a day and health care expenditure per capita estimated at $8.00 per year (Shiner 2003). Shiner notes that donors fund nearly 50% of its total health care spending and this reduces the autonomy of the government of Tanzania in formulating health policy. According to Shiner, Tanzania's health sector reforms must be viewed in the wider context of shifting opinion among influential bilateral and multilateral donors. In Tanzania, national health insurance officially started in 2001. It is compulsory for the formal sector. Employers pay 3% of the employee's salary to the scheme. It covers the spouse of the employee and up to four other dependants and entitlement stops three months after retirement. The benefit package includes inpatient and outpatient care of a fixed predetermined amount. Payment is only made for cost incurred on generic drugs on a national drug list and basic diagnostic tests. The insurance system as it operates in Tanzania effectively limits coverage to formal sector workers and their dependants, a minority of the population. Systems of this nature discriminate between the population's groups according to their socio-economic standing and can only undermine principles of equity in health care provision and are a threat to national cohesion and solidarity. Carrin and James (2004) have noted that in South America, efforts to extend coverage beyond the formal sector have been singularly unsuccessful, leading to a new emphasis on creating separate downgraded systems for the poor. Nigeria National Health Insurance Scheme Nigeria has a GDP per capita of $1500 (CIA, 2006) and its public health expenditure per capita is among the lowest in Africa. National Health Insurance was launched in Nigeria in 1999 after being on the drawing board since 1962. After the launch, the scheme met stiff opposition and could not be implemented until 2005. The Labour Union of Nigeria, health care providers and the population in general did not trust the intentions of Government in establishing the scheme. DFID (2004) reported that the distrust was based on the fact that Nigerians had had bad experiences of poor and fraudulent management of insurance schemes by government officials. The main objectives of the Nigerian scheme are to ensure that every citizen has access to good health care services, families are protected from the financial hardships of huge medical bills and that health care cost is equitably distributed among different income groups of the population. Nigeria chooses a staggered approach to implementation starting with public and private sector formal employees who constitute about 40% of the population. It is estimated that currently, the scheme covers only 10% of the Nigerian population of 120 million (Arodiogbu, 2005). Public and private sector workers are required to pay 15% of their salary to National Health Insurance Council. Employers also contribute 10% of each of its employee's salary to the Council. Employees and their dependants (maximum of four children under age eighteen) are then entitled to both inpatient and out-patient care. Others of unknown or non-fixed income categories can voluntarily join the scheme through Health Maintenance Organisations. The unemployed, the aged and the disabled are exempt from paying premiums. A scheme member can receive care in any part of the country on providing an identification card (Arodiogbu 2005). The policy recognises and supports community-based insurance schemes by re-insuring them. This is quite progressive as it embodies the principles of community engagement in health and building of community ownership of health projects. It also mitigates the general distrust of government projects. Nigeria also opts for capitation as the payment mechanism for its service providers. Although this is good as a cost control measure, it raises questions of how service quality can be adequately checked and enforced. In some countries capitation is not only related to a number of users of a health facility but a percentage of the revenue generated by the service provider. This can be useful in Nigeria at this stage of its implementation but will erode the principle of universal access in the long run. South Africa National Health Insurance National Health Insurance is still under discussion in South Africa and Zimbabwe. After the abolition of apartheid, South Africa had an ambitious plan to transform its inequitable and fragmented health care system that was largely financed through private Health Insurance Schemes. The African National Congress (ANC) government has since 1994 explicitly recommended social health insurance. It put in place a committee of inquiry to produce a blueprint for social health insurance in South Africa. The core objective established by this committee was to improve overall health system equity and to address the cost-spiral crisis in the private sector. Several committees have since been established to push the idea forward but implementation seems far off (McIntyre, 2003). However, other reforms are ongoing, to make the health system more equitable and to meet the needs of the whole population. The include extending the coverage of commercial and private insurance systems to the uninsured, targeting state funds to the indigent and a basic level of primary health care services to the general population. Laws have also been enacted to combine the centrally controlled public system with a managed commercial insurance market. This involves increased regulation of the commercial insurance market in the areas of enrolment, benefits and grievance procedures. The Ghana National Health Insurance Scheme Ghana