|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

Perception of dental surgeons on the ethical and legal aspects of exercising their profession as personal and corporate entities Mariana Mourão de Azevedo Flores Pereira1, Rhonan Ferreira da Silva1, Luíza Valéria de Abreu Maia2, Ricardo Henrique Alves da Silva3, Eduardo Daruge Junior4, Luiz Renato Paranhos5

1DDS, MSc, Department of Community Dentistry, School of Dentistry, University of Campinas (UNICAMP), Brazil, 2DDS, Department of Community Dentistry, School of Dentistry, University of Campinas (UNICAMP), Brazil, 3DDS, MSc, PhD, Professor, Forensic Dentistry, School of Dentistry of Ribeirão Preto, University of São Paulo (FORP/USP), Brazil, 4DDS, MSc, PhD, Professor, Department of Community Dentistry, School of Dentistry, State University of Campinas (UNICAMP), Brazil, 5DDS, MSc, PhD, Professor, Department Oral Biology, School of Dentistry, Sacred Heart University (USC), Brazil Received: July 19, 2011 Code Number: os11050 Abstract

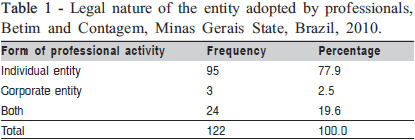

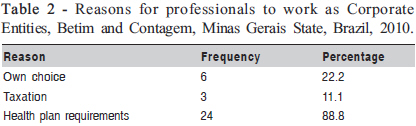

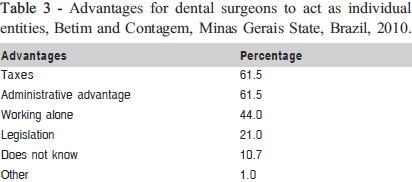

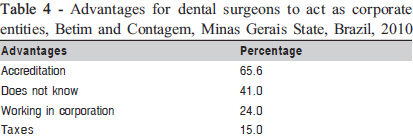

Aim: To evaluate the level of knowledge of dentists of the ethical and legal aspects of exercising their profession as individual and corporate entities; to observe the level of knowledge of professionals on the main taxes inherent to their existence as individual and corporate entities; and to highlight the positive and negative aspects of each entity. Keywords: insurance, health, damage liability, ethics. Introduction The Law is as old as humanity itself, existing since the dawn of civilization and adapting over time to different community contexts. Along with this evolution in Law, people became liable for their actions, both as individual and corporate entities. Specifically, civil liability has evolved from personal retribution, incorporated into the juridical domain and implemented by the State1-2 . The term liability can be employed both in the ethical and juridical senses3. Civil liability deals with the obligation by agents to answer for their professional actions and withstand their consequences. For liability to be constituted, five elements have to be present: agent, professional act, existence of damages, absence of malice, and causal nexus (link between the professional action and damage)4. Thus, in the scope of civil liability, the greatest advance in consumer relations in Brazil took place with the enactment of the Consumer Defense Code5 and the adoption of the objective theory with regard to suppliers and service providers, including corporate entities. For liberal professionals, the code clearly adopts the benefit of proof of fault in the framework of the subjective theory6-9. This code, encompassing all consumer relations, depicts the patient as a consumer and the dentist as a provider and can obligate professionals, under civil jurisdiction, to provide a private service10-11. Due to the facts exposed and the requirement by some healthplans that professionals change their entity status, the aim of the present study was to examine the level of knowledge of dental surgeons (DSs) of the main taxes imposed on individual and corporate entities; to evaluate their knowledge level of the ethical and legal aspects of exercising the DS profession as individual or corporate entities; and to highlight the positive and negative aspects of each entity. Material and methods This research was approved by the Ethics Committee of the Piracicaba School of Dentistry/UNICAMP (Piracicaba, SP, Brazil), and carried out by mailing 392 questionnaires to dentists working in the cities of Betim and Contagem, located in Greater Belo Horizonte, MG, Brazil, whose addresses were provided by the Regional Dentistry Council of Minas Gerais, Brazil. Of the 392 questionnaires sent, 122 were returned and analyzed using descriptive statistics. The questionnaire contained questions on whether the professionals took in patients from health plans, attended ethics and dentistry legislation courses, which type of entity was adopted for their professional activities and why, the advantages and disadvantages of each entity and the main taxes imposed on each type of entity. Each participant of the research received the questionnaire along with an Informed Consent Form that explained the methodology of the study, possible risks and benefits, as well as a sealed self-addressed stamped envelope to return the documents. The confidentiality of the information given was assured, as well as its use exclusively for research purposes. The questionnaires were not individually identified. Results The affirmatives below were demonstrated from the results obtained in the 122 questionnaires returned by the participants, comprising 31.1% of the mailed sample. Of the interviewed