|

| About Bioline | All Journals | Testimonials | Membership | News |

|

||||||

|

||||||

International Journal of Enviornmental Science and Technology, Vol. 4, No. 3, Summer 2007, pp. 383-394 An empirical study of the implementation of green supply chain management practices in the electrical and electronic industry and their relation to organizational performances *M. K. Chien; L. H. Shih Department of Resources Engineering, National Cheng Kung University, Tainan, Taiwan, No.1, University Road, Tainan 701, Taiwan *Corresponding Author Email: chien.mk@msa.hinet.net Received 29 March 2007; Code Number: st07049 ABSTRACT This study aims to investigate the green supply chain management practices likely to be adopted by the electrical and electronic industry in Taiwan, which is dominated by Original Equipment Manufacturing and Original Designing and Manufacturing manufacturers, after the European Union implementation of the Restriction of Hazardous Substances and Waste Electrical and Electronic Equipment directives. The relationship between green supply chain management practices and environmental performance, as well as financial performance, is studied. The approach of the present research includes a literature review, in depth interviews and questionnaire surveys. The companies in the electrical and electronic industry approved by the International Organization for Standardization 14001 certification in Taiwan before December 2004 were sampled for empirical study. The data were then analyzed using statistical package for the social sciences, and structural equation modelling was used as a path analysis model to verify the hypothetical construction of the study. The results indicate that the original equipment manufacturing and original designing and manufacturing manufacturers in Taiwan's electrical and electronic industry have adopted green procurement and green manufacturing practices in response to the current wave of international green issues and have generated favorable environmental and financial performances for the respective companies. Key words: Green supply chain, environmental performance, green procurement, green manufacturing INTRODUCTIONWith increasing awareness of environmental protection worldwide, the green trend of conserving the Earth's resources and protecting the environment is overwhelming, thereby exerting pressure on corporations in Taiwan. The pressure and drive accompanying globalization has prompted enterprises to improve their environmental performance (Zhu and Sarkis, 2006). Consequently, corporations have shown growing concern for the environment over the past ten years (Sheu, et al., 2005). The pressure on corporations to improve their environmental performances comes from globalization rather than localization (Sarkis and Tamarkin, 2005). Increasing environmental concern has gradually become part of the overall corporation culture and, in turn, has helped to reengineer the strategies of corporations (Madu, et al., 2002). To reduce the environmental impact of the waste of electrical and electronic equipment (WEEE), the EU implemented the waste electrical and electronic equipment (WEEE) directive in August 2005. The primary goal of the WEEE directive is to reduce environmental damage by reusing and recycling electrical and electronic equipment, by which the volume of waste electrical and electronic equipment, and thus the capacity for handling it, can be reduced. On the other hand, the ROHS (Restriction of Hazardous Substances) directive prohibits electrical and electronic equipment containing lead, mercury, cadmium, hexavalent chromium, polybrominated biphenyls (PBB) and polybrominated diphenylethers (PBDE). Of the two directives described above, one stresses recycling, reuse and recovery and the other defines the restrictions on the substances used. According to the statistics of Taiwan customs, the total electrical and electronic products exported from Taiwan to the rest of the world within the scope of the WEEE directive amounted to US$ 25.8 billion in 2005. Consequently, corporations in Taiwan have to include the two directives into the design and production of products and have responded by adopting GSCM (green supply chain management) practices. Green supply chain management, also known as ESCM (environmental supply chain management) or SSCM (sustainable supply chain management) (Seuring, 2004), combines green purchasing, green manufacturing/materials management, green distribution/marketing and reverse logistics (Sarkis, 2005). The aim of corporations implementing GSCM is to enhance environmental and financial performance; however, the scope of GSCM practices is very wide and includes internal environmental management, external GSCM, investment recovery and eco-design or design for environmental practices (Zhu and Sarkis, 2004). This study aims to investigate the GSCM practices likely to be adopted by the electrical and electronic industry in Taiwan, which is dominated by OEM (original equipment manufacturing) and ODM (original designing and manufacturing) manufacturers, after the European Union implementation of the ROHS and WEEE directives. The aims of the present research are to discuss the issues that can be summarized as follows:

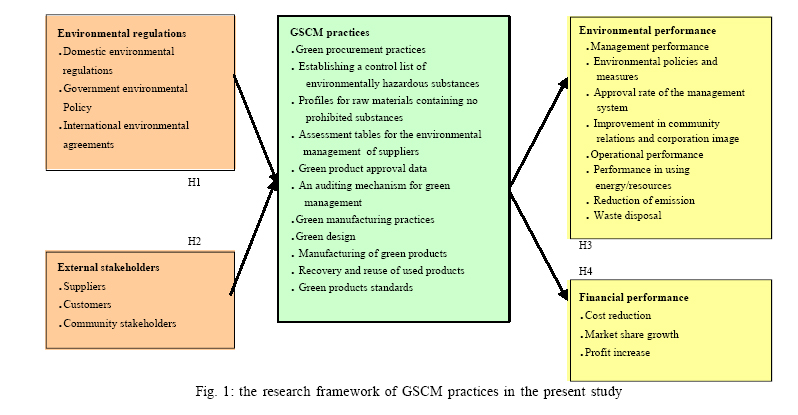

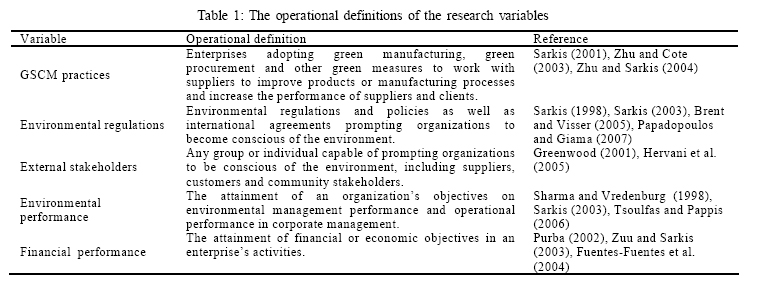

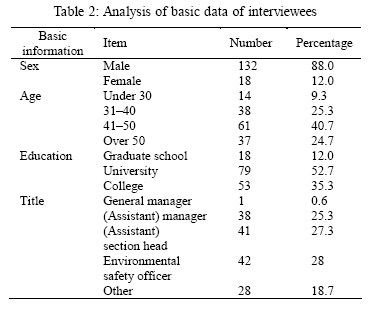

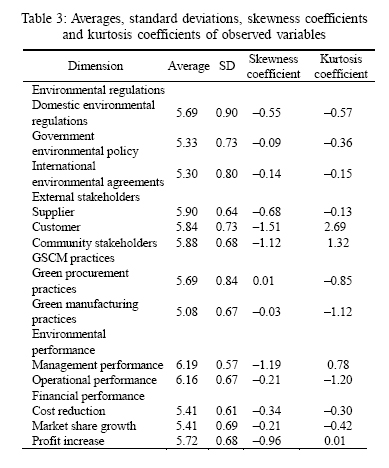

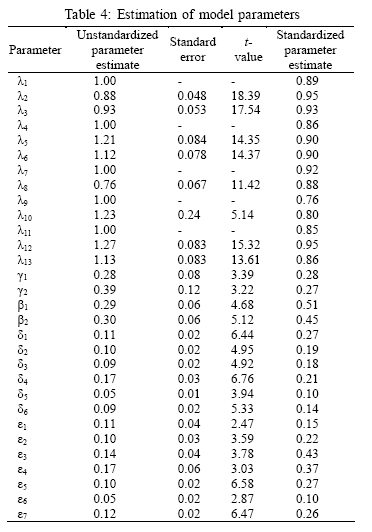

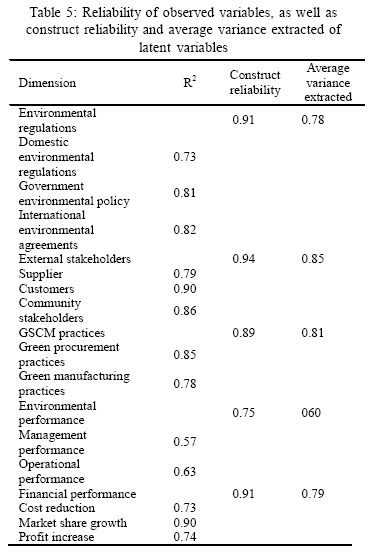

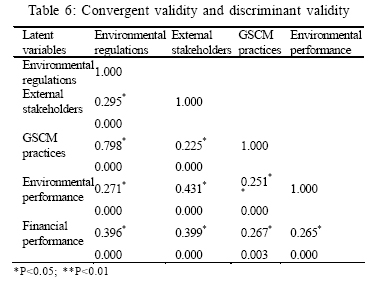

Fig. 1 shows the research framework of GSCM practices in the present study, in which the relationships between environmental regulations, external stakeholders, GSCM practices, environmental performance and financial performance will be discussed through a literature survey, and hypotheses relating these variables will be developed. Description of GSCM practices To meet international expectations and demand for environmental protection, some Taiwanese companies have already implemented GSCM practices. ACER, for example, has established a green product supply chain management system, including green product specification, green products compliance data, an auditing management mechanism, and a green procurement system (ACER, 2005). The environmental management in TSMC covers environmental accounting, life cycle assessment, green procurement and reduction of greenhouse emissions. The company has also implemented measures to ensure that no prohibited substances as defined by the EC are present in their products (TSMC, 2005). Apart from meeting the demands of itsclients,ASUS has also taken initiatives to understand the difficulties faced by its suppliers and provide them with necessary information and services. ASUS also provides their suppliers with ASUS e-Green for registration and evaluation to ensure the capability of suppliers through the mechanism of a part approval process. Finally, the company has established an auditing mechanism for the green management system to ensure that their suppliers conform to green management, thus establishing incentive and elimination mechanisms for green procurement. In summary, ASUS promotes green engineering by implementing green design, green procurement, green production, green marketing and green services in order to conserve natural resources. To ensure that its export to the European market is unhindered, TATUNGestablished a green supplychain to meet the demands of its clients' green procurement standard and the EU ROHS directive. Consequently, its upstream suppliers are requested to provide a guarantee, evaluation report and inspection of hazardous substance management, to assess the suppliers and strengthen the existing supply chain, in order to be able to supply its downstream clients with products conforming to the green procurement standard and the EU ROHS directive (TATUNG, 2005). UMC has established a control list of environmentally hazardous substances and profiles for raw materials containing no prohibited substances, as well as having developed an environmental management table to evaluate the environmental protection performance of its suppliers. The company has also included suppliers' environmental information into its e-management of suppliers and provides necessary training to relevant personnel to enhance their awareness of environmental protection (UMC, 2004). According to Zhu and Sakis (2006), Li, et al. (2006) and Walton, et al. (1998), the green supply chain practices adopted by companies in Taiwan in response to green issues and experts' opinions can be divided into green procurement practices, including establishing a control list of environmentally hazardous substances, profiles for raw materials containing no prohibited substances, assessment tables for the environmental management of suppliers, green product approval data, and an auditing mechanism for green management, and green manufacturing practices, which include green design, manufacturing of green products, recovery and reuse of used products and green products standards. Green procurement Purchasers can improve the environmental performance of products and services by expressing environmental preferences through so called 'green procurement' (Faith-Ell, et al., 2006).Carter, et al. (1998) defined environmental purchasing as consisting of purchasing involvement in activities that include the reduction, reuse and recycling of materials. The procurement or purchasing decisions will have an impact on the green supply chain through the purchase of materials that are either recyclable or