has an income of $2,700 per-capita (CIA 2006). It spends $12 per capita per annum on health. National Health Insurance became law in August 2003. The law put in place a national health insurance system that aims at enabling residents of Ghana to obtain essential health care services without having to pay for services on demand. The law states in part that it is: To secure the provision of basic healthcare services to persons resident in the country through mutual and private health insurance schemes; to put in place a body to register, licence and regulate health insurance schemes and to accredit and monitor health care providers operating under health insurance schemes; to establish a National Health Insurance Fund that will provide a subsidy to licensed district mutual health insurance schemes; to impose a health insurance levy and provide for purposes connected with these (GOG 2003). The passing of the insurance law was against the background that the government funds about 80% of the public health services bill through general taxation and donor funding and the rest from user fees, which was unsustainable as levels of poverty increased, resulting in a dwindled tax base. This was also compounded with diminished foreign aid which further reduced the capacity of the vulnerable in society to have access to health care services. The Policy Content The Ghana National Health Insurance Scheme (GNHIS) acknowledges that, as observed by Kutzin (2001), the four key functions of an insurance scheme are revenue collection; the pooling of funds; the accumulation of pre-paid health revenues on behalf of a population; the purchasing of services i.e. the transfer of pooled resources to the service providers on behalf of the population for which the funds are pooled; and the provision of services, which include type of providers, and the service they offer. For the purpose of this study, and in line with the Ghana Scheme, the functions above are re-categorised as Population Coverage; Revenue Collection; Benefit Package; Purchasing; and Scheme Management. Population Coverage The Ghana Scheme envisions that five years after the passing of the law (by 2008), every resident of Ghana shall belong to a health insurance scheme that adequately covers him or her to receive essential health care services. The law therefore stipulates the establishment of mutual health insurance schemes (MHIS) in each one of the 136 districts of Ghana. It is the responsibility of the local government to promote the setting up of the schemes through the District Assemblies. The law requires all Ghanaians to register with and belong to a health insurance scheme of their choice. However all persons in formal employment compulsorily belong to the MHIS. Formal employees may also join any other supplementary health insurance scheme of their choice. The compulsory nature of the scheme at least for the formal sector workers is an effective approach in health insurance given that risks are spread more widely. In addition, they are more likely to be the healthiest of the Ghanaian society and therefore, the tendency for adverse selection is effectively reduced. When a person registers into a scheme and pays his/her premium, access to the benefits begins after a three month waiting period, in order to reduce on opportunistic membership. Membership cards are issued at the end of the three months. Each district has its unique member identification card system. A member who moves to reside in a different district is entitled to have his membership transferred to his new district of residence. Universal Coverage Ghana's approach to universal coverage within five years of national health insurance is different from what has happened in Kenya, Nigeria, Tanzania and even in Europe. Only twenty-seven countries in the world had established the principle of universal coverage using social health insurance by 2004 (Carrin et al., 2004). Among these, it took an average of forty years to achieve universal coverage. They are Austria, Belgium, Costa Rica, Germany, Israel, Japan, Republic of Korea and Luxembourg. Kenya also had the benefit of operating a National Hospital Insurance Fund for forty years, before attempting to obtain universal coverage. They have all gathered useful experience and enhanced their capacity to formulate and implement a policy for universal coverage. Ghana does not have the same experience. Theirs is from two private hospital-based schemes and a few mutual health organisations which have been in effective existence and operation for less than ten years. Carrin and James (2005) submit that to achieve universal coverage by Social Health Insurance (SHI), a greater amount of income per capita is necessary, in order to increase the capacity of citizens and enterprises to pay insurance contributions. They note that increased tax revenues are likely to increase with income, thus facilitating the subsequent channelling of any government subsidies into insurance while a steady economic growth is likely to enhance the capacity of private individuals to pay premiums. In some developed countries, health insurance started when they were low middle-income countries. Germany had a GDP per capita of $2,237, Austria $2,420 and Japan $2,140. Currently Ghana's current income per capita estimated at $2,700 is almost at the same as level when these countries started social health insurance. Although being at the same economic level may mean Ghana is ripe to start its insurance scheme, trying to achieve universal coverage within five years may be short-circuiting the gestation period that these nations went through and therefore reducing