professionals, 71.1% alleged taking in patients from healthplans, and 40.2% had not undergone any training on ethics or dentistry legislation in the last 5 years. When asked about the legal entity adopted in their professional activity, 77.9% were individual entities, while 19.6% acted simultaneously as individual and corporate entities, and only 2.5% acted solely as corporate entities (Table 1). Table 2 shows the reasons that led professionals to act as corporate entities in their professional activities. In the question dealing with the advantages of acting as an individual entity, the main advantages cited were simpler administration and taxation (61.5%), and 10.7% of interviewees reported not knowing what the advantages are, as shown in Table 3. However, when consulted on their knowledge of the legal and ethical implications when acting as a corporate entity, only 23.8% declared knowing those advantages, whereas 76.2% did not. With regard to the advantages of working as corporate entities, 65.6% of professionals reported the ease in obtaining health plan accreditations as the main advantage (Table 4). When professionals who act as individual entities were inquired on the main taxes involved in their professional activity, 67.4% reported not knowing the main taxes to which they are subjected, while 32.6% did. In turn, when professionals who act as corporate entities and/or both were inquired on the main taxes involved in their professional activity, 77.8% reported not knowing the main taxes to which they are subjected, and only 22.2% did know. Discussion The number of lawsuits involving dental professionals has been growing in Brazil in both the administrative and judicial spheres. Thus, with the social development of the activities of dentists, ethical and legal precepts come into effect, as well as conditions for the professional exercise of service rendering, which obligate these professionals to become more aware of these aspects. In this way, it is verified that in general dentistry, the knowledge of dentists regarding the civil liabilities and other legal aspects of professional practice are considered superficial12-13 . An important change in the scope of civil liability took place with the application of the rules of the Consumer Defense Code7. Among the guidelines of this document is the principle of consumer vulnerability (the weaker part in consumer relations) and the reversal of the burden of proof2,14. As a result of this legislation, traditional care in dental practice (proper and correct filling of the documentation, such as records) take on a superlative importance in defending the professional11,15,16,17, but are often neglected in clinical routine11,18. The rules set by the Consumer Defense Code5 afforded a greater balance in the legal relations between consumers and product/service providers, leading to important changes in Brazil’s legal scene. These changes took place in the different health services, favoring good professional-patient relations, transforming into a more commercial relationship and leaving aside the previous confidence. Currently, patients affiliated with a health service provider are sent to a given professional through a mere referral by their health plan’s administrative department. Therefore, patients seek more information on their rights and complain when dissatisfied with the quality of the services rendered. This often leads to poor professional/patient relationships, leading to lawsuits. However, dental surgeons are generally unfamiliar with lawsuits and do not bother to learn more about civil law, the Brazilian Civil Code and the Consumer Defense Code, all of which determine the civil liability of professionals while in the exercise of their profession, as shown by the obtained results. This demonstrates a lack of preparedness by professionals – efforts are not made to learn more about these legal questions, even when aware of the existence of administrative and judicial suits. The Brazilian Consumer Defense Code clearly adopts the objective theory with regard to suppliers and service providers, including corporate entities such as clinics. All that is needed is to prove the act, damage and causal nexus in order to award damages8,19-22, without the need to establish fault. Liberal professionals, however, are exempt from this condition, and are given the benefit of the need to establish fault in the framework of the subjective theory. Nevertheless, the fact of whether a professional is an individual or corporate entity does not change the liability from subjective to objective20,23, as a liberal professional may set up a professional partnership only to better organize revenue and expenses, still acting as a liberal professional. What effectively annuls the liberal professional status is not the existence of a corporate entity, but rather the