|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

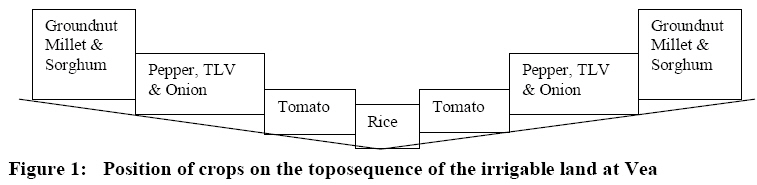

African Journal of Food Agriculture Nutrition and Development, Vol. 9, No. 6, Sept, 2009, pp. 1436-1451 The Tomato Industry In Northern Ghana: Production Constraints And Strategies To Improve Competitiveness Clottey VA1*, Karbo N2 and KO Gyasi3 *Corresponding author: catuq@yahoo.com Code Number: nd09072 ABSTRACT Market-oriented agricultural development is a way to empower smallholder farmers in developing countries who are increasingly getting involved in commodity value chains. The position of smallholder farmers in commodity value chains can be improved by enhancing their distinctive competencies. Entrepreneurs in the northern Ghana tomato industry are taking advantage of recent government policies to promote agribusiness. The competitiveness of the industry is assessed in this paper and possible pathways to empower smallholder farmers to grow from supply chain actors into value chain integrators and possibly co-owners of the tomato value chain is discussed. A three-day Participatory Rural Appraisal (PRA) was conducted at Vea among the 2856 inhabitants living in 625 houses in 2004. The farming systems and market opportunities of tomato growing communities situated on an irrigation site were studied. The staff of the Irrigation Company of Upper Region (ICOUR) Limited who manages the irrigation site was also engaged in the focus group discussions during the PRA. Tomato production, despite being capital intensive was the main enterprise of the communities situated on the Vea irrigable lands. This typifies the other irrigation sites in northern Ghana. The root causes of the reduced levels of capital investment in tomato production were found to be the non-observance of right production techniques and absence of processing facilities in the proximity of the irrigation project. The northern Ghana tomato industry now has the potential to become competitive, and develop into a network of value chains after the former Pwalugu Tomato Factory, closed in 1990 was re-opened in 2007 under new management and a new name – Northern Star Tomato Company. This anticipated competitiveness of the revamped tomato industry in the northern part of the country was analyzed based on the Porter’s Diamond and the typologies of value chains were proposed. Building competencies of farmers or their organizations to enable them to play greater roles in chain management is recommended. It is also of the view that development workers should get farmers engaged in a few more chain activities that can enhance their position in the tomato chain to improve their livelihood. The content of the Farmer Field School concept for technology transfer could be improved to enhance the business skills of farmers and entire rural communities. This may diversify their activities into related enterprises upstream and downstream of the predominant primary production. Key words: Agribusiness , Ghana, tomato, value chain INTRODUCTION The Government of Ghana has identified production inefficiencies and inaccessibility to markets as the major constraints to Ghana’s agribusiness sector [1]. Increasing efficiency and creating new employment through micro-enterprises is a viable solution to rising unemployment; rural-urban migration; inefficient use of resources; and lack of international trade capabilities [2]. Increasing demands from traders and rising imports of tomato products combine to make marketing of tomato fruits a daunting challenge to smallholder farmers in northern Ghana. Lack of a secured ready market for tomatoes produced at dam sites in the Upper-East region and Janga in the northern region has been a major concern to most farmers who often run into debt. Market queens from southern Ghanaian markets sometimes prefer to move further to buy from farmers in neighbouring Burkina-Faso. Tomato production has been an important agricultural venture in the Upper East region, and has a great potential for growth and employment generation. A survey report by Trade Aid Integrated, an NGO, pointed out that tomato production gave employment to about 11,728 farm families from the Upper East region and with an average family size of 5 persons, it is estimated that 58,640 persons benefit from its production [3]. Improvements in macroeconomic management have resulted in appreciable growth and stability in the Ghanaian economy but what next [4]? Microeconomic foundations of development, anchored in creating enabling environments for businesses to thrive, looks like the right choice. The promotion of agribusiness clusters is vital as weaknesses in the national business environment are tackled to improve people’s livelihoods. Clusters are groups of interconnected firms, suppliers, related industries and specialized institutions in particular fields, that are present in