the chance of its scheme succeeding. Agrarian Country Carrin and James (2004) also note that developing countries, where the economies are dominated by rural agriculture and informal employment, are likely to face administrative difficulties in assessing incomes and collecting premiums. However, for populations in urban areas where there is likely to be at least a minimum quality of infrastructure and communications and a high population density, social health insurance systems are likely to work. Hussey et al. (2003) had earlier expressed a similar viewpoint. They noted that low and middle income countries with a higher share of rural and agricultural workers and other workers outside of the formal economy may have difficulty in assuring compliance with an insurance mandate for the entire population. This viewpoint therefore casts doubts on the Ghana situation where about 65% of the population is estimated to live in dispersed rural parts of the country, with limited income, engaged in subsistence agriculture and served with limited and rudimentary communication systems. South Korea also failed to achieve universal coverage in forty years. Their scheme was saddled with problems of collecting premiums in the rural areas of the country, determining the correct number of family members and determining individual income levels (Hussey et al., 2003). Skilled Labour The establishment of a NHI scheme requires a sufficiently skilled labour force with capacities in bookkeeping, banking and information processing. The country must therefore have the capacity to administer. Having to start 136 schemes at a go without adequate piloting to create a pool of trained and experienced managers reduces any chance of having sufficient numbers of skilled labour force to manage the schemes. The ILO recognised the inescapable need for skilful managers and recommended that about 300-400 scheme managers and financial experts needed to be trained prior to implementation (ILO, 2003). Solidarity and Trust Social or national health insurance relies heavily on the concept of solidarity. A society with a higher level of solidarity is interpreted as where individuals are more willing to support other individuals. The concept of solidarity may exist within a society but if the majority of the population is poor, then each one may be willing to help another but have no help to offer. This situation of helplessness is worsened by the lack of trust and legitimacy with which governments activities are viewed by the citizenry. In developing countries where governments are perceived as very corrupt and non-accountable, a solidarity requiring pooling of resources together in which government becomes the custodian of the people's resources is viewed sceptically. It is only open political debate and availability of financial information that can help the population to gain trust in government and other agencies involved in managing the schemes. That needs committed engagement and involvement of the population to build trust and legitimacy, and it takes time. Prior to government establishment of the district schemes, there were 159 small scale Mutual Health Organisations in 2001 (Atim et al., 2001). These mutual health organisations were established by mission hospitals, local churches and mosques, schools, community leaders, market women, ethnic groups and work-based organisations to share the risk of the cost of health care for their members. These organisations were reported to have strong and sustainable solidarity largely due to the significant power of the members over appointments and management decisions and the use of open and easy-to-understand financial accounting systems. Currently, these schemes have been absorbed by the district-wide schemes. Absorbing them in the much amorphous district MHIS erodes their strength of group or communal solidarity. Trust, which is a cardinal issue in any insurance system, is certainly reduced in an amorphous government organisation. People are less likely to part with their money now in exchange for a promise of future service to an organisation they do not trust. Revenue Collection There are three main sources of funds for the NHIS. A Health Insurance Levy (earmarked tax), premium contributions from workers and their employers in the informal and formal sectors and other miscellaneous sources including money that may allocated to the Fund by parliament, grants, donations, gifts and any other voluntary contributions made to the fund, and money accruing to the Fund from investments made by the insurance Council. Formal sector employees contribute 2.5% of their salary to the Social Security and National Insurance Trust Fund (SSNIT). The Health Insurance Levy The National Health Insurance levy is a 2.5% tax on expenditures and transactions on goods and services captured through Value Added Tax (VAT). Funds raised from this levy are used to subsidise the contributions of the core poor and vulnerable segments of the population. This was made possible by increasing the VAT rate from 15% to 17.5% though it was a contentious issue. The political opposition paraded the view that the increase was simply at the behest of the IMF for economic reasons rather than as an earmarked tax. They argued that the increase will affect the poor in the long run, since they also have to contribute to it through purchase of goods. Premium Contributions The main source of funds for the schemes is the premium collections. The premium levels were arrived at after estimates of the average cost of health expenditure per capita. Different social groups in the informal sector are to pay varying