reusable, or have already been recycled (Sarkis, 2003). Green manufacturing Pursuing the green manufacturing of products is very beneficial in the alleviation of environmental burdens. Green manufacturing is a manufacturing mode designed to minimize the environmental impact in the manufacturing processes of products (Tan, et al., 2002), and the adoption of green manufacturing helps to reduce waste and pollution (Hui, et al., 2001). Environmentally responsible manufacturing processes, GSCM practices, and their many related principles have become important strategies for companies to achieve profit and increase market share objectives by lowering their environmental impact and enhancing efficiency (Zhu and Sakis, 2006). Research hypothesis External factors affecting GSCM practices: The drives or pressures upon companies to implement GSCM include regulations, marketing, suppliers, competitors and internal factors (Zhu and Sarkis, 2006). The pressure of environmental protection does not come solely from the demands of regulations; consumers and clients also exert pressure on companies (Hall, 2000). Standards, regulations and competition have together prompted organizations to become more aware of any consequences for the environment (Sarkis, 1998). On the other hand, the regulatory, organizational, community and media stakeholders have prompted companies to conduct environmental management (Henriques and Sadorsky, 1996). Environmental regulations and external stakeholders are considered the major factors affecting GSCM practicesaccording toZhu and Sarkis (2006), Hall (2000), Sarkis (1998) and other experts. Environmental regulations Traditionally, system theory stresses the effects of external systems on the decisions and behavior of an organization; external systems include regulations, the law, professional standards, interest organization and social belief (Oliver, 1991). System theory also characterizes the effects of external pressure on organizational structure (Meyer, et al., 1987). Environmental regulations is considered to include domestic environmental regulations, government environmental policies and international environmental agreements according to Zhu and Sarkis (2006), Hall (2000), Sarkis (1998) and other experts. Domestic environmental regulations Domestic environmental regulations prompt companies to adopt relevant strategies and practices to enhance their environmental performance. Domestic regulations and corporations' environmental missions are the two main sources of pressure (Zhu and Sakis, 2006). Furthermore, the major drive for corporation environmental awareness is increasing the role of government regulations (Handfield, et al., 1997). Government environmental policy The public's increasing environmental conscience, the statutory requirements due to government policies and regulations, and pressure from organized groups are traditionally considered to be the factors that sway companies towards adopting a green manufacturing or environmental management system policy (Hui, et al., 2001). Environmental policy targeted directly at emissions will still typically provide the most important single element of a cost-effective environmental policy strategy (Jaffe, 2005). International environmental agreements Although domestic environmental regulations seem to have a greater and more immediate effect on eco-design than the type of economic policy incentive currently associated with WEEE (Gottberg, et al., 2006), many companies and the government are also being influenced by international environmental agreements, such as the Kyoto agreement, the Climate Change Treaty and the Montreal Protocol (EIC, 2005). The EU WEEE directive attempts to tackle the growing quantity of WEEE by making producers responsible for the costs of the collection and recycling of their products at the end of usable life (Gottberg, et al., 2006). Based on the above arguments, a hypothesis can be made as follows: Hypothesis 1: Environmental regulations have a positive relationship with GSCM practices External stakeholders Stakeholder theory did not enter the domain of business management until Freeman published his book, Strategic management: A stakeholder approach, in 1984. Stakeholders, in the wider definition, include any group or individual who can affect or is affected by the corporation (Greenwood, 2001). External