establishment of a corporate entity that explores a liberal profession activity specifically to exploit the advantages of such status. However, there is no consensus in the jurisprudence on this topic. With regard to the liability of health plans, our courts, based on article 14 of the Consumer Defense Code, have been deciding that the liability of health plans, in addition to being objective, must be solidary (joint and several)14,24-27. Dentists, as the liberal professionals they are, can act as individual entities (self-employed professionals), corporate entities, or both. The great majority (77.9%) of interviewed professionals act as individual entities in their profession– that is, act as individually considered individuals, capable of contracting rights and obligations within the law. A minority (19.6%) acts as corporate entities or both, in this case consisting of a grouping of persons whom the law affords the ability to bear rights and obligations28. The civil liability of liberal professionals, as individual entities, is generally subjective, thus requiring fault to be established in order to award damages. The liability of health plans, according to the prevailing doctrine and jurisprudence is objective, whether because these companies perform a public service or as service providers, in the framework of the Consumer Defense Code. The civil liability of dental clinics is generally objective. However, with regard to damages resulting from professional/clinical practice, regular professional action would sever the causal nexus, requiring an evaluation of the professional’s conduct prior to faulting the clinic. When these professionals perform their duties as individual entities, they are subject to certain municipal and federal taxes, which are different from taxes for corporate entities29. The main positive aspects of working as an individual entity are the use of the subjective liability theory and lower tax burden compared to corporate entities. This corroborates the opinion of most (61.5%) interviewed professionals, who affirm that taxation is one of the main advantages of acting as individual entities. The negative aspect involves the difficulty in being included in health plans. Nevertheless, an expressive minority (13%) reported not knowing the advantages of acting as individual entities. However, with regard to knowledge on the ethical and legal implications of working as corporate entities, the results lead us to reflect on the lack of attention paid by dentistry professionals on the legal knowledge related to their professional actions, ignoring its importance in preventing eventual litigation and making the best possible choice of legal entity. Among the advantages of acting as a corporate entity is the ease of accreditation with health plans; however, some professionals (41%) still cannot specify what these advantages are. The negative aspects cited included the tax burden and civil liability, for which there is no consensus in the doctrine or jurisprudence and can therefore be interpreted as objective or subjective. Thus, these data clearly show the lack of preparation by professionals regarding the issue, effectively demonstrating that most professionals change their legal entity status without even knowing the advantages and disadvantages of doing so. The most often mentioned taxes on individual entities are30: Individual Income Tax (in Brazil, original acronym: IRPF); Federal Pension Contribution (in Brazil, original acronym: INSS); Union dues; Municipal Service Tax (in Brazil, original acronym: ISSQN); Corporate contribution (in Brazil, original acronym: CRO - Regional Dentistry Council of the respective District). For corporate entities, the main taxes are: Federal Income Tax (in Brazil, original acronym: IRPJ); Social Contribution; Social Security Financing Contribution (in Brazil, original acronym: COFINS); Social Integration Program (in Brazil, original acronym: PIS); Federal Pension Contribution; Municipal service tax (in Brazil, original acronym: ISSQN) and Corporate contribution (in Brazil, original acronym: CRO - Regional Dentistry Council of the respective District). It may be concluded that the knowledge level of dental surgeons regarding the ethical and legal implications of performing their profession as individual and corporate entities is insufficient; the interviewed dental surgeons are not properly trained on the pertinent ethical and legal aspects of their profession, thus becoming vulnerable to litigation; and these professionals do not have knowledge of the main taxes related to each type of legal entity. References

Copyright © 2011 - Brazilian Journal of Oral Sciences The following images related to this document are available:Photo images[os11050t1.jpg] [os11050t2.jpg] [os11050t3.jpg] [os11050t4.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}