particular locations[5]. This may be the principle that should govern the District Industrialization Programme of Ghana. In 2007, the former Pwalugu Tomato Factory that closed in 1990 was re-opened under new management and a new name – Northern Star Tomato Company (NSTC) as part of the District Industrialization Programme in Ghana. As at the time of writing this paper, the new tomato factory was under going test runs and had not yet been connected to the national electricity grid. This major policy drive called for analyzing the competitiveness of the revamped tomato industry in the northern part of the country. This study examines the constraints of the tomato industry and assesses the strategies to improve the competitiveness of the industry in northern Ghana MATERIALS AND METHODS A Participatory Rural Appraisal (PRA) to study the farming systems and market opportunities of tomato growing communities situated on an irrigation site was carried out in July 2004 at Vea (read more about PRA methodology in [6] and [7]). Vea represented the communities that share the irrigable lands of the Vea irrigation project, which had been under the management of a parastatal company, Irrigation Company of Upper Region (ICOUR) Limited, since 1965. There were three days of interaction with the community members. The team also held discussions with the extension staff of ICOUR and the staff of the Gowrie clinic to determine health related issues of labour at the dam site. Various PRA techniques, including the problem tree construction and analysis, were employed in the analysis of production constraints as well as livelihood strategies in the study area (read more on PRA techniques in [6]). This helped to improve the visualization of the information gathering and sharing process. Stones of equal size were used as counters to aid in quantitative data representation by respondents during focus group discussions. Direct observations for bottlenecks and opportunities and field measurements of farm size were made within the community and at the irrigable sites. To foster learning and understanding of the problem situation within the community and the research team the soft system methodology was used [8]. Secondary data were collected from newspapers and government policy documents for cross-checking and triangulation. Information and quantitative data were represented in tables and diagrammatic illustrations. More than three years after the field study, the problem situation identified in 2004 continued to be mentioned in the news and statements of government officials. New equipment has been installed at the tomato processing factory in the catchment area calling for the authors to use both logic-based and cultural stream of analysis to evaluate the competitiveness of the tomato industry [8]. The competitiveness of the revamped tomato industry in the northern part of the country was analyzed using the four attributes of the Porter’s Diamond and the typologies of value chain development in [5] and [9] respectively. RESULTS Production system, constraints and opportunities Land tenure Vea had 2856 inhabitants living in 625 houses as at May 2004. The irrigable land extends to 9 communities in the Bongo district and Bolgatanga municipality. Some of these communities are Vea, Gowrie and Bongo Nyariga in the Bongo district, Bolga Nyariga, Zaari, Sumbrungu in the Bolgatanga municipality. The communities are not encouraged to grow perennial tree crops on the irrigated lands for fear of the roots breaking the canals. Individual holding sizes range from 0.2-0.6 hectares. Some few farmers own larger plots but they do not crop all and rather lease part out for a season. Agricultural land in the communities is classified into Samani and Mogla also referred to as Project lands. Samani is land belonging to households and situated around their houses. Family members share the samani for housing development and farming. The irrigated fields, mogla, re-allocated to the community members on yearly basis as compensation for the loss of some farmland to the reservoir during the construction of the Vea irrigation dam is cropped all year round in two growing cycles – one under rain fed (May-October) and the other under irrigation (November-April). A village land management committee (VLMC) allocates land at the site and everyone (man or woman) in principle has the right to access the land. However, in practice, husbands and heads of families acquire the land on behalf of their families and households. An individual who has no intention of cropping any portion of the field allocated to her/him in a particular season first negotiates the terms with a prospective user and later informs the VLMC. Both citizens and non-citizens can rent land both at the samani and the project area for farming purposes. A household that fails to cultivate the irrigated field forfeits