stakeholders affecting GSCM include customers, suppliers, the community, regulators and non-governmental organizations (Hervani, et al., 2005). According to Hervani, et al. (2005), Henriques and Sadorsky (1996) and Hall (2000), as wellas other experts, major external stakeholders of GSCM practices are considered to include suppliers, customers and community stakeholders. Suppliers Suppliers contribute to the overall performance of a supply chain, and poor supplier performance affects the performance of the whole chain (Sarkar and Mohapatra, 2006). Supplier-manufacturer relationships are considered important in developing a sustainable competitive advantage for the manufacturer (Sheth and Sharma, 1997; Cannon and Homburg, 2001). Screening of suppliers for environmental performance has now become a key deciding factor in many organizations (Clark, 1999). Customers Customer demands have now become the most important typeof external pressure(Doonan, et al., 2005). To obtain more sustainable solutions, the environmental properties of products and services must meet customer requirements (Zhu and Sarkis, 2006). In the U.S.A., an estimated 75% of consumers claim that their purchasing decisions are influenced by a company's environmental reputation, and 80% would be willing to pay more for environmentally friendly goods(Lamming and Hampson, 1996). Consequently, the influence of the natural environment organizational decisions not only affects the organization that makes the decision, but also its customers and suppliers(Sarkis, 2003). Community stakeholders Community stakeholders are defined as people who are not necessarily involved in the partnership formation but who have knowledge of the community and the organization (Nelson, et al., 1999). If health impacts and sustainable solutions are to be identified with confidence, it is essential that community perspectives are adequately represented and that they influence decision-making (Kearney, 2004). It has been shown that community stakeholders have the ability to influence society's perception of a firm (Henriques and Sadorsky, 1996). Based on the literature review by Greenwood et al., the researcher's hypothesis is as follows: Hypothesis 2: External stakeholders have a positive relationship with GSCM practices. Organizational performance Performance is a measure for assessing the degree of a corporation's objective attainment (Daft, 1995). Corporations adopting GSCM practices may generate environmental and business performances (Walton, et al., 1998; Zhu and Cote, 2004).Agreen supplychain, for example, can improve environmental performance (reducing waste and emissions as well as increasing environmental commitment) and competitiveness (improving product quality, increasing efficiency, enhancing productivity and cutting cost), thereby further affecting economic performance (new marketing opportunities andincreasing product price,profit margin, market share and sale volume; Purba, 2002). According to Walton, et al. (1998), Zhu and Cote (2004) and Purba (2002), as well as other experts, organizational performance is considered to include environmental and financial performance. Environmental performance Environmental performance is defined as the environmental impact that the corporation's activity has on the natural milieu (Sharma and Vredenburg, 1998). Environmental performance indicators consists of OPI (operative performance indicators) and MPI (management performance indicators): OPI are related mainly to materials' consumption, energymanagement, waste and emission production, and evaluation of real environmental aspects of organizations, whereas MPI mainly concerns the administration's efforts, measures, and contribution to the overall organization's environmentalmanagement (Papadopoulos and Giama, 2007). GSCM stresses more than just improving environmental performance;the implementation of green supply chain management can ensure that the corporation itself and its suppliers conform to environmental regulations. Effective management of suppliers can reduce transaction costs and promote recycling and reuseof raw materials.Also, theproduction of waste and hazardous substances can be cut, preventing corporations from being fined as a result of violating environmental regulations. Consequently, the relevant handling and operational cost involved