levels of premiums as depicted on Table 1.0 The premiums are paid on yearly bases. The law recognises that about 70% of Ghanaians are in the non-formal sector and that there will be problems collecting contributions from this sector. It also recognises that about 40% of the population live below the poverty line and may not be able to afford high premiums. It is to solve this problem that the rich will pay more while the poor pay less, as illustrated in Table 1. In principle national health insurance involves the transfer of resources from relatively richer and low risk social groups to the relatively poorer and sicker population as an act of mutual support. The majority of Ghanaians are classified or classify themselves as poor and therefore pay category B and C premiums. As at March 2006, more than 99% (source: field notes) of those registered paid the minimum premium. The categorisation into social groups is voluntary and people are not willing to identify themselves as middle income, rich or very rich. This therefore means that almost all the social groups pay the minimum premium. This raises issues of equity since the better off in the population do not contribute a greater portion of their income compared to the poor. Therefore, there is regressive financing in the scheme. Even though the minimum premium is comparatively low and easily affordable by the rich, it is a greater proportion of the income of the poor and the majority of them cannot afford it. There is evidence of high price elasticity of demand in community health insurance schemes. In some sub-Saharan African countries a small rise in premium drove away a large number of members (Atim 2001). Bennett et al. (1998) had earlier corroborated this, noting that in sub-Saharan Africa it is only the rural and middle-class that can afford to join such schemes because of the in-ability to pay of the very poor. The most common policy option to increase uptake is premium subsidy for the poor by the government. Several questions emerge in the case of Ghana: to what level must the premium be subsidised in order to enhance uptake by the poor? Who is really poor in Ghana and how can they get identified? Another problem of premium is the fact that the premium levels are set by the council for the districts. Some districts have lower income especially districts in the north and some central parts of the country. These are the districts also underserved with poor and inadequate numbers of health facilities and very poor health outcomes. They are in a better position to determine their own affordable and equitable premiums locally, than depending on a nationally set level for to make premiums universal even in areas that have tertiary level facilities is to widen the access gap and create more problems of inequity. The Korean government noted that the poor and the elderly and those who dwell in the rural areas have lower access to health care due to mal-distribution in health facilities and health staff. As a result, it successfully expanded its system of social health insurance to the entire population with a concurrent expansion in health care facilities and health manpower even to the rural areas to accommodate the increased demand and to maintain and enhance equity (Bennett and Gilson, 2001). There is no evidence that the premium levels and the earmarked tax for the scheme were established after solid and adequate cost analysis. Some detailed work on costs of main service categories, estimates of their utilisation or disease incidence as well as projecting the income and expenditure of the scheme could have provided some evidence for setting premiums and establishing funding levels of other funding sources. Without realistic projections the schemes may suffer from lack of funds as uptake increases resulting in increase demand of services. Any indication of lack of funds in the immediate future will severely destroy any trust that people may have for the schemes. District schemes could have generated their own start-up cost and projected income and expenditure for the first few years. Bluntly put, there is no explicit budget or a medium-term financial plan which shows the contribution of insurance. Formal Sector Contributions Workers of the formal sector do not pay direct premiums. The 2.5% of their salary contributions that SSNIT makes to the Health Fund covers them. Formal sector workers are then entitled to the benefit package in the district scheme in which they register. The 2.5% of workers contribution to SSNIT was negotiated at levels acceptable to SSNIT in order that it does not become insolvent, but has no relation with workers' health care costs. The Health Fund The contributions from the formal sector workers and the health levy are pooled into the Health Fund. The object of the Health Fund, which is managed by the Council, is to provide finance to subsidise the cost of provision of healthcare services to members of district schemes. The monies from the Fund are also used to reinsure district schemes by payment of any deficit between contribution of members and claims made by healthcare providers and also to provide for the health care cost of indigents. Although the law mandates the Scheme to ensure that disease burden and mortality patterns serve as one of the basis for allocating financial resources to geographical areas of the country, there is no evidence that this is the case. The envisaged financing sources from the health levy and formal sector contributions will provide substantial resources in the early years of the schemes when informal registration is low. When informal sector registration