it to the committee and ICOUR. In the past cropping season ICOUR levied a water fee of ¢169,000[1] per hectare of tomato and ¢120,000 per hectare of rice per season. However, crops grown in the wet season are rain fed, and no user charges are levied. The VLMC of the beneficiary communities of the Vea irrigation project is made up of all farmers in a community who farm on the irrigated land. Each village committee has an executive body made up of a President, Secretary, Treasurer and 2 or 3 other members. Elections to the executive body are conducted every 2-3 years and executive members are permitted to stand for re-election. Cropping system and gender The community produces their most important or preferred cash crops on the irrigable lands. The preference for men and women turned out to be the same. Tomatoes, rice and onions were the most preferred in order of importance (Table 1). Table 1: The most preferred cash crop in the Vea community, 2004

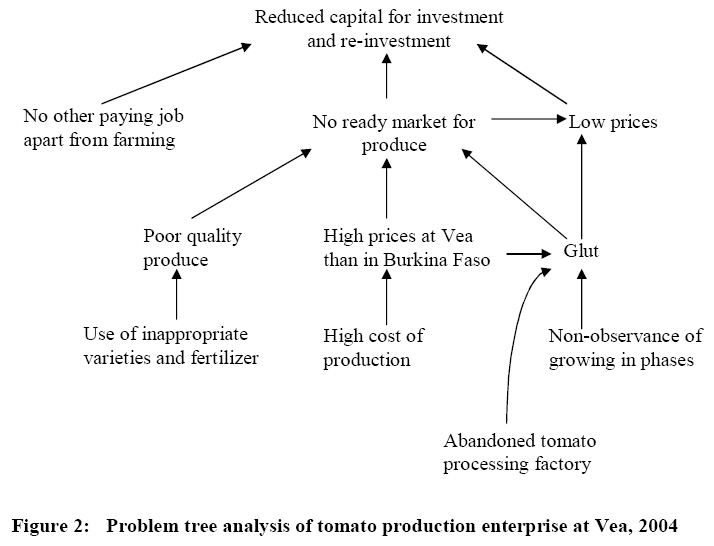

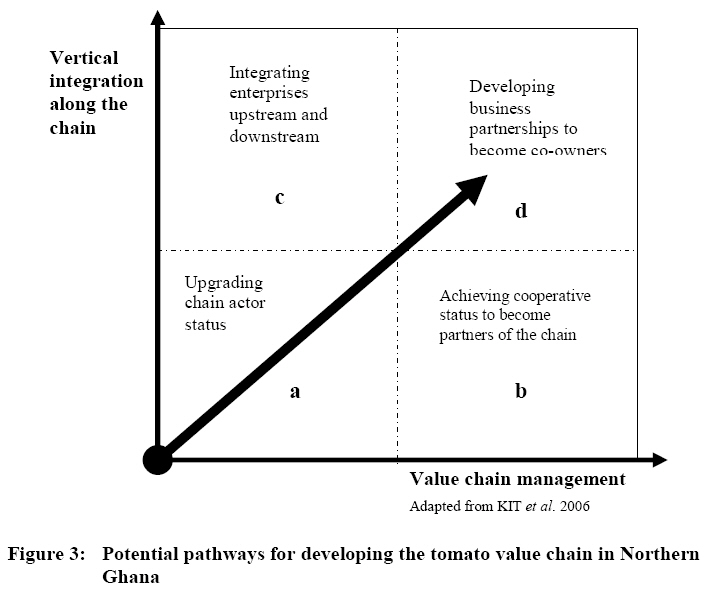

Source: PRA Survey Data, Tomato production attracts more men (60%) than women (40%) because it is capital intensive. Men had more access to financial capital than women in the community. Tomato production was regarded as a risky venture and women appeared not to be ready to take so much risk for fear of incurring debts. On the irrigable lands, it was observed that rice was grown at the valley bottom proper, tomato followed up along the toposequence; and pepper, traditional leafy vegetables (TLV) and onions were found on land slightly above tomato. Millet and groundnuts were grown on the upper levels of the irrigable land (Figure 1). Tomato, onion, traditional leafy vegetables (TLVs) and pepper are grown once in the year as dry season crops; however, rice is grown during both the dry and wet seasons. Groundnut, sorghum and millet are grown only in the wet season on the well-drained elevated portions. The major tomato varieties used in Vea were Pectomech, Tropimech, Roma and a variety the farmers could not name. The hard-skinned Tropimech fruits were the most desired due to their longer shelf life. However, most farmers found the price of ¢95,000 per tin of 100g seed as exorbitant compared to ¢65,000 for the other varieties. On the other hand farmers do not invest in using pure seed but rather re-use seed from the previous crop, often resulting in lower yields and increasing disease persistence. Our analysis revealed that there was no incentive in investing in good seed since the fruit prices are the same irrespective of the variety and seed quality. Constraints in tomato production Both men and women at Vea identified similar constraints to tomato production in the area which were exorbitant land rents; water charges and costs of tractor services, pesticide, seed, and fertilizer. Others were inadequate number of tractors and land for expansion; no places to locate nurseries; poor seed quality; high incidence of diseases; no storage facilities; difficulties in accessing credit; and no ready markets. All these constraints were summed up as lack of capital to invest in tomato production during the analysis. The problem tree analysis in Figure 2 showed the root causes of the reduced levels of investment: non-observance of the right production techniques and the absence of processing facilities in the proximity of the irrigation project. The interesting issues that came out of this study were that farmers knew the root cause of most of their problems and how to solve them but they never took the necessary steps to do so. For instance, the community members knew very well that they could access funds from the Social Investment Fund (SIF) or other financial institutions on basis of having collective collateral by being in groups. However, they were yet to organize themselves into the necessary production groups. The tomato farmers also knew from practice that the best fertilizer to use is the NPK compound, yet they used only sulphate of ammonia (SA) that contributes to rank growth, fewer fruits that are also watery. In the same vein, they knew it was advisable to avoid use of mixed seeds and everyone planting at the same time. Besides, their poor record keeping or complete lack of it impaired making good investment decisions. Often, they did not remember their incomes and expenditures. DISCUSSION The field study revealed that the techniques used by research and extension workers to extend technical advice to farmers did not make farmers own the anticipated innovation process. Often they saw innovations working perfectly on experimental plots that they did not man and that made them skeptical about the results. Experiential learning needs to be encouraged in technology dissemination processes and the establishment of local learning centres that could serve as points for farmers’ meetings