can be further reduced and, in the mean time, the efficiency of using resources can be enhanced (Sarkis, 2003). Furthermore, adopting a sustainable approach can produce less waste and use more recycled material, thereby using energy, water and by-products in a more efficient way (Tsoulfas and Pappis, 2006). Following the above discussions, the present study considers environmentalperformance to include two dimensions: management performance (environmental policies and measures, the approval rate of the management system, and the improvement in community relations and corporation image) and operational performance (the performance in using energy/resources, the reduction of emission, and waste disposal). After the above analyses, the researcher makes the following hypothesis: Hypothesis 3: GSCM practices have a positive relationship with environmental performance. Financial performance Environmental protection activities can have a positive effect on a corporation's financial performance. GSCM can cut the cost of materials purchasing and energy consumption, reduce the cost of waste treatment and discharge, and avoid a fine in the case of environmental accidents (Zhu and Sarkis, 2004). A sustainable approach can lead to internal cost saving, open new markets and find beneficial uses for waste (Tsoulfas and Pappis, 2006). Environmental munificence has a positive effect on financial performance (for example, growth in profits, sales and market share) (Fuentes-Fuentes, et al., 2004). Financial performance is defined here as cost reduction, market share growth and profit increase. To analyze the research done by Zhu and Sarkis et al., the researcher issues a hypothesis: Hypothesis 4: GSCM practices have a positive relationship with financial performance. Samples and analytical methods A questionnaire survey was sent to those electrical and electronic companies in Taiwan listed in the top 1000 manufacturers compiled by the Common Wealth magazine, as well as those that were ISO (International Organization for Standardization)14001 certified before the end of December 2004. The research questionnaires were sent by mail to the electrical and electronic companies in Taiwan, located in Hsinchu Science Park, Central Science Park, Southern Taiwan Science Park, and Export Processing Zone, which include the northern, central and southern parts of Taiwan on December 16th., 2005. The finished questionnaires were received on February 2nd., 2006. Five hundred copies of the questionnaire were sent out, with 151 valid and 20 invalid copies received back, as well as 18 returned empty; hence, the valid response rate was over 30%. These companies were chosen because the EU WEEE and RoHS directives have had the most profound effect on the electrical and electronic companies in Taiwan. The software SPSS and LISREL (Linear Structural Relations) were employed to analyze and assess the hypotheses proposed here. Tools and parameters After surveying Sarkis (1998), Sarkis (2001), Purba (2002), Zhu and Cote (2003), Zhu and Sarkis (2004) and Brent and Visser (2005), the environmental performance assessment in the ISO environmental management system, as well as comments from experts and academics in the electrical and electronic industry in Taiwan, a questionnaire, “The relationship between green supply chain management practices and organizational performances,' was created as the tool of the present study. The items in the questionnaire were then taken as research variables according to the conceptual model of the study. The operational definitions of the research variables are shown in Table 1. According to the methodology of structural equation modeling, the variables of the present research are described as follows: Exogenous variables There are twoexogenouslatentvariables in the present study: environmental regulations and external stakeholders. The exogenous latent variables of environmental regulations are reflected in domestic environmental regulations, government policies on environmental protection and international environmental agreements. On the other hand, the exogenous latent variables of externalstakeholders are reflected in suppliers, customers and community stakeholders. Endogenous variables The endogenous latent variables in the present study are divided into interpretative variables and outcome variables for the