picks up and the exemptions are applied, the resources may become thin and erode the financial viability and sustainability of the schemes. Health Care Benefits Package The minimum benefit package is centrally defined and it includes both outpatient and in-patient medical care. Its focus is to cover the top ten diseases in Ghana. The benefits as spelled out in the policy are depicted in Table 2. The following diseases and services of public health interest are treated or provided free of charge: in-patient and out-patient treatment of mental illnesses, treatment of tuberculosis, onchocerciasis, Buruli Ulcer, Trachoma and confirmatory HIV test on AIDS patients, family planning services, antenatal and post-natal services and immunisations. Districts are allowed the flexibility to upgrade the minimum health care benefit package depending on their capacity to absorb the additional cost. This upgrade must be financially viable and approved by the regulatory council. The first problem of the benefit package is that there is no evidence to suggest that a detailed costing of the benefit package and its implications on revenue has been done. Avoiding a clear understanding of cost of the benefit package can only lead to inefficient and inappropriate use of resources. Pilot projects could have been useful in generating information on how insurance increases utilisation and how this affects service cost. With pilot projects, the effects of the policy can be measured over time to provide evidence towards nationwide implementation. Experience from community health schemes indicates that for much of the informal sector, excluding outpatient care is the only way to marry available resources with the capacity to deal with the most financially catastrophic illnesses where insurance is most needed (Atim 2001). An ideal way for Ghana would have been careful, unhurried piloting that would allow a gradual expansion of the benefits package overtime, and including the outpatient benefits as resources allow. A scheme at its infantile stage may find it overwhelming to combine the provision of both outpatient and in-patient services. In Tanzania, where the package includes both outpatient and in-patient care, the amount payable for services received by a client is limited to a stated amount (the pay-out limit). This curtails costs by reducing unnecessary usage. Where the consumer does not bear direct cost of any sort they tend to use that resource injudiciously. Therefore limiting the benefits package to catastrophic ailments only, especially in the case of Ghana where membership is compulsory, can mitigate the problem of unnecessary usage and cost escalation. Alternatively, the potential viability of the Ghana scheme would have been enhanced if outpatient care was paid for on a pre-payment basis and inpatient care on insurance basis. This would mean that for outpatient care, members would be restricted to a maximum sum equivalent to their contribution, while for in-patient care they could draw irrespective of their contribution. Another option would have been to use a co-payment system for long-term care, which would still be lower than what pertains in the cash and carry system. Under the present arrangement, what is most likely to happen is that since the formal sector workers join the schemes compulsorily and do not have to pay at the time of sickness, they are likely to make use of the most costly benefits. This situation is likely to be prompted by the fact that they are more knowledgeable about the benefits and also need to exploit them to their health benefit. In not limiting the amount of payments that can be made for an episode of ill health, the potential of the contributions collected being eroded by a few members is real and a great threat to the viability of the scheme. Getting service providers to agree to protocols for treatment should have been negotiated and become part of the policy. The act vaguely mandates the regulatory council to ensure that health care services delivered throughout the country are of reasonably good quality and of high standard. The powers and the responsibilities of the council are huge but its capacity to exercise them is inadequate. Provider payment mechanisms could be made to contain incentives in order for them to uphold, upgrade and sustain quality. The Ghana NHIS policy does not spell out incentives for service providers and this can compromise quality. Purchasing the Services The main role of the district schemes is purchasing health services from providers for the insured. In insurance the fundamental goal of purchasing is to achieve a perfect balance between effective provider incentives and the level of risk held by the service provider. Lloyd-Sherlock (2006) rightly notes that the social health insurance programmes are necessarily complex in terms of financial flows, contracts between insurers and different providers. The Act stipulates that payment to service providers is fee-for-service made by the district schemes to the service providers. Each district scheme pays monthly for the services consumed by the insured in that district. A fee-for-service plan places the financial risk on the insurer. This, therefore, can lead to adverse selection and even moral hazard on the part of the patients and providers. This would steadily escalate the health care cost. Moving away from fee-for-service towards capitation would remove the incentive for providers to administer excessive treatment. Even though the act has established a waiting period of three months and a Health Insurance Drug List as cost-containment measures, these are insufficient and not far reaching enough. The Scheme Management The Act established a body corporate known as NHI Council, whose role is to secure the implementation of the NHI policy. The Council oversees and guides the establishment of Health Insurance Schemes nationally. It has an Executive Secretary who has direct day-to-day responsibility of ensuring that policy decisions taken by the council are implemented. The Council reports to the President of the Republic of Ghana through the Minister for Health. All the members of the Council, except the Executive Secretary, hold office for three years, renewable for one other term of three years, and may not hold office for more than two terms in succession. The Act establishes four main units under the Council to assist it to execute its functions. Theses are:

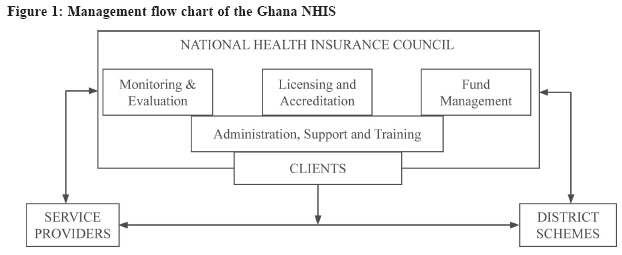

Figure 1 depicts the management relationship between the Council, the district schemes, service providers and the clients. The role of the Council as a regulator of the schemes as well as the administrator of the health fund was variously described by some key actors as incongruous. While the some actors observed that the Council playing these two roles manifested conflict of interest, other groups except government, thought that the council has too much to do and this limited its capacity to deliver The capacity of the Council to assess and accredit health institutions credibly is suspect. There are inadequate numbers of service providers and in some areas none at all. In most parts of the country, service providers have a monopoly and whatever they offer is what must be taken. Therefore, the Council will inevitably offer blanket accreditation of all service providers. Ideally, it should focus on quality, with a view to raising the health services available to acceptable standards before it comes to the issue of accreditation. The management of the schemes at the district level is very elaborate. The legislative instrument establishes that each MHIS will have a District Health Insurance Assembly. The assembly is made up of chairmen or secretaries of the Community Health Insurance Committees in the district. It provides the general policy direction for its district scheme, including a drawing up of a constitution and appointment of a board of directors. The board is, in turn, responsible for the enforcement of the constitution, approval of the budget, rendering the scheme operational, financial accountability to the District Assembly and appointment of management staff for the scheme. The responsibility of the Community Health Committee includes supervising the stratification of residents into socio-economic groupings based their on ability to pay and for collection of premiums. They also identify the core poor who are validated by the main administrative district assembly and/or the Council. The District boards are responsible for negotiating the service contract with the service providers. The staff in-charge of the day-to-day administration of the district schemes includes:

Field evidence suggests that the management staff of all the schemes has been appointed by the Council even before the district assembly and boards were constituted. This undermines the regulations made in the Act and practically it can undermine the authority of the boards and the assemblies at the district level since the allegiance of the staff would be to the national Council. The capacity of the Community Health Committees to truthfully identify the poor through any means test is also poor as evidenced by previous failure in implementing the exemptions policy. Another critical issue is the capacity of the board and management staff to adequately negotiate with the service providers to come up with appropriate contracts. The service providers operate at a different level and one wonders how they could negotiate fairly with an unequal and inexperienced partner. CONCLUDING REMARKS The design and implementation of National Health Insurance and reform are a popular phenomenon across the globe. However, there is emerging evidence of lack of technical and political consensus on the viability of this mechanism. For nations in sub-Saharan Africa that have started implementation, it is evident that National Health Insurance is a complicated task. Decisions about how much should be contributed and by whom and who will manage the funds, the benefit package and provider reimbursement can produce different and complex consequences. As evidenced by this study, the policy content of the GNHIS raises a number of questions. It is clear that the policy tries to address problems of equity in spirit and in letter tries to establish the principle of universal access. However, the practical measures put in place to achieve these are inadequate. It is clear that the Ghana policy content in its current form will not solve the problems it was meant to address. This re-echoes the view that national health insurance policy is difficult and complex to formulate and implement. It is in this light that Berman (1998) cautioned that successful health system change like evolving a new health financing mechanism requires artful combination of establishing the right structures for financing and delivery of health care and developing appropriate behavioural patterns in the consumers, providers and managers within these structures. References

© Copyright 2009 - Department of Health Sciences of Uganda Martyrs University The following images related to this document are available:Photo images[hp09004t2.jpg] [hp09004t3.jpg] [hp09004t1.jpg] [hp09004f1.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}