and knowledge sharing towards the upgrading of their capacities [10]. The ICOUR intended to facilitate the formation and strengthening of smaller farmer groups in the communities that would replace the large and amorphous village committees. These groups, if successful could act as channels through which improved production techniques, development actions and marketing innovations can get to community members. Competitive position of northern Ghana in the tomato industry The tomato industry in the study area can best be described as a supply chain consisting at one end of input dealers and other upstream service providers from whom farmers source inputs and services such as agrochemicals (herbicides, fertilizers, insecticides,) seeds, and tractor services. At the other end are consumers. Many individuals each performing one or more functions such as trading, haulage, and processing among others occupy the middle of the supply chain. Relationships among actors are not permanent and actors are reluctant to fulfill agreements due to non-binding contractual or no contractual agreements when goods and services are exchanged. Farmers produce without knowing their clients until a buyer approaches them. Such supply chain instability is often costly resulting in risky investments, creates poor customer relations, promotes exploitation and breeds mutual suspicion and mistrust [11]. Tomato farmers fill the bottom of crates with low quality fruits while the traders seek to overfill the crates. Traders detain their hired vehicles for days as a strategy to force farmers to reduce prices while they (traders) do not count the extra cost of transport. Field discussions revealed the desire of the tomato farmers to organize into strong and progressive cooperative organization. To achieve that, existing stakeholders of the tomato industry in the study area need to be coached regarding the value chains where the actors of the existing supply chain collaborate and integrate their enterprises to increase efficiency and competitiveness. Assessment of the field data shows that farmers in their current position as chain actors, as depicted in Figure 3 (quadrant a) lack effective organization, and have low bargaining power and limited control of the tomato marketing process. Farmers can improve their position in the chain by building engagements and managing relationships and linkages with other actors. In this regard, the interventions of development workers should strengthen farmer based organizations and build their capacities to become strong and progressive cooperatives to play a greater role in the management of the chain as partners (quadrant b)in the resultant pathway. The cooperative framework will not only provide entry points for members of groups in the value chain but also opportunities to take on new activities in the chain increasing their control over operational issues (quadrant c). As a progressive cooperative and with further developed managerial skills, farmer groups could establish business partnerships with other local actors to become co-owners of the chain (quadrant d). Indeed, the management of the tomato value chain will involve re-working the tomato business processes and the structure of the industry to lead to full and seamless interaction among all members of the chain [12]. Agribusiness cluster formation Three years after the study, in March 2007, the Northern Star Tomato Company (NSTC) began running with new equipment installed. The factory has the capacity to process 500 metric tonnes of tomatoes into puree which is five times greater than the old processing facility. The NSTC processes the puree for Trusty Foods Limited, an Italian subsidiary located at Tema which adds value and exports the product to the West African sub-region and the European Union [13]. This processing arrangement removes one of the root causes of the lack of ready market analyzed with the community at Vea in 2004 (Figure 2). Indeed, the presence of NSTC creates the needed market that will boost tomato production at the irrigation sites at Tono and Vea as well as on the banks of the White Volta River from Pwalugu to Janga. One limiting factor yet to be overcome is the introduction of varieties that can stand the high night temperatures (above 22oC) from March to October and the appropriate fertilizer formulation and rates. This could increase the tomato production period and volume to meet the demands of the factory throughout the year. To remove the above bottlenecks, it calls for integrating the business of the producers, the NSTC, related industries and specialized institutions into a tomato value system to reduce transaction costs for all stakeholders, boost efficiency, promote innovation and accelerate growth in productivity. The concept of clusters has proven to be particularly powerful in the improvement of business environment