final outcome according to the cause- effect relation. Interpretative variables adopted in green supply chain management practices are reflected in two observed variables, green procurement practices and green manufacturing practices. Outcome variablesinclude environmental and financial performance. Environmental performance is reflected in two observable variables, environmental management performance and environmental operation performance, whereas financial performance is reflected in three observable variables, namely cost reduction,market share growth andprofitincrease. Joint variables In the present study, a seven-point scale was used in all questions: 7 for strongly agree, 6 for agree, 5 for partially agree, 4 for not applicable, 3 for partially disagree, 2 for disagree, 1 for strongly disagree. The point for every joint variable was obtained by dividing the total points by the number of questions. RESULTSBasic data analysis The basic data of the respondents answering the questionnaire were first analyzed, by gender, age, education and title; the results are shown in Table 2. Males account for 88% of all respondents, mainly between 41 to 50 years old. Educational backgrounds are largely university and above (64.7%). The titles of the respondents are mostly (assistant) section chief and executive officer in the environmental safety departments, accounting for 65% of all respondents. Choice of assessment method ML (maximum likelihood) of SEM is heavily influenced by variable distribution properties. If the absolute of the skewness coefficient of a variable is larger than 3, this will be considered as extreme skewness; on the other hand, if the absolute value of the kurtosis coefficient is larger than 10, the variable will be considered questionable, and if it is larger than 20, the variable will be regarded as of extreme kurtosis (Kline, 1998). From Table 3, it can be seen that the skewness of the present study ranges between -1.51 and 0.01, with its absolute value less than 3, and the kurtosis ranges from -1.20 to 2.69 with its absolute value less than 10. The results indicate that the skewness and kurtosis of the observable variables are small; consequently, ML can be used to evaluate the model of the present study. Offending estimate In the evaluation of model variables, there is unlikely to be a negative error variance or a very large standard error, and the standardized coefficient cannot be larger than 0.95 (Bagozzi and Yi, 1988). As can be seen from Table 4, all error variances are positive; standard errors are small, ranging from 0.01 to 0.24, and standardized coefficients range from 0.50 to 0.95, which is less than 0.95 and lies below the significance level, suggesting that the effect of offending estimate was absent. Reliability test As can be seen from Table 5, the 13 observable variables' R2 are between 0.57 and 0.90, conforming tothe recommendation that the confidence R2 of an individual observable variable should be larger than 0.50. Also, the construct reliability of the five latentvariables is between 0.75 and 0.94, complying with therequirement that the value should be larger than 0.6 (Bentler and Wu, 1993). Validity test Convergent validity. The factor loadings (λ1"0λ13) of the observable variables shown in Table 4 range from 0.76 to 0.95, which achieve significance and are higher than the threshold, 0.45, indicating that all observable variables can reflect the latent variables constructed. The extracted average variances of the latent variables are 0.78, 0.85, 0.81, 0.60 and 0.79, all of which are larger than 0.5, indicating that the amount contributed to the latent variables is larger for the observed variables than for the error in measurements (Bentler and Wu, 1993). Discriminant validity. The latent variables shown in Table 6 haveall reached the significancelevel, indicating that there is a discrepancybetween the model in which the correlation between any two latent variables is set to be 1.00 and the model in which the correlations for all latent variables are arbitrarily estimated. This discrepancy suggests that the correlation between latent variables can be distinguished, i.e., the discriminant validity is supported. Test for overall model fit The overall model fit is required to adopt at least the following three fit tests (Bagozzi and Yi, 1988): Absolute fit test:

1. NNFI (Non normed fit index) NNFI, larger than 0.9 is generally considered acceptable. The value is 0.97 for the present theoretical model, indicating that the present model is acceptable. 2. CFI (Comparative fit index) CFI, larger than 0.9 is generally considered acceptable. The CFI is 0.97 for the present theoretical model, indicating that the present model is acceptable. Parsimonious fit test: 1. PNFI (Parsimony Normed Fit Index) A PNFI larger than 0.5 is generally considered as a good model. The value is 0.72 for the present theoretical model, indicating that the present model is acceptable. 2. PGFI (Parsimony Goodness of Fit Index) A PGFI larger than 0.5 is generally considered as a good model. The value is 0.60 for the present theoretical model, indicating that the present model is acceptable. 3. Normed Chi-Square An index of less than 3 is considered as a good fit. The value of the present model is 1.51, indicating a good overall fit. Tests for overall model fit were performed in order to understand the fit between the observed data and the hypothesized model. Table 7 shows that the overall fit of the present theoretical model is good (Hu and Bentler, 1999). DISCUSSION AND CONCLUSION GSCM is a relatively new green issue for the majority of Taiwanese corporations. From the perspective of management, GSCM is a management strategy, taking into account the effects of the entire supply chain on environmental protection and economic development. However, the feasibility of reaching the right balance between the environmental performance and financial performance is a serious concern for corporations implementing GSCM. The present empirical study investigated the GSCM practices adopted by the OEMand ODM-dominated electrical and electronic industry in Taiwan in response to the EU ROHS and WEEE directives. The pressures or drives to implement GSCM practices and the relationship between GSCM practices and environmental performance as well as financial performance were also studied. The approach adopted in the present study included a questionnaire and in depth interviews with the electrical and electronic corporations approved by the ISO14001 certification in Taiwan before December 2004. The findings obtained from the 151 valid samples are described as follows: Hypothesis 1 The environmental regulations factors consist of three observed variables: domestic environmental regulations, government environmental policy and international environmental agreements. Their factor loadings, λ1, λ2 and λ3, of the environmental regulations factors of latent variables are 0.89, 0.95 and 0.93, respectively. Their t values are all larger than the significance level of 1.96, indicating that the preliminary fit index is favorable. On the other hand, the path coefficient, γ1, of the normative factors to the latent variables of GSCM practices is 0.28 and t is 3.39, suggesting that the normative factor has a positive relationship with the implementation of GSCM practices. Also, λ2 (government environmental policy) is 0.95, higher than λ1 (0.89) and λ3 (0.93) of domestic environmental regulations and international environmental agreements, respectively, indicating that the pressure on enterprises to adopt green supply chain management practices comes from the government environmental policy of environmental regulations factors. Hypothesis 2 The factor loadings, λ4, λ5 and λ6, of the external stakeholders of latent variables are 0.86, 0.90 and 0.90, respectively, and their t values are all larger than the significance level of 1.96. On the other hand, the path coefficient, γ2, of the external stakeholders factors to the latent variables of GSCM practices is 0.27 and t is 3.22, suggesting that the external stakeholders factors have a positive relationship with the implementation of GSCM practices. The values of λ5 (customers) and λ6 (community stakeholders) are both equal to 0.90, indicating that customers and community stakeholders of external stakeholders have a larger effect on enterprises' adoption of green supply chain management practices than suppliers. A possible cause, as revealed in the in-depth interviews conducted in this study, can be identified from the fact that some interviewees regard suppliers as enterprises' internal stakeholders. Hypothesis 3 GSCM practices consist of two observed variables: green manufacturing practices, including green design, manufacturing green products, recovery and reuse of used products, and setting standards for green products, and green procurement practices, including