because it primarily looks at improving productivity. Productivity is now synonymous with competition according to Porter and clusters bring together government organizations, private enterprises, suppliers and local institutions around a common constructive agenda, thus promoting growth in the economy [5]. In the case of the tomato farmers in the Upper-East region of Ghana, they now have the potential to become a chain partner by organizing themselves into groups to negotiate with the market queens, NSTC, agri-input dealers and the micro-finance institutions. They would also have to work with the Savanna Agricultural Research Institute to solve their varietal, fertility and pest management problems to remain competitive. On the basis of the Porter’s “Diamond” the competitive advantage of the tomato industry in northern Ghana was assessed using four attributes discussed below. Factor Conditions: The risky nature of rain-fed agriculture led to the development of large and small-scale irrigation sites across northern Ghana by the state to facilitate the production of grain and cash crops. This presents northern Ghana with a comparative advantage as the irrigation schemes in the three northern regions can be used to produce tomato all year round, if the appropriate varieties are available. In addition, there is a large agricultural labour force as well as tomato learning centres with a long tradition of growing the crop at Janga, Pwalugu, Tono and Vea irrigation sites. However, other regions in Ghana with longer rainfall periods also have these factors of production. Therefore, northern Ghana needs to develop a competitive advantage to keep a greater share of the tomato industry. Demand Relationships: The revamping of the processing plant at Pwalugu gives northern Ghana a competitive advantage for now. The proximity of the factory to the farmers will improve communication on requirements of actors in the value chain. The partnership between NSTC and Trust Foods Limited will also put pressure on NSTC to meet high standards in terms of product quality. This pressure will eventually be transferred to the farmers who in turn will have to build their capacities to manage quality and to meet contract demands promptly. Increase in farmers’ skills in chain management will improve their status as active chain actors that will move them towards becoming chain partners (Figure 3). Ghanaians at home and in the diaspora have grown an insatiable taste for meals prepared with tomato, especially the paste. This has increased demand for the product. This demand for tomato products (in quantity and quality) is also spreading in the sub-region. This demand has the potential to give the local firms and indeed the local tomato chain actors a competitive edge because of their proximity to these markets. Demands on working wives in West Africa are shaping recipes in most homes to be based on semi-processed food items, including tomato products. The NSTC could take advantage by diversifying into the preparation of mixtures of other vegetables with tomato or only those vegetables when the tomato season ends thus increasing the value created by the chain. These are opportunities for both process and product upgrading and eventually chain upgrading (see for instance [14]). The NSTC may also invest in research to get the much needed heat-resistant tomato varieties and their production guidelines to farmers to assure the company’s raw material base. Strategy, structure and nature of rivalry between firms: The long standing tradition of growing tomatoes and the presence of specialized institutions to provide business support services could be harnessed to improve the competitiveness of the North in tomato production. The government policies to grow micro, small and medium scale enterprises (MSMEs), encourage foreign direct investments and promote agro-based industries are also factors that could combine to make the tomato industry in northern Ghana more competitive [15]. The NSTC has strong rivalry from Afrique Link Limited (formerly Tomacan) located in Wenchi. Innovations will spread through the value system as these two factories and the proposed tomato factories to be sited at Akumadan and Techiman pitch their strength to compete with one another, making them internationally competitive In terms of investment in the industry, the close to 12,000 farm families engaged in tomato production need strategies to take advantage of the prevailing capital markets. They also need to invest in their individual career development to improve their level of integration into the value chain. Re-investment from season to season should not be only at tomato production level but in areas like grading, processing and packaging if their dream of attaining cooperative status is to become a reality. These should go along with similar investments in managerial skills that would lead to the development of more sustainable endogenous structures. Investment strategies that will see farmer groups holding shares in NSTC are options to consider. Related and Supporting Industries: The NSTC would prefer to have tomato fruits from home-based suppliers in northern Ghana all year round, than importing from the Brong-Ahafo, Greater-Accra, Burkina-Faso or Togo. To this end it is in the interest of both the NSTC and farmers to coordinate their activities to reduce transaction costs. In 2004, there was no incentive for tomato farmers to use improved seeds; now they look prepared to jointly find solutions to their production problems with R&D partners. Farmers in the Upper-East and Janga and the NSTC are already asking the Council for Scientific and Industrial Research (CSIR) institutions, namely the Savanna Agricultural Research Institute (SARI) and the Crops Research Institute (CRI) as well as the Ministry of Food and Agriculture (MoFA) to get them appropriate varieties they can grow throughout the year. This is a potential for a viable tomato seed industry to emerge, enabling farmers to integrate better upstream into the chain. Energy supply is another major challenge to the NSTC, which at the time of writing this paper operated on diesel generators, looking forward to be connected to the national electricity grid. The quest for alternative energy supply may lead to the development of other related industries. Biodiesel from Jatropha curcas and biogas from cattle dropping are alternate energy sources, which if developed will create related industries that will boost the competitiveness of the North due to the favourable factor conditions for growing Jathropha and raising cattle. Incidentally the Zuarungu meat factory happens to be in the same region as the tomato factory while women in the adjoining West Mamprusi District also grow Jatropha and extract the oil for domestic use. Fertilizer and crate manufacturing are other enterprises that can be supportive to the tomato industry in northern Ghana. CONCLUSION The tomato industry in the North can catalyze economic growth through agribusiness cluster models that would put the farmer at the centre. In this public-private partnership, the private sector must dictate the pace while government restricts itself to creating the enabling environment for businesses to thrive. Public agencies that make the bulk of specialized institutions supporting the business initiatives must be proactive in generating information and providing the required infrastructural base. The tomato industry in northern Ghana has the potential to be competitive, stimulate the creation of a host of related and supporting enterprises with prospects for wealth creation. The investments made in the establishment of the Northern Star Tomato Company (NSTC) Limited can be safe-guarded if the NSTC will address the root causes of past failures. These include access to improved and affordable seeds; appropriate and affordable soil and water management practices; and technical and managerial production know-how. The dream of tomato farmers’ groups to become cooperative organizations and play active roles in the management of the tomato value chain can be realized if the farmers improve their managerial skills and acquire technical skills in grading, processing and packaging thus making appreciable margins. Building farmers’ competencies in chain management is a challenge to development workers. Farmers’ skills in managing information, quality and innovation needs enhancement. They need to build capacities to enable them coordinate their activities with other chain actors to reduce risk. These can be done using methodologies that promote experiential learning. Technologies have been pushed using the Farmer Field School concept. Similarly, agribusiness concepts can be imparted to rural communities through Farmer Business Schools. In Ghana, the functional literacy programmes for adult learners can serve as entry points and development workers may have to consider putting their efforts together to promote market oriented farming. ACKNOWLEDGEMENT The authors express gratitude to the management and staff of the Catholic Relief Services (CRS), Ghana for financing the PRA sessions. Special mention is made of the staff of FOSADEP – a CRS/Ghana partner who participated in the PRA to build their capacity in participatory methodologies and its application in the field. We are also very grateful to the Vea community members, the management and staff of Gowrie clinic and ICOUR for the valuable information they provided.

REFERENCES

[1] US$1 = ¢8644 at the time of the survey. © Copyright 2009 - Rural Outreach Program The following images related to this document are available:Photo images[nd09072f2.jpg] [nd09072f3.jpg] [nd09072f1.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}