establishing a control list of environmentally hazardous substances, the profile for raw materials containing no prohibited substances, the assessment table of environmental management for suppliers, the green product approval data, and the auditing mechanism for green management. The factor loadings, λ7 and λ8, of the environmental performance of latent variables are 0.92 and 0.88, respectively, and their t values are both larger than the significance level of 1.96. On the other hand, the path coefficient, β1, of GSCM practices to the latent variable environmental performance is 0.51 and t is 4.68, indicating that the implementation of GSCM practices has a positive relationship with the environmental performance of corporations. Hypothesis 4 The path coefficient, β2, of GSCM practices to the latent variable financial performance is 0.45 and t is 5.12, indicating that the implementation of GSCM practices has a positive relationship with financial performance. On the other hand, the implementation of GSCM practices can provide benefits to organizations, including cost reduction, market share growth and profit increase, whose effects on financial performance are reflected by the values λ11 (0.85), λ12 (0.95) and λ13 (0.86), respectively; the most significant effect of enterprises' implementation of GSCM practices is, therefore, in enhancing market share growth. The above findings suggest that the pressure or drive from environmental regulations, suppliers, consumers and community stakeholders have prompted the electrical and electronic manufacturers in Taiwan to implement GSCM practices. From the present study, and the studies of Seuring (2004) and Gottberg, et al. (2006),it is found that regulations and external stakeholders exert pressure on corporations to implement GSCM practices. Furthermore, it was found that the implementation of GSCM practices can enhance the environmental and financial performance of corporations, consistent with the findings of Purba (2002) and Sarkis (2001), who emphasized the beneficial effects of the implementation of GSCM practices in improving environmental and financial performance. A corporation should not overlook long-term sustainability whilepursuingshort-term profit. It is important to pursue economic development and at the same time consider environmental burden, thereby preserving the natural resources and environment on which the entire human race is dependent, instead of relentlessly exploiting available resources. In pursuing economic development, social justice has to be taken into account in order to strike the right balance between economy, environment and benefit to society. It is therefore suggested that future research may focus on the relationship between GSCM practices and sustainable performance. Enterprises used to be concerned only with their own profit, ignoring the most important links in their production chain: upstream suppliers and downstream customers. The present study found that, in the face of the current global green issue, corporations can benefit from an entirely green supply chain by cooperating with upstream suppliers on green production technology and exchanging green information with them, as well as taking the voices of downstream customers and green consumers into account in their production processes. The conventional end-of-pipe treatment approach taken by corporations in face of environmental problems can no longer meet the demandsof international environmental protection. To meet the expectations of society, pollution preventive measures should be adopted as an environmental management strategy. However, corporations in general are concerned that stressing environmental performance would add to their operational cost, accompanied by a decreasing market share and competitiveness. Nevertheless, the present study found that the implementation of GSCM practices has a positive effect on environmental and financial performance; that is, an increase in environmental performance will be accompanied by increased corporation profit and market share. These conclusions effectively dispel the doubts of those corporations in Taiwan that have not yet implemented GSCM practices. REFERENCES

© 2007 Center for Environment and Energy Research and Studies (CEERS) The following images related to this document are available:Photo images[st07049t5.jpg] [st07049t6.jpg] [st07049f2.jpg] [st07049f1.jpg] [st07049t1.jpg] [st07049t4.jpg] [st07049t2.jpg] [st07049t3.jpg] |

| |||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}